This futures exchange has been quietly making a killing on cryptos

With the cryptocurrency craze still in full swing, it’s easy for a bystander to see just how fervently retail buyers have dedicated themselves to the idea of blockchain technology.

Yet, the true motivation behind stripping out the middleman from financial transactions involves more than just passionate day traders and Elon Musk’s Twitter account.

By uncovering the incredible returns one company makes in the exchange service business, which are completely hidden by as-reported financials, we can shed some light on the issue.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The basis of cryptocurrencies and the blockchain technology they are built on is the concept of a post-trust world.

What this means is, rather than relying on credit cards, banks, and exchanges to act as trusted middlemen between transactions, a public ledger is established to verify transactions instead. This public ledger is the power behind cryptocurrencies, and what makes them special compared to other forms of payment.

As everyone can see what is going on, the need for a third party to ensure confidence and facilitate smooth transactions disappears.

However, as any grizzled analyst in the current financial system would have guessed, even in the world of cryptocurrency and blockchain the same old integral financial players are popping up.

One great example is the Chicago Mercantile Exchange, or CME Group (CME), the world’s largest futures and options exchange.

While industry disruptors like Binance (BNB) are attempting to bring crypto futures and derivatives to the masses, CME Group has already been offering them to experienced traders for some time.

As they provide a liquid futures market in Bitcoin and Ethereum, institutional investors flock to the company because they are more comfortable with having an established and trusted partner.

CME Group’s roots go back nearly a century, with the original CME founded in 1898 as an agricultural commodities exchange—dubbed the Chicago Butter and Egg Board.

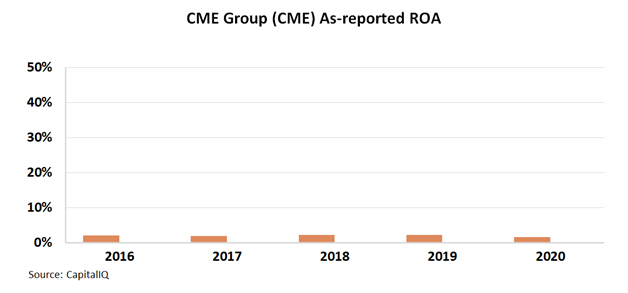

Looking at as-reported metrics though, investors might be scratching their heads as to how the CME Group’s forays into crypto and other futures markets as an artificial middleman have made the company any money.

After all, CME Group appears to not have generated a return on assets (ROA) of above 4% a single time over the past 10 years, suggesting it isn’t raking in cash from investor transactions.

However, a closer look at the real numbers shows why so many want the middlemen gone.

By providing investors faith their transactions will be secure and settled, CME has been minting cash.

The company’s Uniform ROA has never been below 20% over the past decade, and last year alone it rose to 50% levels, 25x higher than as-reported figures suggest.

Those who understand how profitable CME really is also understand how much they’ll save in transaction fees by removing them from the process, and that’s why the idea of distributed trust has gained such popularity.

SUMMARY and CME Group Inc.

As the Uniform Accounting tearsheet for CME Group Inc. (CME:USA) highlights, the Uniform P/E trades at 34.2x, which is above the global corporate average of 21.9x, but around its historical average of 35.4x.

High P/Es require high EPS growth to sustain them. In the case of CME, the company has recently shown a 22% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, CME’s Wall Street analyst-driven forecast is an immaterial EPS decline in 2021 and an EPS growth of 13% in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify CME’s $207 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 12% annually over the next three years. What Wall Street analysts expect for CME’s earnings growth is well below what the current stock market valuation requires by 2021, but just above the requirement for 2022.

Furthermore, CME’s earning power is 4x the corporate average. Also, cash flows and cash on hand are slightly above its total obligations—including debt maturities, capex maintenance, and dividends. This signals a low credit and dividend risk.

To conclude, CME Group’s Uniform earnings growth is below its peer averages and the company is also trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research