This company is pulling ahead in the race for autonomous driving

The idea of fully self-driving cars is moving forward slowly rather than in one big leap, held back by cost, safety rules and public trust.

Real progress is happening in robotaxis and automated trucks, where companies are already testing and earning revenue in cities across the US and China.

Tesla’s rocky Austin launch handed Uber (UBER) an opening to expand its Waymo partnership into Atlanta, letting riders book autonomous rides through the Uber app without owning any cars.

By plugging tested Waymo vehicles into its huge global network, Uber can grow bookings and returns without the heavy costs that pure-play robotaxi operators face.

Investor Essentials Daily:

Thursday News-based update

Powered by Valens Research

The dream of a car that drives itself has captured our imagination for a long time. We picture a future where we can relax or work while our car handles the commute.

While that future is coming, it’s proving to be more of a gradual evolution than a sudden revolution.

The path to fully autonomous personal cars is a long one, slowed by high costs, complex safety regulations, and building public trust.

The real, immediate progress is happening in more focused areas like robotaxis and autonomous trucks.

These commercial services are already operating and expanding in major cities, particularly in the United States and China.

This is where the technology is being tested and proven in the real world, and where the first significant business opportunities are taking shape.

And companies are racing to be the first to adopt and deploy this new technology, but it’s not all smooth sailing…

One company’s misstep in the robotaxi race has opened a door for another. Tesla’s (TSLA) early launch in Austin hit public roadblocks, drawing scrutiny for erratic behavior.

Meanwhile, Uber (UBER) has quietly broadened its collaboration with Waymo, moving beyond its initial Phoenix pilot into a 65-square-mile area of Atlanta.

Riders there can now summon autonomous Waymo vehicles directly through the Uber app for both passenger trips and local deliveries, though the service still avoids highways and airport routes.

This steady, measured expansion has reassured investors that Uber’s path toward self-driving mobility is more sustainable.

Behind the scenes, Uber is leveraging assets it already owns. It has built a global network of 170 million active users in more than 30 countries, handling $160 billion in gross bookings last year and converting a 27% take rate into $6.8 billion of free cash flow.

Because it doesn’t need to buy its own fleets, Uber can plug Waymo’s vehicles and eventually those from other partners into its existing platform without heavy capital outlays.

That contrasts with the high tool-up costs faced by pure-play robotaxi operators, who must cover sensors, lidar and computer hardware at up to $150k per vehicle.

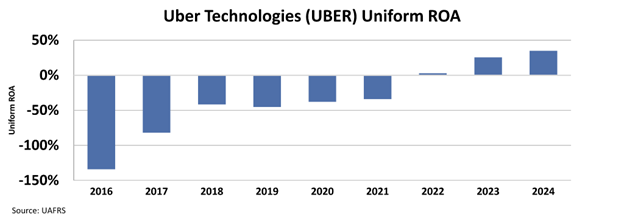

Profitability has already turned in Uber’s favor. After years of subsidies and market development, the company posted positive Uniform return on assets ”ROA” in 2022.

Its operating model leans on third-party drivers and carriers, keeping fixed costs low. As autonomous vehicles take on a larger share of rides, Uber stands to capture a revenue share without carrying the full burden of vehicle ownership.

Uber’s balance sheet flexibility is another draw. With rising free cash flow, the company can fund share buybacks or make small strategic acquisitions to deepen its technology stack.

Industry chatter even suggests that companies like Alphabet or Tesla could see Uber as an acquisition target.

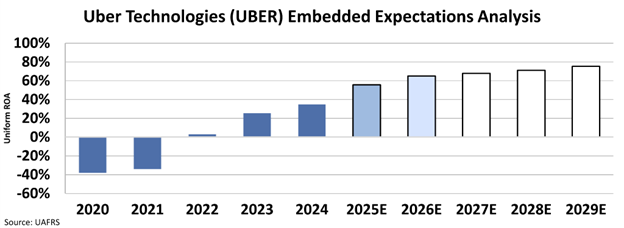

Wall Street forecasts project mid-teens growth in gross bookings and ROA to double in the upcoming couple of years and the market agrees.

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects that Uber’s Uniform ROA will rise to around 75% from 35% last year.

Competition remains fierce. Chinese firms such as Baidu and WeRide are testing robotaxis in select cities, while Tesla has publicly floated integrating its own autonomous fleet into Uber’s app.

But Uber’s deliberate approach, tying growth to fully tested Waymo vehicles, has so far sidestepped the public stumbles seen at rival pilots.

Regulatory approvals, safety performance and customer experience all favor a gradual rollout, and Uber’s partnerships give it room to pivot among technology providers as systems mature.

The market expects Uber’s ROA to rise as autonomous trips replace a growing portion of driver-led rides.

Every additional AV mile driven through the company’s app will boost utilization rates without corresponding increases in operating expenses.

That dynamic, combined with ongoing improvements in pricing, routing and customer retention, positions Uber to turn its competitors’ struggle into its own advantage and to lead the charge in commercializing self-driving mobility.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research