With a 13x as-reported P/E, investors may think this is a deep value commodity play, Uniform data shows a stronger company, but greater risks

While investors think all companies in the Aluminum business are commodity companies, this firm has been able to yield consistent returns and avoid commodity cycle uncertainty by focusing on high value-add markets.

While as-reported metrics make the name look like a weak-returning, deep value idea, TRUE UAFRS-based (Uniform) analysis shows that, as a result of its expertise, this company has been able to produce stable profitability and is priced for that to continue.

However, management appears concerned about their outlook. If the company was priced for weak performance, this wouldn’t be a concern. But Uniform numbers highlight much higher expectations and, therefore, downside risk.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Aluminum is the third most abundant element in the Earth’s crust. Over 55 million tons of aluminum are estimated to be produced in the world every year.

In contrast, annual gold production is only in the thousands of tons.

This discrepancy highlights a major difference between the two metals. Gold is a precious metal. Aluminum is a commodity. They serve different purposes and are viewed very differently in the marketplace.

Gold is often displayed prominently in jewelry and prestigious awards. It has been used as a currency and is often viewed as an extension of wealth. It was even the central driver behind one of the most significant events in American history: the Gold Rush of 1849.

Aluminum is not the same. You can find it in many daily-use items, such as aluminum foil, soda cans, and kitchen shears. Because of the commodity nature of the business, investors expect companies in the aluminum business to have low-returns.

In some respects, they’re correct. Aluminum smelting is an energy-intensive business and since there is no way to differentiate the raw commodity, producers must compete on cost.

However, there is another large, potentially lucrative portion of the aluminum market that may go underappreciated: processing and fabrication.

Although the metal itself may lack variety, aluminum’s end-uses are vast. The fabrication of the metal into these various products often requires a specific skill set, numerous patents and other intellectual property, and specialized equipment. This part of the aluminum business can be a high value-add.

Constellium SE (CSTM) was spun off from Rio Tinto’s Alcan business in 2010. It has made a name for itself in the aluminum business by focusing on high-value end markets.

Aluminum is a versatile material; it can be lightweight, strong, and corrosion-resistant. As such, it has become a trusted component in many expensive products. In particular, it is a crucial part of many products that need a high level of safety.

Instead of being tied to the commodity cycle, Constellium has differentiated itself by adapting to the ever-changing demands for aluminum, while focusing largely on supplying the automotive, aerospace, and defense industries, among others.

Its customers are household names: Mercedes Benz, BMW, Ford, Boeing, Airbus. The list goes on and on. The firm has seen great success and has become a global leader in its industry with over 100 years of experience.

However, despite its strong customer base, as-reported metrics paint the company to be a volatile, low profitability business, and investors using as-reported metrics may be misled about its historical success.

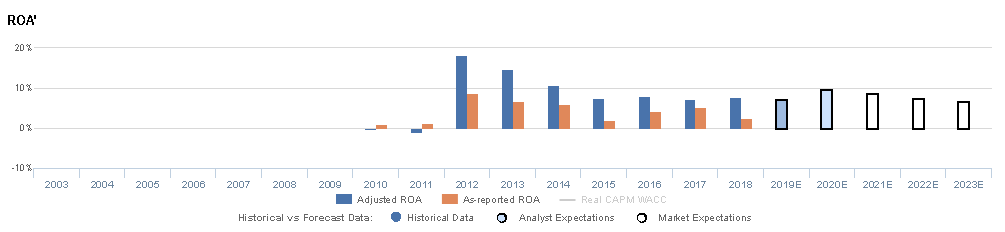

Return on assets (ROA) have declined from a peak of 9% in 2012 to a low of 2% in 2015, before bouncing back to 5% in 2017, and collapsing to a weak ROA of 3% in 2018.

However, Uniform Accounting indicates that as-reported metrics are understating Constellium’s profitability. Due to its expertise and good demand visibility, the firm has seen Uniform ROA stabilize at 7%-8% levels since 2015.

Investors appear to recognize Constellium’s stability and that as-reported metrics are artificially distorting the company’s performance. The firm currently trades at near-corporate average Uniform P/E levels of 19.2x, contrary to the as-reported P/E of 13.6x.

On an as-reported basis, investors might view Constellium as a declining-return business priced at low valuations by the market. A potential turnaround candidate and a value investor dream.

In reality, Constellium is a stable return business that the market understands—it’s priced for continued stability and growth. It’s anything but a turnaround or a value idea.

At its current stock price, the market expects Constellium to see Uniform ROA remain at 7%-8% levels through 2023, accompanied by steady 8% Uniform Asset growth.

That said, given growing customer uncertainty, driven by declining auto demand and issues with the Boeing 737 MAX, even stable expectations for Constellium may be too optimistic. Industry trends seem to be shifting for the firm in a negative way.

