2020, the year of…foam clogs?

Early on in the pandemic, lockdowns sent most students and workers packing from the office or the classroom.

Without having to face professors or colleagues in person, many resorted to ditching work attire for something a bit more comfortable, especially given that in the age of Zoom calls, all one can see are the head and shoulders.

Nevertheless, as-reported metrics fail to capture just how skillfully this footwear provider was able to leverage its unique brand to generate high returns during this unusual period.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

On July 1, 2020, it was difficult to say what single topic would define the year.

It was the “year of” COVID, the first recession in the U.S. in over a decade, the so-called At-Home Revolution, Bitcoin, the presidential election, and seemingly so much more.

Yet, what most people would have never predicted was that 2020 would end up being the year of something far more casual…Crocs.

Made by Colorado-based Crocs, Inc. (CROX), the famous foam clogs witnessed a stunningly successful revival in 2020 due to a clever branding strategy and well-placed marketing initiatives.

These included special release launches in collaboration with the companies like KFC, with whom they created fried chicken-themed clogs with chicken-scented accessories, and celebrities like Post Malone, Justin Bieber, and even celebrities in China.

With people stuck at home and spending more time thinking about wearing comfortable shoes—and less about what they’ll wear to work—these efforts struck the right chord, elevating Crocs high onto the radar of consumers around the world.

Such a pop-culture resurgence seems like exactly what Crocs needed. The company could barely keep its shoes stocked on shelves when they first came out in the early 2000’s, but since then, their reputation became closely aligned with small children and occasionally as house shoes for their parents.

For the first time in years, Crocs was relevant again.

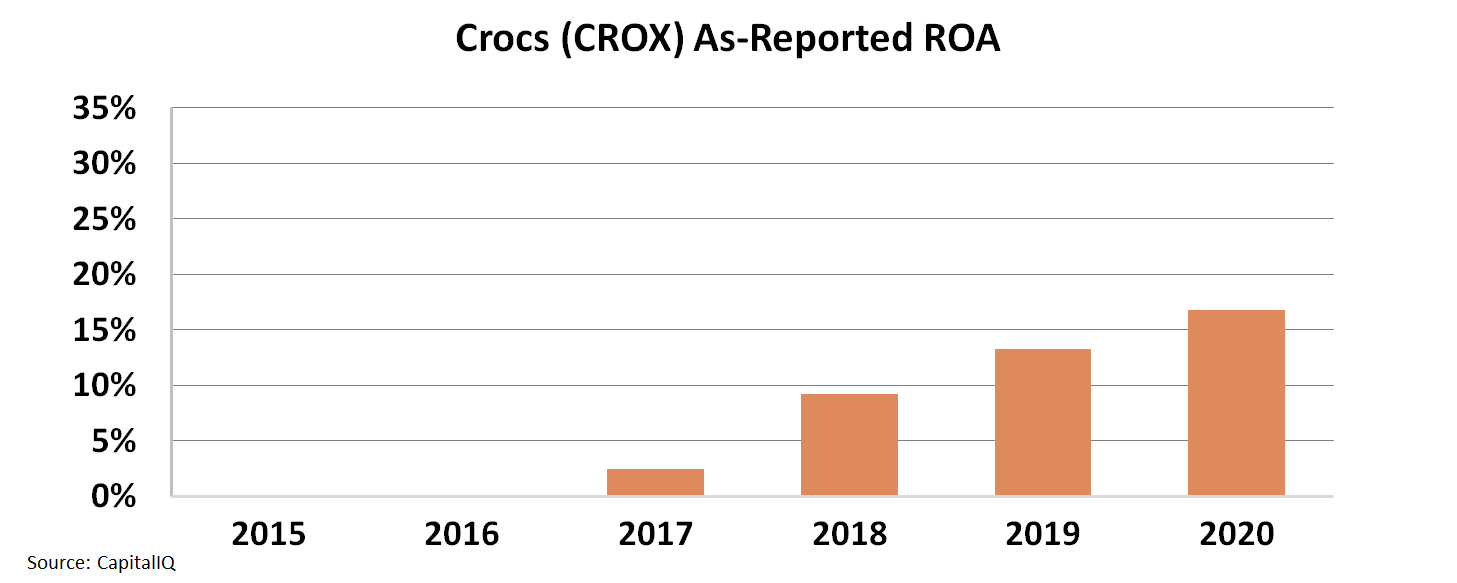

Despite this success, looking at as-reported metrics it appears Crocs’ profitability barely improved from 2019 to 2020, with ROA only rising from 13% to 17%.

Not the huge jump one might expect when a company takes over social media attention by storm. In fact, these returns are still less than half of what they were back in 2006.

