Many consumer staples like soup are overlooked by investors, giving diligent investors an edge

Soup has long been the go-to food for people feeling under the weather. As the pandemic continues to accelerate, we will likely be in for a rough winter of sickness. Today’s firm makes arguably the most famous soup in the world.

Looking at as-reported numbers, it appears today’s firm generates declining and below cost-of-capital returns. Digging deeper into the numbers, we can see the firm has stronger profitability than the market thinks.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

We are seeing a surge in the coronavirus pandemic right now and cases have recently crossed the 150,000 mark per day for the first time.

Some of these increases can be attributed to more testing nationwide. Mostly, it’s clear we’re facing a genuine second wave across the country.

As we head into the flu season, the second wave is going to put the healthcare system under especially high stress. Hospitals are quickly filling up and exhausting their resources. If they have to cope with both flu patients and coronavirus, it might push them past the edge.

The flu and coronavirus carry similar symptoms, making things particularly tough. It will be difficult to tell whether someone has one or the other until they are tested.

For those who only get mildly sick this winter, they will turn to a different kind of treatment–hot soup. Campbell’s Soup Company (CPB) is a processed food and snack firm that has brands like Pepperidge Farm, Synder’s, V8, and other products under its umbrella.

However, the firm is most famous for its Campbell’s Chicken Noodle Soup, which has become a staple for people who are feeling under the weather.

During the early stages of the pandemic, Campbell’s business thrived. People were looking to stock up on non-perishable goods, which the company has in spades. Q2 sales were up 18% year over year.

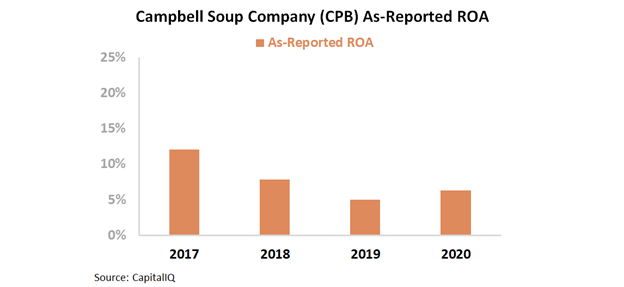

One might expect a household name like Campbell to have strong profitability. However under GAAP accounting, returns have struggled.

Looking at as-reported return on assets (ROA), the firm has cost-of-capital returns at best. As-reported ROA has fallen from 12% in 2017 to just 6% in 2020.

It appears Campbell’s 2018 acquisition of Snyder’s-Lance, a giant in the snack space, has been value destroying. Despite Campbell’s market leading position, it has appeared to generate below-average returns.

However, this picture of Campbell’s performance is not accurate. This is due to distortions in as-reported accounting, including the treatment of interest expense and goodwill, among other distortions. Wall Street has missed Campbells’s profitability.

Campbell’s Uniform ROA has been at least double as-reported numbers in every year since the 2018 acquisition. Uniform ROA was 22% in 2020, compared to 6% for as-reported ROA.

While as-reported metrics show declines since 2017, Uniform Accounting reveals the opposite. Uniform ROA has risen from 12% in 2017 to 22% in 2020.

Campbell’s diversification into snacks through Snyder-Lance has led to an ROA expansion. The business is less dependent on its soup brands and has grown its addressable market.

Without Uniform Accounting, investors would miss the strong returns of this consumer staples company as they might see Campbell as a firm with declining returns instead of robust profitability.

Ultimately, this company has been growing returns since its 2018 acquisition of Snyder’s-Lance. Additionally, as people buckle down for a harsh winter, Campbell will likely benefit from increased spending on perishable goods.

SUMMARY and Campbell Soup Company Tearsheet

As the Uniform Accounting tearsheet for Campbell Soup Company (CPB:USA) highlights, the Uniform P/E trades at 22.0x, which is around the global corporate average valuation levels and its historical average valuations.

Average P/Es require average EPS growth to sustain them. In the case of Campbell, the company has recently shown a 5% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Campbell’s Wall Street analyst-driven forecast is a 7% and 6% EPS shrinkage in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Campbell’s $49 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow 1% per year over the next three years. What Wall Street analysts expect for Campbell’s earnings growth is way below what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 4x the long-run corporate averages. However, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Altogether, these signals high credit and dividend risk.

To conclude, Campbell’s Uniform earnings growth is in line with its peer averages, and the company is also trading in line with its peer average valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research