Don’t listen to Wall Street—Salesforce has mastered the SaaS sales model

In the late 1990s and early 2000s, a wave of investor enthusiasm over the growing internet economy pushed scores of companies, many of which did not generate a single dollar of revenue, to multi-billion dollar valuations.

Once the true nature of many of these businesses was revealed, investors were left with the resulting market slump.

Fears of a similar boom and bust have gripped Wall Street once again over the past year, yet those spreading this narrative have long gotten it wrong.

Today, we’ll use Uniform Accounting to highlight how distortions inherent to as-reported metrics can mislead investors into dismissing high-growth technology names as unprofitable hot stocks reminiscent of the Dot-com era.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Last March, we published a Forbes article highlighting how wrong Wall Street gets many of the most popular companies in the world.

We specifically looked at Goldman Sachs’ (GS) “Non-Profitable Technology Index,” a list of companies the investment bank claims make no money, despite the fact their stock prices have surged to dizzying heights.

The narrative behind Goldman Sachs’ index back in March was that the surge in high-growth technology names made little sense because the included companies generated no profits, at least according to as-reported metrics.

At the time, we highlighted how in reality many of the businesses on the list were, and still are, quite profitable. It’s only a matter of looking at the right numbers.

A case in point is Salesforce (CRM). The cloud computing solutions business didn’t end up on Goldman’s unprofitable list, but only just.

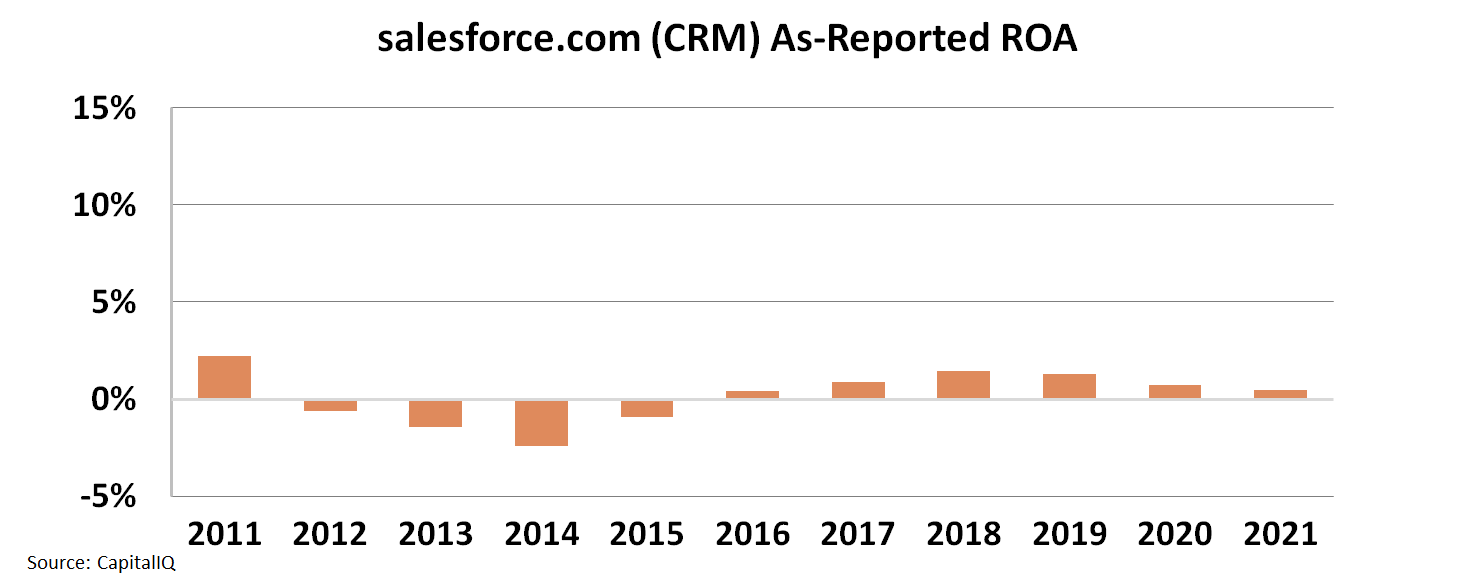

Looking at the $300 billion software-as-a-service (“SaaS”) giant’s as-reported return on assets (“ROA”), it looks like Salesforce hasn’t seen its profitability rise above 3% a single time over the past decade.