To add to this, management appears concerned about their working capital, Automotive & Transportation segment, and free cash flow. These raise major concerns about the company’s future and its ability to invest in accretive projects.

With potential weakness in its core segments and industry headwinds, stable market expectations may be too high.

If the company was priced like a deep value turnaround, like as-reported metrics imply, it might not be a risky investment. But once we see the real Uniform accounting numbers, it is clear it may be difficult for Constellium to justify current valuations, even with its expertise and value-add abilities.

Constellium SE Embedded Expectations Analysis – Market expectations are for slight Uniform ROA compression, and management may be concerned about their working capital, A&T segment, and free cash flow

CSTM currently trades near recent averages relative to Uniform Earnings, with a 19.2x Uniform P/E (Fwd P/E’).

At these levels, the market is pricing in expectations for Uniform ROA to decline from 8% in 2018 to 7% by 2023, accompanied by 8% Uniform Asset growth going forward.

However, analysts have bullish expectations, projecting Uniform ROA to expand to 10% in 2020, accompanied by 2% Uniform Asset growth.

CSTM was created in 2011 when Rio Tinto sold off Alcan Engineered Products to Apollo Management and FSI. Prior to the spinoff, the division struggled to generate positive profitability levels, with Uniform ROA ranging from -1% to 0%.

After becoming an independent company, CSTM saw dramatic improvements, with Uniform ROA jumping to a peak of 18% in 2012. However, this proved unsustainable as Uniform ROA fell to 7%-8% levels from 2015-2018.

Meanwhile, Uniform Asset growth has been consistent since the firm became an independent company, positive in each of the past seven years, while ranging from 6%-16%, excluding 76% growth in 2015 driven by the acquisition of Wise Metals. `

Performance Drivers – Sales, Margins, and Turns

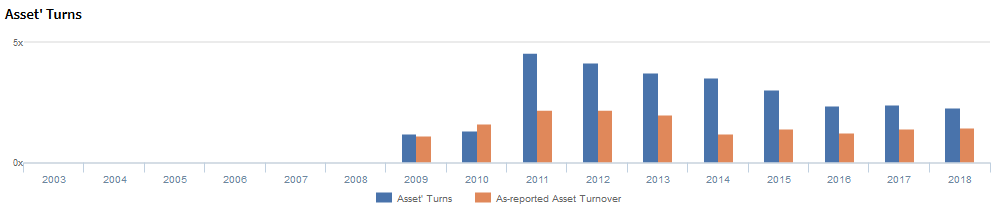

Trends in Uniform ROA have been driven mainly by fluctuations in Uniform Asset Turns and, to a lesser extent, Uniform Earnings Margin.

After the spin-off, Uniform asset turns jumped from 1.2x-1.4x levels in 2009-2010 to 4.6x in 2011, before fading to 2.3x-2.4x in 2016-2018.

Meanwhile, Uniform earnings margins jumped from negative levels in 2009-2011 to 3%-4% levels from 2012-2018.

At current valuations, markets are pricing in expectations for slight compression in both Uniform earnings margins and Uniform asset turns.

Earnings Call Forensics

Valens qualitative analysis of the firm’s Q3 2019 earnings call highlights that management may lack confidence in their ability to sustain recent performance levels in their A&T segment, and they may be concerned about the value of vertically integrating with their suppliers.

Furthermore, they may lack confidence in their ability to effectively manage their working capital, and they may be concerned about the sustainability of current free cash flow performance.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for CSTM than as-reported metrics reflect.

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight.

Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate CSTM’s asset efficiency, one of the key drivers of profitability.

For example, as-reported asset turnover for CSTM was 1.5x in 2018, significantly lower than Uniform Asset Turns of 2.3x, making CSTM appear to be at a much weaker business than real economic metrics highlight.

Moreover, as-reported asset turnover has understated Uniform asset turns in each year since the firm’s IPO, distorting the markets perception of CSTM’s historical asset efficiency.

SUMMARY and the Constellium SE Tearsheet

As our Uniform Accounting tearsheet for Constellium SE (CSTM) highlights, Constellium trades at a 19x Uniform P/E, roughly in-line with corporate average valuation levels and its recent history.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to our Uniform earnings forecasts. When we do this, we see that Constellium is forecast to see 8% Uniform EPS shrinkage in 2019, followed by 100% Uniform EPS growth in 2020.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify a $13 share price. These are often referred to as market embedded expectations.

In order to justify current market valuation levels, the company would have to have Uniform earnings grow by a modest 5% each year over the next three years.

As a result, Wall Street analyst expectations for Constellium’s earnings growth are far greater than what the current stock market valuation requires.

Meanwhile, the company’s earnings power is roughly in-line corporate averages, signaling that there is a moderate cash flow risk to the company’s operations and credit profile.

To conclude, Constellium is a company with average earnings power and near corporate average valuations, suggesting that embedded expectations are fairly moderate for the firm.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research