Dropbox and its file-sharing services are much more profitable than many suspect

The rise of cloud computing has been massively accelerated by the pandemic and the shift to working from home.

For those that provide cloud solutions, demand has gone through the roof. Yet, for one company widely used for its popular file-sharing functionalities, as-reported metrics fail to capture the true story.

Today, we’ll use Uniform Accounting to uncover the company’s true profitability, highlighting how as-reported metrics can mislead investors’ perception of the bottom line for years at a time.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Cloud computing has quickly become a booming industry.

While many have been talking about its benefits for nearly a decade, for some businesses it truly took the pandemic and its ensuing disruption to get them transitioned to the cloud.

Whether it was for easy file sharing and collaboration purposes or increased data security reasons, the major shift to working from home created glaring capability gaps for many businesses that have yet to adapt.

One could call this one of the few bright spots over the past two years, namely because cloud computing offers such tremendous benefits for businesses of all sizes.

The ability to easily access on-demand computing power allows companies to quickly develop or integrate new software, receive automatic updates, and scale their businesses without spending massive sums on data infrastructure.

In other words, cloud computing enables companies to grow their businesses with ease while increasing both efficiency and profitability.

One would therefore assume any companies providing these services are benefitting immensely from greater adoption.

Yet, it appears that the COVID-19 inflection in the industry was only a lifeline for one of the earliest companies to offer cloud storage solutions, Dropbox (DBX).

Before the pandemic, the file-hosting company was consistently losing money on an as-reported basis, facing competition from tech giants like Google (GOOGL), Microsoft (MFST), and Amazon (AMZN).

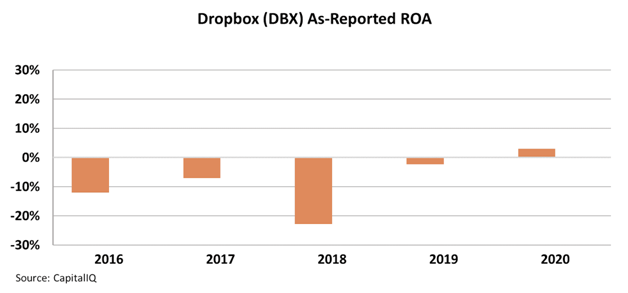

In fact, Dropbox’s as-reported return on assets (“ROA”) reached as low as -23% in 2018, before recovering to -2% in 2019 and inflecting positive for the first time in 2020.

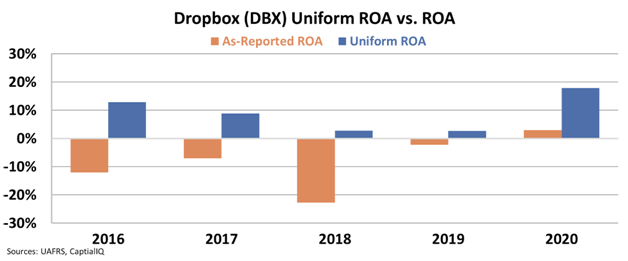

However, the reality is quite different, as a look through the lens of Uniform Accounting makes clear.

Corporate IT departments have long remarked that their employees continue to use Dropbox’s file-sharing services, no matter how many times they mandate employees use company-shared drives.

Dropbox’s user interface (“UI”) is more user-friendly and easier to learn than many others, which is borne out in the data. The firm’s Uniform ROA has been positive every year since 2016, despite as-reported metrics showing negative profitability.

Dropbox’s cloud storage solutions have taken on new life as the pandemic pushes more and more businesses to adopt cloud computing.

Yet the company’s recent profitability surge should come as no surprise to investors.

Uniform Accounting highlights that the company has been in the black for years, which makes much more sense. As often happens when you understand the fundamentals of a business, the as-reported metrics simply lead investors astray.

SUMMARY and Dropbox Tearsheet

As the Uniform Accounting tearsheet for Dropbox, Inc (DBX:USA) highlights, the Uniform P/E trades at 14.7x, which is below the global corporate average of 24.0x and its own historical P/E of 47.8x.

Low P/Es require low EPS growth to sustain them. In the case of Dropbox, the company has recently shown a 711% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Dropbox’s Wall Street analyst-driven forecast is a 72% EPS growth and a 5% decline in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Dropbox’s $24 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 3% annually over the next three years. What Wall Street analysts expect for Dropbox’s earnings growth is above what the current stock market valuation requires in 2021, but below this requirement in 2022.

Furthermore, the company’s earning power in 2020 is 3x the long-run corporate average. Moreover, cash flows and cash on hand are 4x its total obligations, and intrinsic credit risk is 70bps above risk-free rate, signaling low credit risk.

Lastly, Dropbox’s Uniform earnings growth is above peer averages, while the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research