Centene shows that operating a government healthcare system is more profitable than you might imagine

Investors often dislike government contractors for a reason. Accountability to Congress and the American taxpayer forces the federal government to save as much money as possible in its dealings with the private sector.

This inevitably leads to bidding wars by potential clients where the lowest offers might ultimately win the most deals. The resulting low margins make many government contractors look unattractive.

But that’s not to say this is the case for all of them.

Today, we highlight one government contractor whose true profitability is much higher than what as-reported metrics suggest.

We’ll specifically analyze the company through the lens of Uniform Accounting and uncover how it’s able to generate healthy profits on the services it provides, despite working for Uncle Sam.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

When people think of working for the government, what often comes to mind is low pay.

With limited budgets and grand ambitions in many cases, government agencies simply can’t afford to pay workers in the same way as technology companies in Silicon Valley.

Investors often have similar views when it comes to looking at companies that do contract work with the government.

They often assume that the competitive bidding processes for government contracts, where those with the lowest prices are likely to win the most deals, lead to slim margins and unimpressive profitability.

This sets up an environment where it’s nearly impossible for firms to take market share without cutting prices down to match competitors, lest they lose out on business.

You might point to a company like Centene Corporation (CNC) as an example of this phenomenon.

Centene’s primary business is operating Medicaid, the government healthcare program for people who can’t afford health insurance and who don’t have a job that will provide it for them.

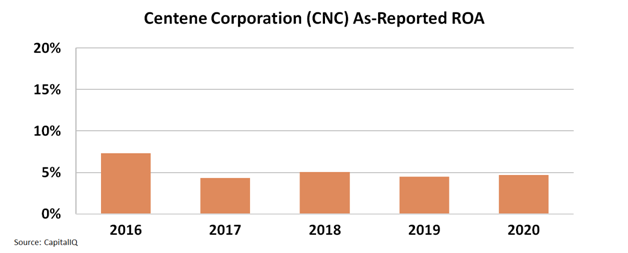

Considering the tight margins for such a government program, where Uncle Sam can simply choose a different provider if Centene raises prices, you wouldn’t be surprised to see that for the past four years Centene’s as-reported return on assets (“ROA”) has hovered around meager 5% levels.

To put that in context, average cost of capital levels in the U.S. currently stand at around 4.8%.

In other words, Centene looks like a business barely generating any economic returns above the costs of its own funds. This makes it a quite unattractive company for many investors looking to generate excess performance.

As the chart below shows, after falling from 7% in 2016 to 4% in 2017, as-reported ROA still hasn’t recovered above 5%.

In reality, the story of Centene’s profitability is much different once we remove Generally Accepted Accounting Principles (“GAAP”) distortions.

Taking a closer look after cleaning up the numbers with Uniform Accounting, we can see that Centene is making significantly more profit running Medicaid than one might expect.

With the exception of 2019, Uniform ROA has regularly been above 15% levels, as the company manages its costs, and like many others in the health insurance space, builds a baked-in margin with the investment income it earns from premiums.

Looking at Centene through the lens of Uniform Accounting, we can easily see that the Medicaid operator doesn’t suffer from the low-margin curse other government contractors might face.

Instead, Centene highlights that working for the government isn’t always the worst business to be in.

SUMMARY and Centene Corporation Tearsheet

As the Uniform Accounting tearsheet for Centene Corporation (CNC:USA) highlights, the Uniform P/E trades at 13.6x, which is below the global corporate average of 24.0x, and slightly above its historical P/E of 12.1x.

Low P/Es require low EPS growth to sustain them. In the case of Centene, the company has recently shown a 12% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Centene’s Wall Street analyst-driven forecast is a 36% EPS decline in 2021 and 68% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Centene’s $75.37 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to decline by 8% annually over the next three years. What Wall Street analysts expect for Centene’s earnings growth is above what the current stock market valuation requires in 2021, but below 2022.

Furthermore, the company’s earning power in 2020 is 3x above the long-run corporate average. Moreover, cash flows and cash on hand are nearly 6x its total obligations—including debt maturities and capex maintenance. All in all, this signals a low credit risk.

Lastly, Centene’s Uniform earnings growth is in line with peer averages, but the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research