This credit card company’s latest move comes with a catch

American Express (AXP) is overhauling its Platinum Card with expanded perks and lounge access in its biggest card update ever.

The move aims to fend off rising competition from JPMorgan and Capital One.

While Amex has outperformed with strong returns and a premium brand, the market now expects even higher profitability.

With rising costs and tighter competition, those expectations may be hard to meet.

Investor Essentials Daily:

Thursday News-based update

Powered by Valens Research

American Express (AXP) is going all-in on its premium perks.

The credit-card giant just unveiled a sweeping update to its Platinum lineup, calling it the “largest investment ever” in a card refresh.

The overhaul affects both the personal and business versions of the Platinum Card, its flagship offering for high-spending customers.

These changes won’t just be cosmetic. Amex is expanding Centurion Lounge access, with new outposts in Tokyo, Salt Lake City, and Newark, and revamping the card’s travel benefits, concierge services, and branded offers.

It’s a direct challenge to rivals like JPMorgan’s (JPM) Sapphire Reserve and Capital One’s (COF) Venture X. Those competitors have been luring away younger, more travel-savvy customers with flexible points and simpler perks.

So, Amex is upping the ante to hold its ground at the top of the premium market.

The company has been one of the market’s quiet winners. Its shares have doubled in the past two and a half years, beating the broader S&P 500. And that outperformance has come not from wild innovation, but steady execution.

Its core strategy has been consistent. Raise annual fees, add travel perks, and expand exclusive rewards partnerships.

Each wave of upgrades helped it retain customers, grow fee revenue, and deepen spending behavior.

It’s been a smart way to differentiate in a commoditized space. Most cards focus on cash back or simple travel points.

Amex turned its product into a lifestyle brand, one built around prestige, experiences, and concierge-like service.

That positioning has helped it dominate the premium market. It also allowed the company to weather economic slowdowns better than its peers.

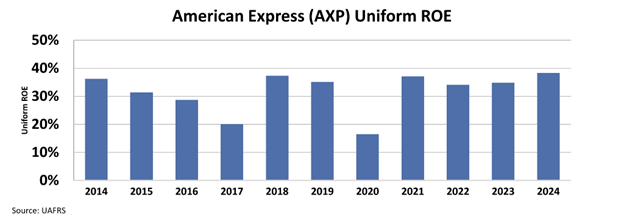

Excluding the underperformance in Covid, Amex’s Uniform return on equity (“ROE”) has been stable at above 35% in the last five years.

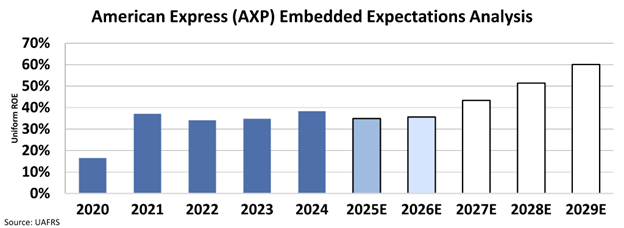

However, after years of outperformance, investor expectations have caught up…

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

Analysts expect the company’s performance to stay at around the same levels over the next two years. However, the market thinks Amex’s Uniform ROE will reach 60% by 2029.

Take a look…

The market is pricing in a significant improvement in profitability, even as competition tightens and consumer pushback on fees grows louder.

Card updates like this one often look great on paper.

They make headlines, attract media buzz, and reinforce Amex’s premium brand. They also tend to come with fee hikes, which boost top-line growth, assuming customers stick around.

But these moves aren’t cheap. Lounge expansion alone involves major capex and long-term leases. And elevated customer acquisition costs are already a drag on margins.

At the same time, competitors have closed the gap. Venture X’s annual fee undercuts Amex by nearly half while still offering lounge access, travel credits, and strong cashback features. Sapphire Reserve is similarly positioned and has broader merchant acceptance.

Amex can’t afford to slip. Premium customers are loyal, until they’re not.

That’s what makes today’s valuation so risky. The market is pricing in continued dominance, as if execution will remain flawless. But even a modest stumble could unravel that confidence.

Investors should be cautious.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research