Dillard’s looks to be the model for the department store of the future, while rating agencies are stuck in the past

Retailers who invested heavily in online stores have seen this investment pay off in online customer growth and profitability improvement over the last two years. A great example of this is Dillard’s Inc. (DDS), an upscale department store chain with approximately 300 stores scattered across the southern half of the United States.

Unfortunately, credit rating agencies seem to once again be missing this significant shift that’s happening in the world of retail with Dillard’s success, as they still see the company at a high risk of bankruptcy.

However, we can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Everyone thinks that retail is dead, with none more so than the department store.

Lockdowns and restrictions due to the pandemic hampered the already struggling world of retail, as retailers and department stores took a big hit at the beginning of 2020.

By not specializing in anything, retailers are just bad enough at everything that people will just go online for whatever they need to.

And because of that, many retailers are viewed as risky investments by both equity and credit markets.

However, those that successfully prepared for such an occasion by investing heavily into e-commerce were quick to reap the rewards. By specializing in a lifestyle or product online, retailers were able to adapt to the post-pandemic world.

A great example of missing this transformation is BB- rated Dillard’s (DDS), for which rating agencies imply a 10% risk of bankruptcy for this upscale department store chain.

However, Dillard’s has actually done a lot better navigating this new world than one might think based on credit rating agencies, thanks to its move to e-commerce.

The company limited its inventory, created a strong online presence, and successfully managed its debt maturities and cost structure through rough times.

For these reasons, Dillard’s Credit Cash Flow Prime (CCFP) is way healthier than the market is thinking.

We can figure out if there is a real risk for this high-potential company by leveraging the CCFP to understand the company’s obligations matched against its cash and cash flows.

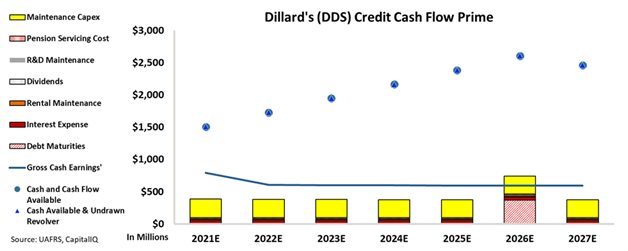

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

Its BB- rating suggests a high risk of default, but the CCFP shows that Dillard’s cash flows cover all of its obligations until 2026, when its large cash reserve will handily cover its 2026 debt.

That’s why the Valens Credit Rating is a much stronger IG3+, which is less than a 2% default risk.

Rating agencies seem to be missing the potential success of companies once again, by giving Dillard’s a credit rating that implies it is riskier than the company actually is.

On the contrary, Valens Credit Rating represents the full story of the company. Dillard’s has a lot less risk attached to it than what the rating agencies suggest.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Dillard’s, Inc. Tearsheet

As the Uniform Accounting tearsheet for Dillard’s, Inc. (DDS:USA) highlights, the Uniform P/E trades at 12.6x, which is below the global corporate average of 24.0x, but above its historical P/E of -4.3x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Dillard’s, the company has recently shown a 959% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Dillard’s Wall Street analyst-driven forecast is for a 40% and 41% EPS shrinkage in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Dillard’s $304 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to decline by 19% over the next three years. What Wall Street analysts expect for Dillard’s earnings growth is below what the current stock market valuation requires in 2023 and 2024.

Furthermore, the company’s earning power in 2022 is 4x the long-run corporate average. Moreover, cash flows and cash on hand are almost 4x its total obligations—including debt maturities and capex maintenance. All in all, this signals a low dividend risk.

Lastly, Dillard’s Uniform earnings growth is above its peer averages, but the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research