CoStar Group is an economic powerhouse with attractive credit, but S&P has missed the story

While we spend most of our time at Valens looking at equities, we understand that it’s important to look at the credit universe from time to time.

This week’s credit highlight gives you a closer look at how we recommend bonds for the Valens Conviction Credit List.

Specifically, CoStar Group may offer investors attractive credit. Read on to learn why we like it.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

While stock analysis is core to what we do here at Valens, we know that to be good equity investors, we also have to be good credit analysts.

When looking at the capital structure for any public company, it’s always comprised of some blend of debt and equity.

Debtors always get paid first. That’s why it’s so important to understand companies from a credit perspective—if you don’t, you may be misvaluing equity without even realizing it.

Additionally, we understand that portfolio diversification is important. While we typically recommend our clients stay heavily invested in equities, bonds have their place in most portfolios too.

That is why our team monitors the corporate bond world for mispriced credit that may offer investors an attractive risk-adjusted fixed income return.

Yet so frequently, we find that the large credit rating agencies fail to understand why certain companies are far better credit than their official ratings imply.

Take CoStar Group (CSGP), for example. S&P rates it as “BB+”, which implies a 10% chance of default over the next five years.

Given that the company is at the crossroads of several long-lived business trends, this raised a few eyebrows on our team.

Specifically, CoStar’s real estate databases and analytics platform forms the backbone to many REITs’ decision-making processes. It also owns a portfolio of apartment listing companies such as Apartments.com that consumers have come to rely on for their renting search. Furthermore, the company records and distributes information about tenants, owns real estate auction platforms, and builds tools that help landowners manage and maintain their leases.

CoStar benefits heavily from the global digital transformation, where data and analytics have been and will continue to inform more and more of what companies do with their resources. The firm has loyal customers and may benefit in the future as the lull in urban office and apartment leasing ends.

Even a cursory glance at the company’s financials raises doubt about S&P’s rating. CoStar’s revenues have steadily doubled over the past five years and its Uniform earnings margins have been consistently improving. Moreover, the firm has a small debt position relative to its asset base.

Furthermore, the company is far more productive than most would realize. In 2020, even amidst severe challenges to the urban real estate and leasing businesses, CoStar was able to deliver 36% Uniform return on assets (“ROA”), although the more widely seen GAAP-based as-reported figures would only suggest 3% ROA, below the cost of capital.

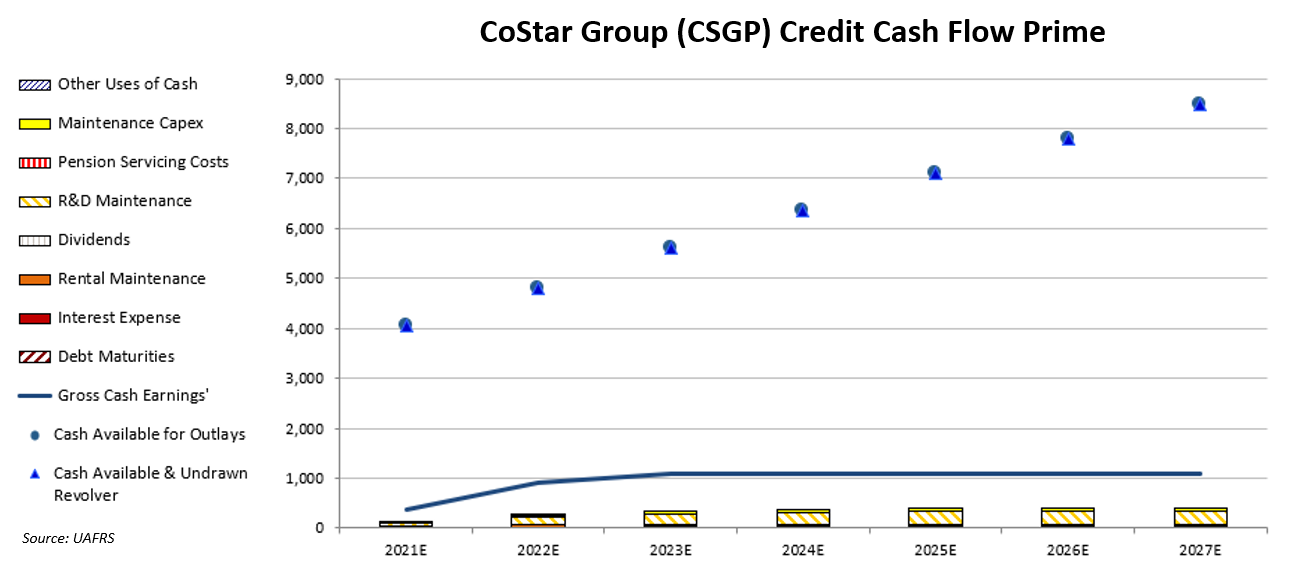

A closer look at its actual cash flows and obligations paints a much safer picture than S&P implies. Using our Credit Cash Flow Prime (“CCFP”) analysis tool, we can see that CoStar has no debt coming due in the next 5 years. The company does have a $1 billion maturity slated for 2030, but it is building a cash buffer large enough that creditors should have no concerns.

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

This CCFP demonstrates why CoStar group gets an investment-grade IG3+ rating, implying a chance of default in the next five years below 2%.

Specifically, the 2030 2.8% bond is mispriced by credit markets, with a yield-to-worst of 2.75%, while a fairer risk-defined intrinsic yield-to-worst would be 2.03%. This implies that credit markets are overstating risk, and investors can own the bond with an attractive risk-reward profile.

With a 2030 maturity, however, the investor may be exposed to more event risk than we typically recommend.

The Valens Conviction Credit List offers even deeper credit security analysis, and recommends bonds that mature between three and seven years from now, a goldilocks zone between value and time-based risk.

Investors looking for a safe place to store their money for the next five or fewer years should look no further than the Conviction Credit List. Learn about how to get access here.

SUMMARY and CoStar Group, Inc. Tearsheet

As the Uniform Accounting tearsheet for CoStar Group, Inc. (CSGP:USA) highlights, the Uniform P/E trades at 69.8x, which is above the corporate average of 24.3x and its historical P/E of 64.5x.

High P/Es require high EPS growth to sustain them. In the case of CoStar Group, Inc., the company has recently shown a 10% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, CoStar Group’s Wall Street analyst-driven forecast is for 87% EPS decline in 2021 followed by 26% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify CoStar Group’s $92.35 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 36% over the next three years. What Wall Street analysts expect for CoStar Group’s earnings growth is below what the current stock market valuation requires in 2021, but above that requirement in 2022.

Furthermore, the company’s earning power in 2020 is 6x the long-run corporate average. Moreover, cash flows and cash on hand are 16x its total obligations—including debt maturities and capex maintenance. However, intrinsic credit risk is 40bps above the risk-free rate. All in all, this signals a low dividend but moderate credit risk.

Lastly, CoStar Group’s Uniform earnings growth is below peer averages, while the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research