Want to make sure you’re invested in the right companies heading into 2022? Don’t forget to tune into our 2022 market prospective webinar this Thursday, November 18th at 12pm ET. We’ll be covering everything you need to know to confidently invest to beat the market next year.

This suggests that the firm operates below its own cost of capital, a recipe for economic value destruction.

Based on this lackluster performance, it’s no wonder Wall Street has been throwing up their hands on similar names in the software industry.

The issue though is that there are incredible complexities involved in software accounting.

From revenue recognition and M&A adjustments to accounting for stock option expenses, these bookkeeping issues substantially distort how profitable software businesses like Salesforce and its up-and-coming peers truly are.

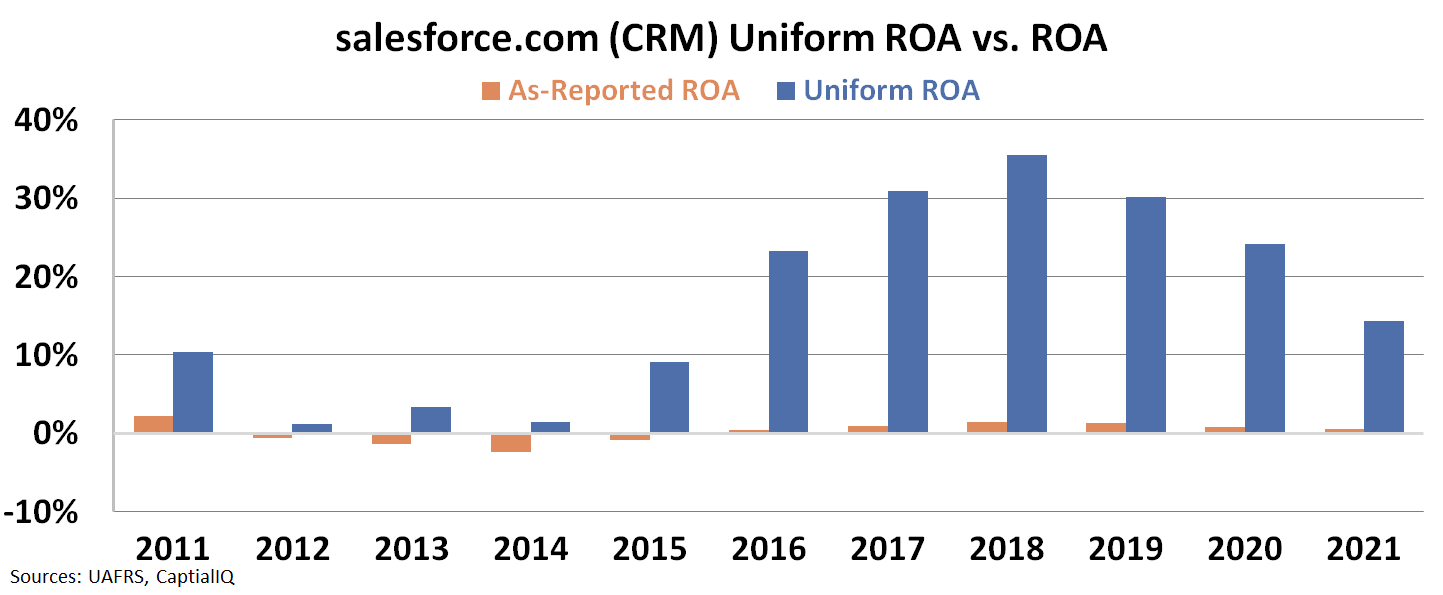

In reality, when we take a look at Salesforce using Uniform Accounting metrics, we can see that the company’s Uniform ROA has been consistently in the double digits since 2016. Moreover, the firm has been able to massively compound these high levels of profitability with strong growth.

