This company is benefiting from rising demand for orthopedic implants

As the population ages, the need for orthopedic care continues to rise, driven by a growing demand for knee and hip implants that help restore mobility and alleviate chronic pain.

Zimmer Biomet (ZBH) stands out as a leading maker of these implants, bolstered by surgeon trust, brand loyalty, and steady demand for reconstructive procedures that remain essential for patients’ quality of life.

Strategic acquisitions and investments in surgical robotics further expand its offerings, positioning the company for sustained growth despite concerns about potential changes in long-term demand from weight-loss drugs.

Its consistent performance, strong market position, and focus on innovation may lead investors to view the company more favorably over time.

Investor Essentials Daily:

Wednesday News-based Update

Powered by Valens Research

A growing number of people now rely on advanced knee and hip implants, driving spending in orthopedic care ever higher.

As the population ages, the need for reconstructive procedures is rising, and patients are seeking surgeries that can help them regain mobility and reduce chronic pain.

Surgeons increasingly trust reliable implants designed with long-term success in mind. At the same time, insurers are more willing to cover procedures that keep older adults healthier and less prone to further hospital visits.

Even with concerns about cost, these treatments offer tangible benefits for patients who might otherwise face limited activity or ongoing discomfort.

And this is where Zimmer Biomet (ZBH) comes in…

The company is a leading maker of orthopedic reconstructive products with a long history of staying profitable and defending its market position.

Orthopedic care typically sees steady demand, as many procedures are driven by health needs that rarely fluctuate with short-term trends.

Zimmer’s core business model and focus on reconstructive solutions like hips, knees, and other joint implants have kept it on solid ground over the years.

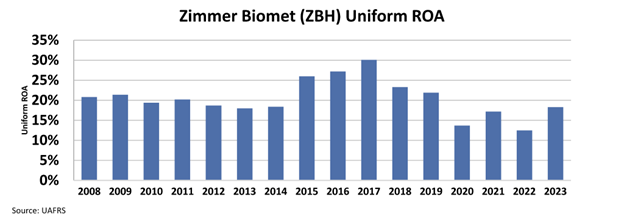

This resulted in the company sustaining a 19% Uniform return on assets ”ROA” historically.

Another reason for Zimmer’s success is its focus on surgeon trust and brand loyalty. Surgeons often work with the same products for years. They do so because they trust the reliability and proven results of these implants.

The company has nurtured these relationships by making high-quality devices that have a long record of success in the operating room.

This consistent track record helps it remain a top choice for hospitals and outpatient surgery centers around the world.

Over time, Zimmer has grown by both refining its existing product lines and acquiring other companies that complement its core offerings.

An example is the company’s recent move into foot and ankle orthopedics with a recent $1.2 billion acquisition of Paragon 28, which diversifies its portfolio beyond its signature knee and hip solutions.

Even though this move could take some time to show results, it has broadened Zimmer’s product scope and strengthened its ties to an aging population seeking relief from chronic pain and mobility issues.

Furthermore, innovation is another area where the company shines. In addition to producing traditional knee and hip implants, the company invests in areas like surgical robotics and smarter implant designs.

Robotics, in particular, is becoming more common in operating rooms as it adds precision and can improve patient outcomes by helping surgeons make more accurate cuts and alignments.

Zimmer’s product approvals and new releases keep it competitive and ready to meet evolving patient and surgeon needs.

Despite all these strengths, the market is concerned about how the rising use of weight-loss drugs could affect the need for joint replacements over the long run and the benefits of the company’s acquisition strategy.

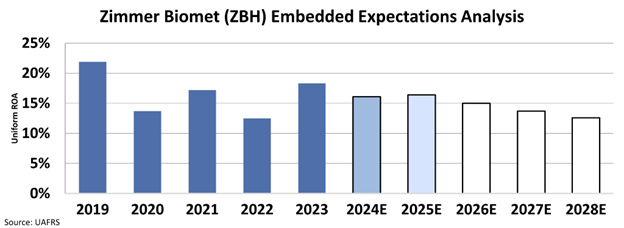

We can also see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market predicts that the company’s Uniform ROA will decrease to around 12% from 18% last year.

Zimmer benefits from stable demand in an environment where most joint replacement procedures are important for a patient’s quality of life.

Even if procedures are sometimes delayed, they are rarely canceled completely.

This makes the overall revenue picture less volatile than many other types of businesses, which in turn gives the company room to refine product lines or pursue acquisitions that strengthen its position.

While its stock price has not always moved in large swings, Zimmer’s consistent record and focus on growth may lead the market to view it more favorably over time.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research