This is the unlikely turnaround management story you don’t want to miss, but the rating agencies are!

While it may be difficult to take the shoes that Crocs (CROX) sells too seriously, apt investors are taking the firm and its textbook turnaround management story very seriously.

In 2021, CEO Andrew Rees’ hard work has paid off in a big way, with an explosion of new revenue and improving profitability. Read on to learn more about the story, and how some of Wall Street’s largest institutions are completely missing the story.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

In a turn of events that stunned many who thought they knew fashion, the Crocs brand made a strong resurgence during the pandemic.

For those who aren’t familiar with the shoe brand, Crocs (CROX) makes a clog-style shoe out of unique rubber-like material.

For decades, these colorful shoes were mostly viewed as an absurdity, other than by children and, unbeknownst to many, healthcare workers.

Indeed, it is a seldom-known fact that Crocs actually served a real, practical purpose to many nurses. But this was also the brand’s downfall through the late 2000s and early 2010s when it tried to adapt its shoes for practical use-cases like golfing.

Taking the brand away from its endearingly goofy stylistic roots caused the company to lose focus. But after a major restructuring in 2014 and the introduction of new CEO Andrew Rees, Crocs made a textbook turnaround.

Rees refocused the brand on its leisure roots, and made targeted efforts to improve its brand appeal and recognition by reintroducing fun ways to customize the shoes with “charms”. These charms slot right into the shoe’s famous holes, opening a world of possibilities for the goofy and creative.

In a footwear landscape dominated by Adidas and Nike, this gave Crocs a unique edge that especially appealed to teenagers.

But the floodgates really opened in 2019 when Crocs released its first celebrity collaboration with Takashi Murakami.

Since then, Crocs has released dozens of collaborations with the likes of Diplo, Post Malone, Justin Bieber, and even high-fashion brand Balenciaga.

The Balenciaga partnership was particularly successful. In a fashion world dominated by shock factor, nothing turns more heads than a pair of high-heeled crocs sold for $700. It’s a classic case of “all publicity is good publicity.”

Customers and potential branding partners are now more engaged with the brand than ever.

Hence, full-year 2021 revenue is slated to outperform 2020 and 2019 levels by roughly 60%. The business is also realizing significant scale advantages, seeing its Uniform margin steadily rise from immaterial levels in 2015 to a respectable 20% in 2020.

That has led Uniform return on assets (“ROA”) to expand from 0% in 2015 to 35% in 2020, an improvement trend that is showing no signs of slowing down.

Once again, it appears that the major credit rating agencies are slow to understand the story. Moody’s is rating the firm as a BB- name, which signals to potential creditors that there is a 10% chance of bankruptcy in the next five years.

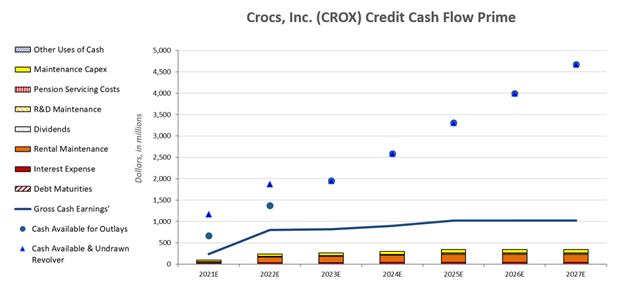

That is not reflective of the $10 billion powerhouse that the company has become. Let’s jump into the company’s Credit Cash Flow Prime (“CCFP”) to demonstrate the absurdity of the rating agencies’ pessimism.

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The estimates for future cash flows are based on Wall Street analyst consensus predictions, then adjusted to Uniform Accounting standards. Analysts are incredibly bullish on Crocs, betting that its story of acceleration has only just begun. But given the difficulty in predicting fashion trends, we have tempered Wall Street’s estimates down somewhat to show a more conservative scenario.

Take a look:

As you can see, even with tempered estimates, the firm should have no trouble using only its year-to-year profit from operations to finance its obligations. With no major debt maturities in the next seven years, it will be either building a massive cash position, or using its cash flows to invest in the business.

That should erase any concerns about defaulting on debt. We rate Crocs as an investment-grade IG3+, suggesting a sub-2% chance of default in the next five years.

Deep cash flow analysis doesn’t just matter to credit investors. It matters to equity investors trying to understand the future health of a company’s balance sheet.

With access to Valens’ research database, you can see CCFP for thousands of companies. Click here to learn more.

SUMMARY and Crocs, Inc. Tearsheet

As the Uniform Accounting tearsheet for Crocs, Inc. (CROX:USA) highlights, the Uniform P/E trades at 17.6x, which is below the corporate average of 24.0x, but above its historical P/E of 12.9x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Crocs, the company has recently shown a 107% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Crocs’ Wall Street analyst-driven forecast is for 178% growth in 2021 and 13% EPS decline in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Crocs’ $168 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 8% over the next three years. What Wall Street analysts expect for Crocs’ earnings growth is above what the current stock market valuation requires in 2021, but below that requirement in 2022.

Furthermore, the company’s earning power in 2020 is 6x the long-run corporate average. Moreover, cash flows and cash on hand are more than 5x its total obligations—including debt maturities, capex maintenance, and dividends. Additionally, intrinsic credit risk is 40bps above the risk-free rate. All in all, this signals a low credit risk.

Lastly, Crocs’ Uniform earnings growth is above peer averages, while the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research