Credit rating agencies are missing Cornerstone’s massive cash flows

Over the past two decades, the global economy has changed dramatically. No longer do energy conglomerates dominate lists of the world’s most valuable companies, being replaced long ago by producers of the world’s newest addiction: technology.

As a result, success in the digital age has become ever more dependent on talent, which means demand for recruiting and workforce development solutions will only continue to accelerate.

Yet, for one SaaS company that provides the intelligent solutions corporations depend on, the credit rating agencies rate its debt as high risk, which seems overly pessimistic given strong tailwinds in the space.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Just a few weeks ago we updated our insights on Uniform return on assets (“ROA”) for the U.S. in aggregate, something we do every few months here at Valens.

One of the big reasons we’ve seen a secular uptrend over the past 20 years is because of the mix shift in the U.S. from manufacturing businesses to technology and services providers.

For these asset-light firms, human capital (i.e., innovative talent) powers business through the software, processes, and service solutions it can create.

As recruiting (and retaining) top talent in engineering, business, and many other disciplines becomes more and more important for corporations, so too does managing it, which is why we’ve seen the success of platforms such as Workday (WDAY) that try to do just that.

Another firm that has been making successful forays into the marketplace is Cornerstone OnDemand (CSOD), which offers a software as a service (“SaaS”) model for workforce learning and development solutions and now has over 6,000 clients and 75 million users.

The company provides an entire suite of end-to-end needs for people development, including recruitment solutions, training software, and performance analytics.

In fact, its solutions have gained significant traction, hence why as recently as 2020 Uniform ROA spiked to over 40% levels, an indication of the strength of demand for its services.

Despite these apparent tailwinds, credit rating agencies appear to be asleep at the wheel, unsure of how essential Cornerstone OnDemand’s tools are for businesses in the 21st century.

Moody’s for example rates the company’s debt as a B-, implying a 25% chance of going bankrupt over the next five years.

Based on the company’s valuable offerings in a booming space, we know Wall Street’s view of economic reality makes little sense, but a deeper look at our Credit Cash Flow Prime (“CCFP”) analysis, which is able to get to the heart of the firm’s true credit risk, further confirms how overstated rating agency concerns are.

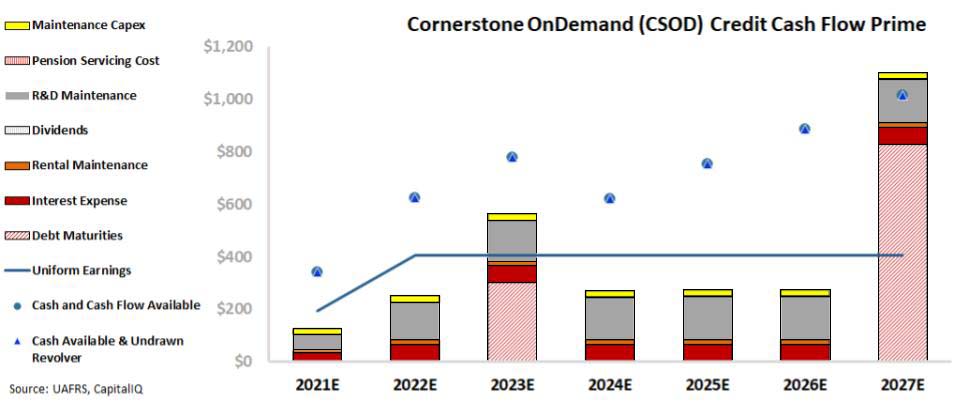

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As depicted, Cornerstone OnDemand’s cash flows plus cash on hand significantly cover all of the firm’s obligations going forward, including significant R&D investments that fuel growth. Meanwhile, the company lacks any substantial maturing debt over the next five years, suggesting it will have plenty of space to meet its obligations.

Rather than a distressed credit, Cornerstone OnDemand is actually in a quite comfortable cash position, boosted by strong tailwinds in the workforce solutions space. This is why Moody’s speculative B- rating, with a 25% risk of default expectation, seems to be missing the point.

Hence, Cornerstone’s Valens credit rating is an IG4, which implies a 2% change of default.

Ultimately, Uniform Accounting and the Credit Cash Flow Prime analysis highlight how Cornerstone OnDemand’s credit risk profile is much safer than what rating agencies believe, especially when considering the future of corporate talent management.

SUMMARY and Cornerstone OnDemand, Inc. Tearsheet

As the Uniform Accounting tearsheet for Cornerstone OnDemand, Inc. (CSOD:USA) highlights, the Uniform P/E trades at 30.7x, which is above the global corporate average of 24.3x, and its historical average of 25.3x.

Low P/Es require low EPS growth to sustain them. In the case of Cornerstone, the company has recently shown a 39% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Cornerstone’s Wall Street analyst-driven forecast is an EPS decline of 32% and 1% in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Cornerstone’s $57.31 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 5% annually over the next three years. What Wall Street analysts expect for Cornerstone’s earnings growth is below what the current stock market valuation requires in 2021, but above the requirement in 2022.

Furthermore, the company’s earning power is 9x the corporate average. Also, cash flows and cash on hand are nearly 2x above its total obligations—including debt maturities, and capex maintenance. This signals a moderate credit and dividend risk.

To conclude, Cornerstone’s Uniform earnings growth is below its peer averages, but the company is trading in line with its average peer valuations.

Best Regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research