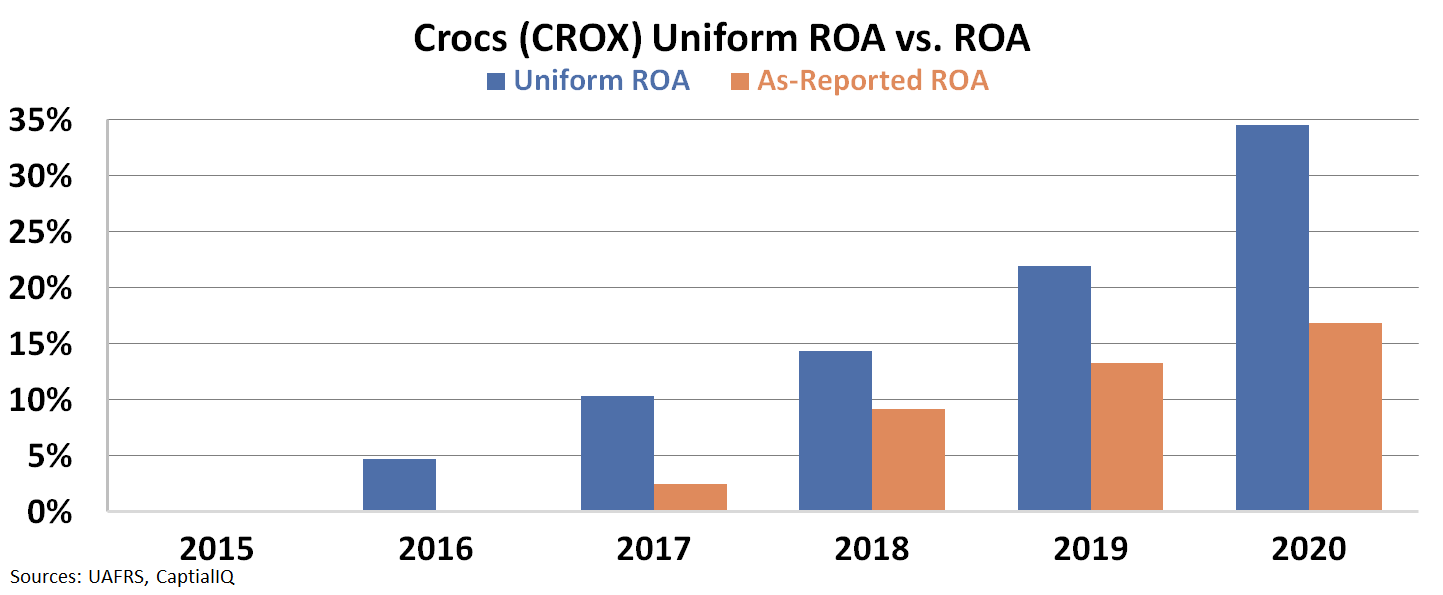

The reason for this disconnect is quite easy to understand for those in the know on how as-reported metrics fail to reflect the true story behind a business.

That’s why we focus on economic reality.

Removing inherent accounting distortions around line items such as operating leases and special line items, we can see that Uniform ROA actually rose from around 20% in 2019 to 35% in 2020.

This is a much more pronounced increase than as-reported metrics suggest, continuing a strong trend in returns that bottomed out at around 0% in 2015 and is now more than triple corporate averages.

Taking advantage of the shift to more time spent at home and online, Crocs has cleverly leveraged its unique brand to achieve high returns.

Other businesses may want to heed a lesson or two from the foam clog maker’s playbook. And yet, the lesson may be lost if corporate strategists were only using as-reported accounting.

SUMMARY and Crocs, Inc. Tearsheet

As the Uniform Accounting tearsheet for Crocs, Inc. (CROX:USA) highlights, the Uniform P/E trades at 15.7x, which is below the global corporate average of 21.9x, but above its historical average of 12.4x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Crocs, the company has recently shown a 107% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Crocs’ Wall Street analyst-driven forecast is an EPS growth of 159% in 2021, followed by a 20% EPS decline in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Crocs’ $142 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 5% annually over the next three years. What Wall Street analysts expect for Crocs’ earnings growth is well above what the current stock market valuation requires in 2021, but below that requirement in 2022.

Furthermore, the company’s earning power is 3x the corporate average. Also, cash flows and cash on hand is 5x above its total obligations—including debt maturities and capex maintenance. This signals a low credit risk.

To conclude, Crocs’ Uniform earnings growth is above with its peer averages, but the company is trading below average peer valuations.

Best Regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research