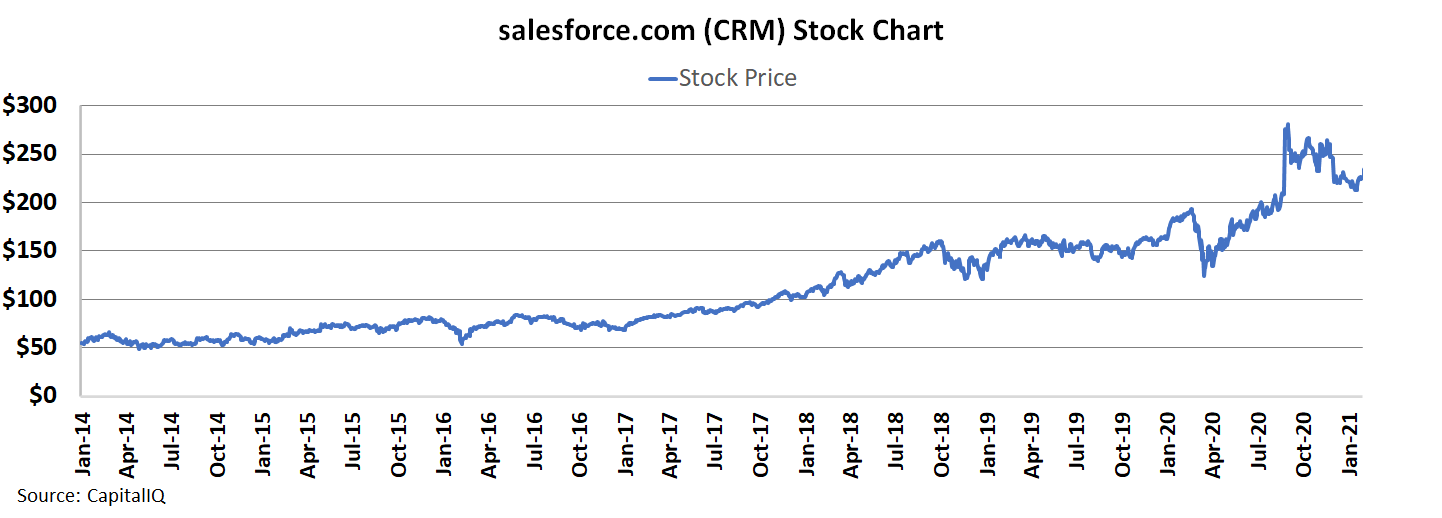

When putting these pieces together it becomes clear why Salesforce’s stock has been on such an incredible run since 2015.

Uniform Accounting metrics could not more clearly highlight the issues inherent in the generally accepted accounting principles (“GAAP”) relied upon by Wall Street.

It’s easy to miss out on winning stocks when they look just like the duds using as-reported accounting. Make sure to start 2022 on the right foot by using accurate financial data. Tune into our 2022 prospective webinar to learn more about Uniform Accounting and our top ideas for next year. Click here to register.

When looking at the real numbers, it’s clear that Salesforce and many of the other software names on Goldman Sachs’ “unprofitable” companies index have been surging in value because they’ve benefitted immensely from the shift towards technology during the pandemic.

It’s only the arbitrary and often nonsensical nature of accounting standards that make them appear to be unprofitable businesses riding a speculative mania like that of the dot-com era.

Going forward, investors looking at the companies of the future need to bear in mind the difference.

SUMMARY and salesforce.com, inc. Tearsheet

As the Uniform Accounting tearsheet for salesforce.com, inc. (CRM:USA) highlights, the Uniform P/E trades at 65.3x, which is above the global corporate average of 24.3x and its historical P/E of 50.9x.

High P/Es require high EPS growth to sustain them. In the case of salesforce, the company has recently shown a 23% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, salesforce’s Wall Street analyst-driven forecast is a 66% EPS growth in 2022 and a 2% shrinkage in 2023.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify salesforce’s $308 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 43% annually over the next three years. What Wall Street analysts expect for salesforce’s earnings growth is above what the current stock market valuation requires in 2022, but is below that requirement in 2023.

Furthermore, the company’s earning power in 2021 is 2x the long-run corporate average. Moreover, cash flows and cash on hand are 3x its total obligations—including debt maturities and capex maintenance. All in all, this signals a low credit risk.

Lastly, salesforce’s Uniform earnings growth is above peer averages, while the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research