This company is another beneficiary of Tesla’s failed robotaxi launch

Tesla’s stumble with its Austin robotaxi rollout has pushed back widespread autonomous taxi fleets for years, giving ride-hailing firms like Lyft (LYFT) breathing room.

Lyft is leaning into partnerships with AV developers instead of building its own self-driving cars, while bolstering its cash position through a FREENOW acquisition in Europe and a $750 million buyback.

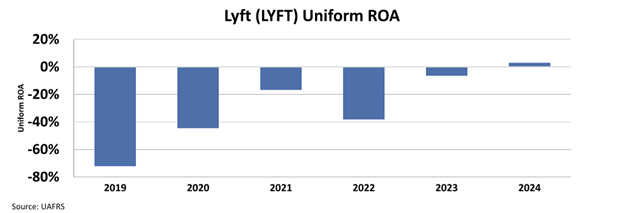

The company has turned the corner, generating positive free cash flow and Uniform ROA, and is focusing on margins and efficiency rather than top-line growth.

With Wall Street forecasting roughly 25% annual cash earnings growth and the market pricing in only modest ROA gains, Lyft looks undervalued relative to its long-term prospects.

Investor Essentials Daily:

Friday News-based Update

Powered by Valens Research

We discussed the effects of Tesla’s failed robotaxi launch in Austin earlier this week and how ride-hailing businesses like Uber could benefit from this.

When Tesla’s limited launch showed self-driving cabs still can’t handle real-world traffic without issues, it made clear that large-scale autonomous taxi fleets are still years off.

This delay presents a significant opportunity for established players like Lyft (LYFT), the second-largest company in the ride-sharing market.

The diminished immediate threat from autonomous technology creates a more stable demand environment for its core services, allowing the company to focus on strengthening its business fundamentals and competitive standing against its primary rival, Uber.

Lyft has been making strategic moves to solidify its market position for the long term. Rather than developing its own autonomous vehicle technology from the ground up, the company is pursuing a partnership-based approach with various autonomous vehicle developers.

This strategy allows it to integrate future technologies without bearing the full weight of research and development costs.

Furthermore, the company is actively expanding its reach, as seen with its recent acquisition of FREENOW in Europe.

This purchase provides an immediate foothold in several major European cities, offering a new avenue for growth outside of its established North American markets.

These actions, combined with a strong net cash position and a recently announced $750 million share buyback program, signal a company that is becoming more disciplined and focused on delivering shareholder value.

This strategic shift is reflected in its improving financial performance. After years of operating at a loss, Lyft has successfully reached a critical turning point, generating positive free cash flow and Uniform return on assets ”ROA”.

The company’s operating model is beginning to show the benefits of scale, with management successfully controlling operating expenses while growing its user base and the number of trips per user.

While its revenue growth may not match the pace of its larger competitor, the focus has clearly shifted towards profitability and margin expansion.

Wall Street projects that this focus on efficiency could drive cash earnings growth of around 25% annually over the next few years.

However, the market does not agree with the Street’s predictions and has concerns over how profitable the business can become.

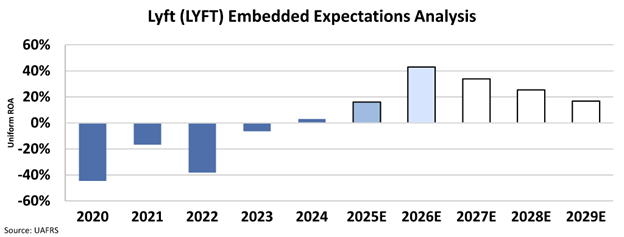

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market predicts that the company’s Uniform ROA will only rise to 17% from 2% last year, far below the 43% Wall Street projects.

The combination of a delayed autonomous threat and internal operational improvements presents a compelling case for the business.

While Uber still commands a larger market share, at approximately 76% of the U.S. market, Lyft has demonstrated it is a resilient competitor.

The key challenge ahead is to continue narrowing the performance gap with Uber.

If Lyft maintains its current trajectory of expanding margins and leveraging its network effect to attract and retain both drivers and riders, there is a clear path for its returns to scale toward the 35% levels that Uber currently generates.

Its current valuation appears discounted compared to its growth prospects, making it an interesting case for investors and even a potential acquisition target for technology companies looking for an immediate entry into the transportation market.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research