Mass customization seems like a logistical nightmare, but today’s PC maker shows how profitable the business model can be

While it may seem like a logistical nightmare, the concept of mass customization is one of the greatest manufacturing innovations of the last 30 years. With an efficient supply chain, companies can charge higher prices while also benefiting from economies of scale.

Today’s company is a trailblazer in the mass customization movement, but investors looking at as-reported metrics alone might fail to see the benefit to its stock.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Mass customization is one of the most revolutionary ideas in manufacturing over the last 30 years.

The concept allows large enough companies to offer its customers to build their products to specification while maintaining significant economies of scale.

Doing so successfully means some firms are able to charge more and spend less on their products, which is a recipe for massive profitability.

The best case study into mass customization comes from the inventor of the concept… Dell Technologies (DELL).

Starting in the 1990s, Dell began to offer PC users the ability to “build their own” devices, essentially allowing them to configure their computers to the exact specifications they desired.

Dell found immense success in this strategy.

Since it was able to sell massive volumes of PCs, accompanied by its ability to smartly source its suppliers, the company was able to achieve tremendous scale and thus generate robust profitability levels.

Dell quickly became one of the most popular PC makers worldwide thanks to the mass customization model.

Unfortunately, times change, as do business models. As Dell has grown, it has expanded into different business lines like enterprise production, and competitors have begun catching up to its manufacturing efficiency, making it more difficult to earn a strong return.

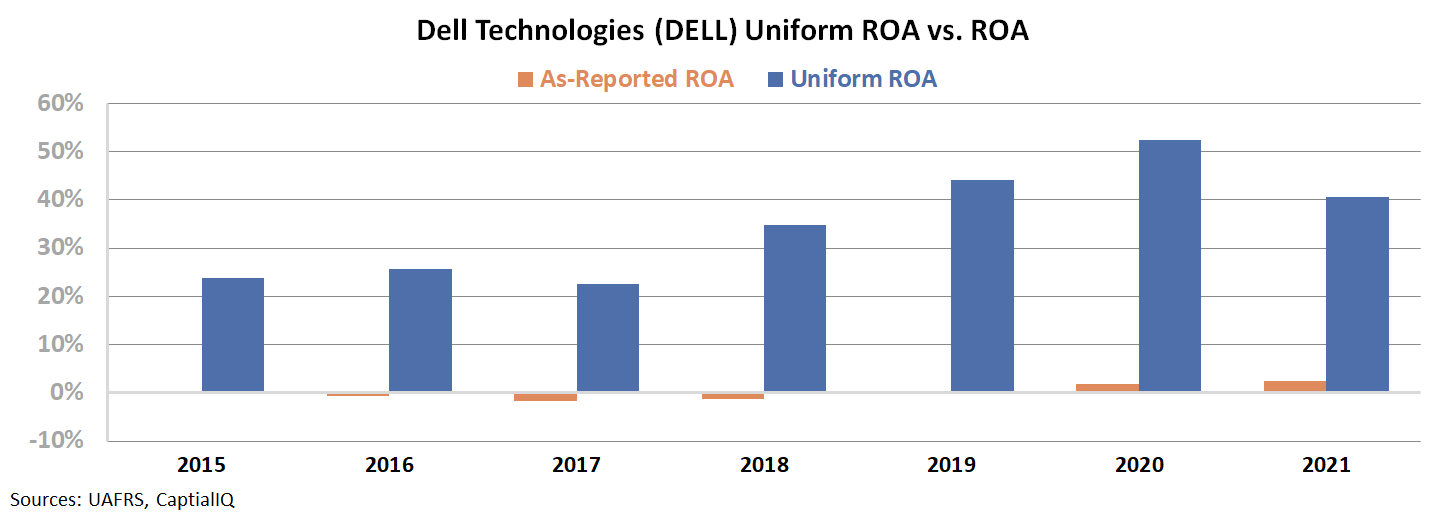

Investors analyzing Dell’s performance over the past seven or so years would fail to see the value mass customization has brought to its profitability metrics.

Specifically, since 2015, the firm’s as-reported ROA levels have been muted, well below the U.S. corporate average of about 12%, let alone above its own cost of capital.

See for yourself below.

These profitability levels make it look like Dell’s mass customization model may be hurting returns, not supporting them.

However, the problem lies with the as-reported metrics, which distort Dell’s real profitability. When looking at Uniform metrics, the firm has generated robust and improving returns since 2015.

Specifically, Dell has been able to expand its ROA from 24% levels in 2015 to even more robust levels of 41% in 2021.

Even as Dell has seen its core business shift away from solely PCs to an enterprise focused company, Uniform metrics highlight how the mass customization model continues adding value today.

SUMMARY and Dell Technologies Inc. Tearsheet

As the Uniform Accounting tearsheet for Dell Technologies Inc. (DELL:USA) highlights, its Uniform P/E trades at 11.1x, which is below the global corporate average of 25.2x, but around its own historical average of 9.5x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Dell Technologies, the company has recently shown a 14% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Dell Technologies’ Wall Street analyst-driven forecast is an immaterial EPS growth in 2022, followed by a 3% EPS decline in 2023.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Dell Technologies’ $89 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 10% annually over the next three years. What Wall Street analysts expect for Dell Technologies’ earnings growth is above what the current stock market valuation requires through 2023.

Furthermore, the company’s earning power is 7x the long-run corporate average. Also, cash flows and cash on hand are above its total obligations—including debt maturities and capex maintenance. Together, this signals a low credit risk.

To conclude, Dell Technologies’ Uniform earnings growth is well above peer averages, but the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research