The pandemic forced the start of a new auto cycle in America, but rating agencies haven’t caught on yet

The pandemic forced a reset to the auto cycle in America, and it’ll be unlike any we’ve seen before.

Today’s company will likely succeed for the next few years as people continue moving out of cities, but the option to work from home might shorten the average American’s commute and put less wear on their tires.

Currently, the ratings agencies are showing a lack of understanding for this tire maker’s credit risk, rating it as a high yield name without looking at its fundamentals.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Thanks to the “At-Home Revolution” changing consumer habits, car ownership is once again on the rise. Many individuals and families have left cities to move into the suburbs for more space.

With this transition, many former city dwellers are forced to buy a car for the first time if they want to get around.

On the other hand, one of the major sources of road traffic is on the decline – the work commute. People are commuting to work far less than they used to.

Even though the number of cars is on the rise, road mileage hasn’t recovered yet.

Some investors may believe the entire car industry will do well due to the tailwinds of the At-Home Revolution. They are neglecting a sub-industry which makes revenue on miles driven, not cars sold.

Even though car companies may have a great few years in sales ahead, tire companies may struggle.

As fewer miles are being driven on each given car during the quarantine, companies such as Cooper Tire & Rubber Company (CTB) are facing significant headwinds.

Evidently, the rating agencies seem to buy the story that tire companies will struggle, as Cooper Tire is rated as a Ba3 name by Moodys. Cooper Tire is assigned a high yield credit risk, which carries more than a 10% risk of default in the next five years.

However, if investors avoid the hype and focus on fundamentals, they will be able to see why Cooper Tire is much safer than ratings agencies suggest.

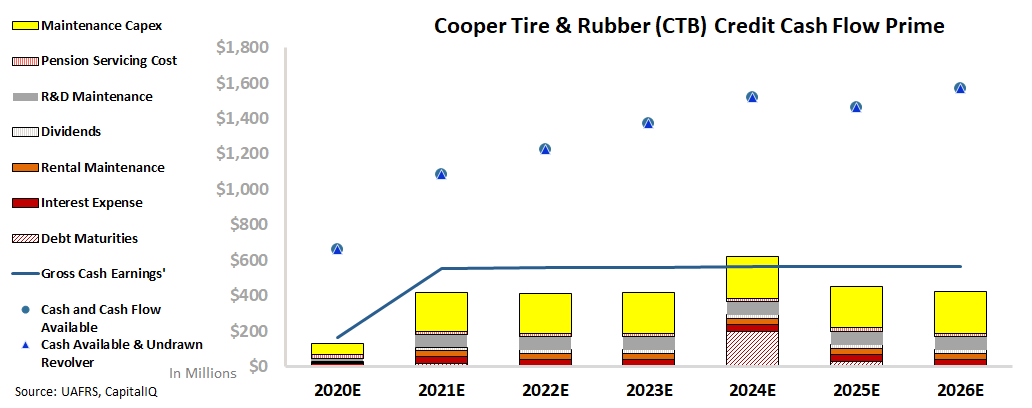

Our Credit Cash Flow Prime (CCFP) analysis is able to get to the heart of the firm’s true credit risk.

In the below chart, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As depicted, Cooper Tire has massive cash liquidity and therefore should have no issues handling its obligations going forward. On top of this, even if the firm did not have access to this capital, cash flows alone exceed all operating obligations by a wide margin every year including 2024, when the firm has debt maturities.

Cooper Tire’s cash flows currently exceed obligations by approximately 50% a year giving the company significant margin for earnings compression. Additionally, its cash on hand of $600 million is larger than its single $400 million debt maturity in 2024 .

Even if fundamentals are squeezed and cash flows drop by a third, the remaining cash flows alone would still match all obligations. This is before having to dip into any cash reserves.

Thanks to the firm’s strong asset backed recovery rate, it would have no issues refinancing its debt maturities in future years if need be.

Rather than a name in distress, Cooper Tire is actually a cash flow machine. Using the CCFP analysis, Valens rates Cooper Tire as an investment grade IG4+ safe credit rating.

This rating corresponds to a default rate of less than 2% within the next five years, a more realistic projection once a holistic understanding of the company’s risk is taken into account.

Ultimately, Uniform Accounting and the Credit Cash Flow Prime analysis highlights how Cooper Tire’s credit risk profile is much safer than what rating agencies believe. Despite a short-term constriction in cash flows, Cooper Tire & Rubber is secure from bankruptcy concerns.

By using Uniform Accounting, investors are able to match cash to operating obligations at a glance. Instead of being blinded by market trends, investors can turn to the numbers to get ahead on credit.

SUMMARY and Cooper Tire & Rubber Company Tearsheet

As the Uniform Accounting tearsheet for Cooper Tire & Rubber Company (CTB:USA) highlights, the Uniform P/E trades at 13.1x, which is below the global corporate average valuation levels and its historical average valuations.

Low P/Es require low EPS growth to sustain them. That said, in the case of Cooper Tire, the company has recently shown a 25% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Cooper Tire’s Wall Street analyst-driven forecast is a 17% and 18% EPS growth in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Cooper Tire’s $40.13 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 4% per year over the next three years and still justify current stock prices. What Wall Street analysts expect for Cooper Tire’s earnings growth is around what the current stock market valuation requires in 2020, but above that requirement in 2021.

Furthermore, the company’s earning power is below the corporate average. Also, cash flows and cash on hand are almost 3x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low dividend risk and moderate credit risk.

To conclude, CTB’s Uniform earnings growth is above its peer averages while trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research