As-reported metrics fail to see the benefits automation presents for this machine vision systems pioneer

When the lights turned back on for the first time across the world’s factories after a significant period of lockdown, it was clear to manufacturing executives that their industry would be no exception to the massive technological disruption instigated by the pandemic.

With workers spaced out and production volumes running well below full capacity, automation emerged as a clear avenue towards increasing efficiency and reducing costs. Yet, for one of the industry’s biggest suppliers, as-reported metrics fail to show how profitable mastering the art of “seeing” can be.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

When the pandemic first began in mid-March 2020 and the U.S. economy began to go into lockdown, manufacturing companies and their workforces were not viewed as necessary “front-line” workers essential to keeping the country running.

The spread of COVID-19 therefore led many factories in America to close for a period, and unlike many services businesses which could easily make the transition to working from home, factories needed a physical workforce presence to operate.

This disruption to the manufacturing sector led to a significant acceleration of a trend that had been slowly rolling on now for decades: automation.

For years, as technology experts and Luddites have squabbled over the decline of manufacturing jobs and the replacement of human workers by robots, the costs to factory operators of adopting industrial robots has declined rapidly.

While this has made greater adoption of automation cheaper, the pace of adoption was often slow in certain countries, lacking major catalysts to force the transition.

But with health concerns and social distancing requirements during the pandemic, factory workers needed to be more spaced out and less efficiently positioned along production lines, meaning if companies wanted to continue running at anywhere near normal production volumes coming out of lockdown, they needed to jump more fully into the automation trend than they ever had before.

To do that and allow intelligent machines to automate parts of the production process, there is one key capability all industrial robots must have: the ability to “see” what they’re working on.

This is where one of the most important suppliers to industrial robotics makers and the world of manufacturing automation as a whole comes in.

Cognex (CGNX), a manufacturer of machine vision systems, creates the software and devices that allow automated manufacturing equipment to conduct tasks that in the past were delegated to humans. These include inspecting products and parts, detecting defects, and verifying assembly.

One would assume that as demand for automation has been supercharged by the pandemic, Cognex would be printing money as it sells its products to manufacturers around the world.

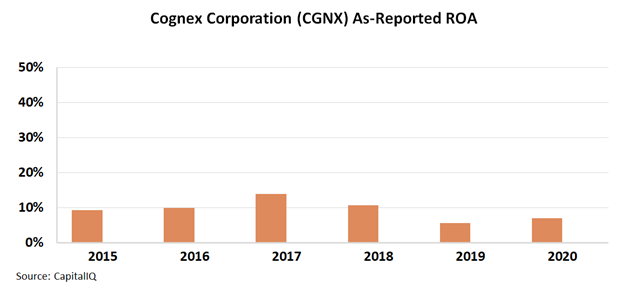

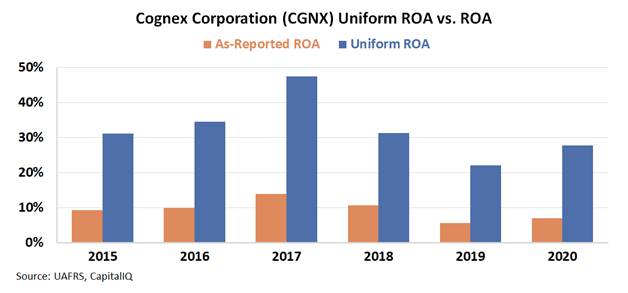

Yet, looking at as-reported numbers over the past 4 years, the vision systems leader has seen return on assets (ROA) decline into the single digits, perhaps signalling its equipment just simply isn’t as valuable as it seems.

In reality however, this is merely a consequence of accounting noise. Cutting through the distortions, Uniform Accounting shows that ROA was actually above 25% last year, and has consistently sustained double digit levels over the past five years, pointing to how essential this company truly is to automation taking over manufacturing processes around the world.

Along with many other waves of technological adoption brought forward by the pandemic and its massive disruption, automation only looks set to continue growing over the next few decades.

By shining a Uniform Accounting spotlight on Cognex, it is clear that the company is one of the industry’s most important suppliers and is surely worth keeping an eye on for potential future investment opportunities.

SUMMARY and Cognex Corporation

As the Uniform Accounting tearsheet for Cognex Corporation (CGNX:USA) highlights, the Uniform P/E trades at 43.8x, which is above the global corporate average of 21.9x and its historical average of 40.8x.

High P/Es require high EPS growth to sustain them. That said, in the case of Cognex, the company has recently shown a 36% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Cognex’s Wall Street analyst-driven forecast is an EPS growth of 42% and 19% in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Cognex’s $87 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 25% annually over the next three years. What Wall Street analysts expect for Cognex’s earnings growth is above what the current stock market valuation requires in 2021 but below that requirement in 2022.

Furthermore, Cognex’s earning power is 5x the corporate average. Also, cash flows and cash on hand are almost 5x above its total obligations—including debt maturities, capex maintenance, and dividends. This signals a low credit and dividend risk.

To conclude, Cognex’s Uniform earnings growth is below its peer averages and the company is also trading below peer valuations.

Best Regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research