Consumer credit remains a question mark this holiday season… here’s why low holiday sales might not be a bad sign

With the holiday shopping season here, it’s important to look at consumer credit health. Given how volatile this year has been, some investors are worried about how consumer credit could affect holiday shopping.

Today, we will look at data regarding the consumer credit markets to see if there is anything to worry about.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

The holiday season is finally among us!

Just like many aspects of life this year, it looks different than usual. As this Forbes article about holiday shopping highlights, the whole holiday shopping landscape has been altered.

For starters, more shopping will be online than ever before. With many stores having limited in-store capacity or no in-person shopping at all, consumers are flocking to online shopping.

Online shopping has altered the shopping calendar too. With the surge of online orders, retailers and shipping companies anticipate delays as we get further on in the season. Companies have intentionally tried to extend the timeline. To aid consumer spending and help relieve some of the expected bottlenecks, companies started pulling Black Friday deals forward to as early as mid-October. The holiday deals have blurred with Black Friday deals.

Finally, despite retailers’ best efforts, spending is expected to be down across the season. Some folks will be spending normal amounts, but for others, it’s not financially feasible given the pandemic.

All these changes are making this holiday shopping season one to remember. It’s also bringing up questions about the health of the consumer and the effects that could have on spending.

Consumer spending makes up roughly 68% of GDP. Consumer spending is the backbone of the economy. These transactions have a ripple effect on business profits, taxes, and more. A small reduction in consumer spending can greatly alter both GDP and many sectors.

This means it’s critical to keep a pulse on consumer credit. The aggregate consumer credit profile can help us understand where the economy is heading.

A strong profile means consumers can return to normal spending faster once the pandemic ends. The less income spent repairing personal balance sheets, the more folks are buying into the economy. However, a weak profile would imply a delay in consumers returning to normal spending levels.

Consumer credit has been a topic of conversation more than usual during the pandemic. Investors were scared consumers would default on loans when unemployment rates skyrocketed.

However, as we highlighted over the summer, consumer credit was strong and left little to worry about.

Now, it is time to look again.

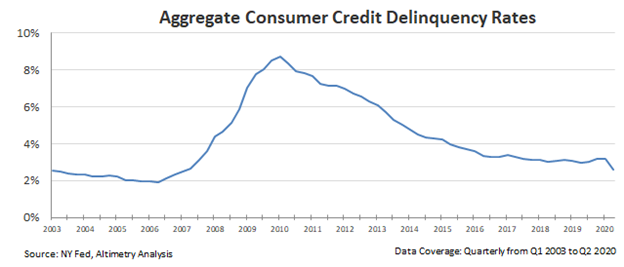

Overall consumer credit delinquency rates are down in 2020. This is something that would have been hard to predict when the pandemic began. This is a positive sign for financial markets and the economy.

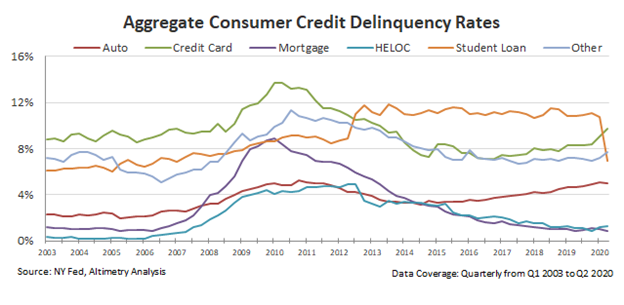

Looking into the data, we can see the fall in delinquency rates has not been uniform. Student loans, mortgages, and home equity loans and lines of credit (HELOC) have been the main causes for the improvement.

Mortgage and HELOC defaults have stayed depressed due to low interest rates. Expectations are for interest rates to stay low in the near future, which means the risk of these defaults rising are low.

Student loan defaults have fallen dramatically due to student loan forbearance. This has changed the interest on many student loans to 0% and suspended some payments. While these protections expire in 2021, this has helped keep delinquency rates low during this unique time.

Auto loan delinquencies are not declining, but have flattened out. The delinquency rate on auto loans consistently rose from 2014 to 2019. However, this year they have slowed their rise.

Credit card and other loan delinquencies have slightly increased this year. Although they have increased, it is important to note they are still well below historical highs. Credit card delinquency rates reached 14% in 2010, and are currently near 10%. This is a far better rate than what was seen in past recessions.

The overall picture of consumer credit is positive. The data shows aggregate delinquency rates have fallen. This means once society normalizes, consumers should have no problem resuming normal spending habits.

Compared to past recessions, the hangover may not be as bad and drawn out with this strong of a credit profile. This also means GDP growth could accelerate faster.

For all these reasons, we can remain bullish on the economy.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research