This company is transforming its legacy business to the future of transportation

Cummins Inc. (CMI) holds a significant place in the history of diesel engine manufacturing, having been one of the earliest industry pioneers.

Renowned for its immense presence in this sector, the company is now preparing not only to adapt but to establish itself as an industry leader as market dynamics evolve.

To navigate this transformation, Cummins has launched a novel segment New Power (Accelera), which provides hydrogen production solutions and electrified power systems.

Cummins’ management is committed to the idea that the New Power segment will eventually become the company’s most substantial revenue generator by 2040.

However, the market does not appear to share this optimistic outlook and instead anticipates a decline in profitability.

Also below, is the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Hydrogen offers significant potential in the transition to clean energy. It can become the future of transportation…

Hydrogen fuel cells, known for their clean emissions, are particularly promising. While they emit only water vapor and warm air, they currently face challenges related to high costs and limited infrastructure.

However, it is also seen as an efficient way to store and transport renewable energy, crucial for the future energy supply. It can contribute to the expansion of charging infrastructure for electric vehicles.

The outlook for hydrogen is improving, as the cost of producing it from renewable electricity is expected to decrease by 30% by 2030, driven by falling renewable energy costs and the scaling up of hydrogen production.

This trend is sparking growing interest in electrolytic hydrogen.

Hydrogen fuel cell technologies have significant potential in various applications, including vehicles and portable power plants, and major automakers are gradually introducing hydrogen fuel cell electric vehicles in select markets.

Hydrogen’s unique advantages, such as quick refueling and suitability for long-distance transportation, position it as an ideal choice for EVs.

One legacy engine maker is aware of this shift and potential in renewable energy, Cummins (CMI)…

Cummins stands as a prominent institution in the engine manufacturing sector, particularly renowned for its pioneering role in the development of diesel engines.

With a rich heritage from the early days of engine manufacturing, Cummins has established itself as a colossal name in the industry. It is so ingrained that the industry cannot be talked about without a mention of Cummins.

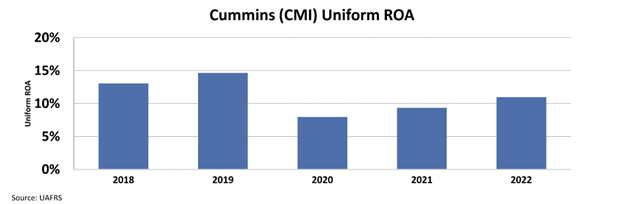

This is why it has been able to recover quickly from the pandemic. While its Uniform return on assets dropped from 15% in 2019 to 8% in 2020, it has been recovering and reached 11% in 2022.

Take a look…

Now, the company is taking an important step into the future. Management introduced the new segment New Power, also known as Accelera. At the heart of it lies a profound commitment to sustainable and efficient energy solutions.

This new segment is actively involved in methods for the production, storage, and application of hydrogen, preparing for the transformation in the energy.

In addition to hydrogen, the New Power segment encompasses a comprehensive suite of electrified power systems. These include advanced battery technologies, poised to revolutionize the expanding electric vehicle market and energy storage solutions.

While the New Power segment currently contributes just 1% of the company’s total revenue, this segment is still in its early stages of commercialization. Cummins’ management envisions a future where New Power becomes the company’s flagship revenue generator, surpassing all other segments by the year 2040.

Being a pioneer in this area, Cummins has the opportunity to unlock higher profitability going forward.

Despite the promising outlook, it appears that the broader market remains skeptical about the growth potential of the New Power segment.

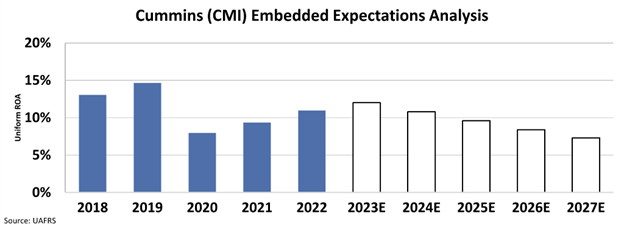

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to fall to around 7%, around the pandemic numbers.

The market remains cautious, foreseeing a potential drop in Cummins’ ROA as the company channels significant resources into this visionary venture.

However, if Cummins is successful in this venture, these levels of profitability might be just the start of something much bigger.

SUMMARY and Cummins Inc. Tearsheet

As the Uniform Accounting tearsheet for Cummins Inc (CMI:USA) highlights, the Uniform P/E trades at 15.0x, which is below its global corporate average of 18.4x and its historical P/E of 16.7x.

Low P/Es require low EPS growth to sustain them. In the case of Cummins, the company has recently shown a 29% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Cummins’ Wall Street analyst-driven forecast is a 23% growth in 2023 and a 9% EPS shrinkage in 2024.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Cummins’ $219.64 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 5% annually over the next three years. What Wall Street analysts expect for Cummins’ earnings growth is above what the current stock market valuation requires in 2023 but below its 2024 requirement.

Furthermore, the company’s earning power is 2x its long-run corporate average. Moreover, cash flows and cash on hand are 1.5x its total obligations—including debt maturities, capex maintenance, and dividends.

All in all, this signals low dividend risk.

Lastly, Cummins’ Uniform earnings growth is in line with its peer averages and its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research