This company delivers power to where it’s needed

Power demand in the U.S. is projected to reach record highs, driven by AI, data centers, and steady residential and commercial consumption, with further growth expected in 2025.

This has spurred significant investment in power infrastructure, benefiting companies like IES Holdings (IESC).

IES, a diversified electrical and tech system contractor, has grown through acquisitions and serves residential, communications, commercial, and infrastructure markets.

In 2024, IES achieved record profitability and strong growth across its segments, particularly in AI-driven communications and infrastructure.

Despite these achievements, the market undervalues IES’s potential, presenting an opportunity for investors to capitalize on its growth prospects.

Investor Essentials Daily:

Tuesday News-based update

Powered by Valens Research

The U.S. Energy Information Administration projected that power demand hit a new high of ~4.1 trillion kilowatt hours (kWh) in 2024, driven partly by the massive demand from AI and data centers.

The 1.0 trillion kWh for industrial customers brought demand to peaks not seen since the dot-com bubble.

That said, it’s not just AI that is so power-hungry. Residential demand hit 1.5 trillion kWh, in line with prior peaks. Commercial demand reached 1.4 trillion kWh, a new high. And the demand is not decreasing, with another 170 billion kWh projected to be added in 2025.

Unsurprisingly, the U.S. Bureau of Labor Statistics is projecting demand for electrical workers to skyrocket over the next decade, growing at a pace of 11%, nearly three times the overall job market.

Clearly, the U.S. wants more power, and to meet this demand, governments and corporations are going to need to continue to invest massively in power infrastructure.

Those companies set up to serve this investment look poised to win.

IES Holdings (IESC), or Integrated Electrical Services, got its beginnings 60+ years ago as a community-based electrical contractor.

Since then, through strong organic growth and smart bolt-on acquisitions, it has vastly expanded its geographical reach and capabilities to become a diversified electrical and tech system designer and installer.

Now, IES splits its billions in revenue into four segments; residential, communications, commercial & industrial, and infrastructure solutions.

In residential (48% of revenue), IES serves as a one-stop-shop for electrical, mechanical, and plumbing contracting needs for single and multi-family homes.

IES has ridden multi-decade tailwinds from homebuilding to scale this business and service large and complicated projects more ably than its smaller competitors.

In communications (27%), IES designs, builds, and maintains networking infrastructure for data centers, large technology companies, high-tech facilities and more.

This segment is well-positioned to capitalize on growth in AI, computing and storage project demand.

In commercial & industrial (13%), IES serves as an electrical and mechanical contractor for large projects brought on by a wide array of corporations.

Finally, in infrastructure (12%), IES’s fastest-growing and highest-margin segment, it acts as a specialized electrical and mechanical contractor for industrial operations, offering capabilities ranging from custom steel fabrication and power solutions to generator enclosures.

IES is well positioned to capitalize on power demand, regardless of end market

As it has scaled its capabilities, IES has been able to expose itself to more tailwinds across the power ecosystem.

Driven by massive investment in scaling data centers and AI, as well as a material re-investment in securing and replacing aging U.S. corporate infrastructure, IES saw an explosion of growth in 2024, with communications and commercial & industrial segments growing by ~30%, and its infrastructure solutions scaling by over 60%.

Even amid a tepid home construction market, given the immense fragmentation in electrical contracting, IES managed to pull off an impressive 9% sales growth in residential.

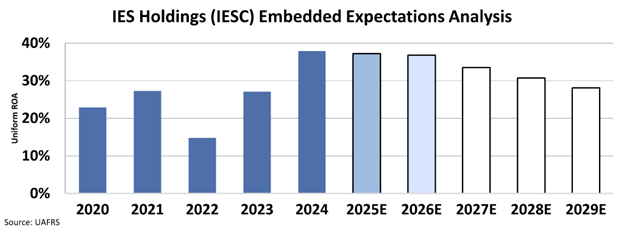

The company has leveraged its strong positioning across electrical contracting markets to achieve a record 38% Uniform return on assets ‘‘ROA’’ and 29% Uniform asset growth in 2024.

Despite strong profitability and impressive growth in recent years, and consistent improvements in its business capabilities over the past few decades, the market is not completely reflecting IES’s potential.

Our EEA model clearly shows this.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market predicts that the company’s Uniform ROA will fall to around 28% from 38% last year.

Trading below market averages at a 21.3x Uniform P/E, markets appear to be underestimating the firm’s improved ability to capture upside through cycles.

With more investment pouring into the power grid, IES can continue to grow rapidly, allowing it also to realize profitability benefits from economies of scale.

As such, IES appears to have upside potential and could be an interesting name to add to an investment portfolio.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research