Credit health matters, even for equity investors

Avnet’s (AVT) apparent cheap valuation masks a looming credit crunch.

A heavy debt repayment schedule over the next few years means free cash flow won’t cover obligations without refinancing or asset sales.

Refinancing at today’s rates would spike interest costs, while asset sales could erode higher-margin services.

Credit headwalls threaten to sap profitability long before any market recovery.

Investor Essentials Daily:

Friday News-based Update

Powered by Valens Research

When using our EEA tool, it’s easy to spot companies that look cheap at first glance. But often there’s a solid reason behind an apparently low price.

The EEA starts by looking at a company’s current stock price.

From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

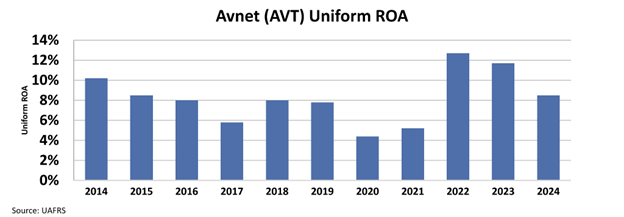

Avnet (AVT) posted a healthy 13% Uniform return on assets ”ROA” in 2022.

That’s fallen to about 9% last year, and the market now expects profitability to collapse over the next five years.

That skepticism isn’t born from thin air; it reflects very real concerns about the company’s upcoming debt obligations.

Digging into Avnet’s credit structure makes the market’s pessimism easier to understand.

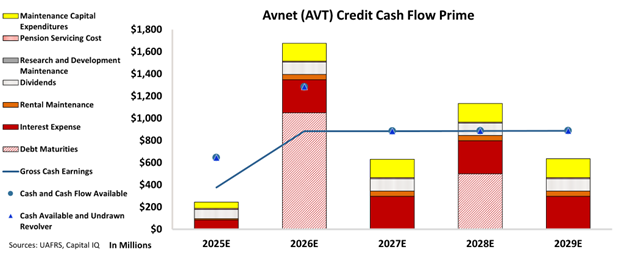

If you map out the timing of the company’s debt maturities, known as debt headwalls, you see a busy stretch of repayments looming in the next few years.

Our Credit Cash Flow Prime (CCFP) shows that Avnet will struggle to generate enough free cash to cover all its obligations without taking drastic steps.

When a business faces that kind of squeeze, the fixes typically hurt profitability.

Refinancing or selling assets all come with costs that flow straight through the income statement.

On the surface, signs of industry recovery are a reason for optimism. Distribution companies tend to rebound when electronics spending picks up.

Quarterly revenue in Asia has seen year-over-year gains for two straight quarters. Design activity in Asia remains healthy, suggesting future order flow, which is a plus for Avnet’s volume‐driven model.

But those positives sit alongside weaknesses in the Americas and Europe, which fell by double digits in the latest quarter.

Management still sees negative growth ahead in North America and EMEA, even in a seasonally strong period.

Even if the top line recovers, the real hurdle is leverage.

Refinancing large debts at today’s interest rates would raise interest expense and squeeze net income.

If the company opts for asset sales to boost liquidity, it risks losing parts of its higher-margin services business.

Avnet’s situation illustrates why credit health matters, even for equity investors.

Surface metrics like price-to-earnings can miss the drag from looming debt repayments and underappreciated leverage risk can turn an attractive valuation into a serious pitfall.

In Avnet’s case, apparent cheapness hides a refinancing challenge that could hold returns down for years.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research