Consumer savings have dried up

In early August, U.S. unemployment rose to 4.3%, triggering recession fears and a market sell-off.

However, a later drop in jobless claims helped the S&P 500 recover some losses.

Despite mixed signals from the labor market, consumer spending remains crucial, but dwindling savings and rising debt have heightened the importance of income.

With savings exhausted and debt at record levels, any negative shifts in the job market could lead to a consumer-driven recession, making jobs data a critical economic indicator.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research.

To start August, U.S. job data for July showed that the unemployment rate had climbed to 4.3%, up from June’s 4.1%. This was near a three-year high and higher than estimates for unemployment to remain at 4.1%.

This triggered the Sahm rule—a reliable recession indicator—and investors panicked. The U.S. market lost more than $1 trillion in a three-day sell-off.

The slaughter ended with another jobs-related data announcement on August 8. Initial jobless claims for the week ending August 3 came in at 233,000—3.3% below expectations and 6.8% lower than the previous week’s number.

The S&P 500 recovered about 3% following the report, partially offsetting the market’s bloodbath at the beginning of the month.

This has left investors confused as some labor reports seem bad and some seem good.

Employment data has been the key driver of financial markets lately—more so than inflation statistics.

That’s because it’s now a more critical indicator of economic health than it has been in recent history.

The consumers are a major force in the U.S. economy, accounting for nearly two-thirds of GDP.

Consumer behavior and spending can either support economic growth… or tip us into a recession.

Consumer spending relies on two things: savings and income.

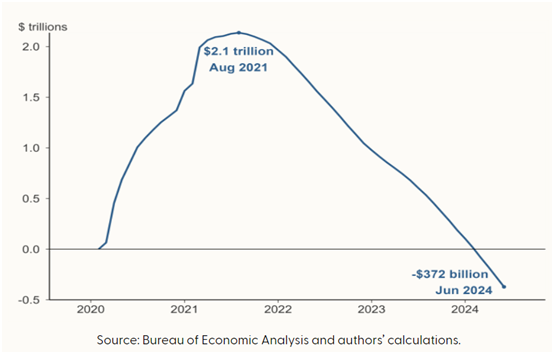

According to the Federal Reserve Bank of San Francisco, aggregate “excess savings” (meaning the extra savings people built up during the pandemic) peaked at $2.1 trillion in August 2021.

However, since then, households have been spending more than they’re saving, driving their excess savings down.

By September 2023, all pandemic-era savings had been exhausted. Yet that didn’t stop people from spending.

Fast-forward to June 2024. American consumers have $372 billion less in savings than they did at the beginning of the pandemic.

Take a look…

Remember: “excess savings” includes all savings that exceed the pre-pandemic trend.

So not only have we exhausted everything saved since 2020… household savings are now in a worse position than they were prior to the pandemic.

Over the past few years, consumers continued spending despite high inflation and high interest rates.

They had enough savings and almost everyone who wanted a job had one.

Now, household savings have dried up.

That means income is even more important in determining consumer spending. And income is directly tied to the health of the job market.

The labor market has been sending mixed signals. Unemployment is on the rise, though jobless claims haven’t yet reached alarming levels.

Households also have a record $17.7 trillion in debt as of the first quarter, up 1.1% from the fourth quarter of 2023.

Consumers are struggling to pay big expenses like credit cards and auto loans.

And with their safety cushion of savings gone and huge amounts of debt piling up, they may have to change their spending habits—and fast.

The Federal Reserve has been trying to reduce consumer spending to lower inflation.

However, if consumer spending shrinks more than necessary in the process, this might push the economy into a recession.

Right now, consumers only have their income to pay debt and fund their spending.

Any developments in the job market will be more decisive of the macro-outlook. Layoffs and fewer available jobs, for instance, would be devastating news for the economy.

So keep a close eye on jobs data, particularly on weekly jobless claims.

If they start to surpass expectations, it could signal a consumer-led recession is right around the corner.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research