Did A Hedge Fund Legend Play In The 1932 World Series?

It’s game 3 of the 1932 World Series, and the score is tied 4-4 in the 5th inning.

October baseball is always special, but an at bat in a tied game in the World Series is a true pressure cooker.

Babe Ruth strode to the plate for the Yankees, facing the Chicago Cubs in Wrigley Field.

As he takes strike one, the Cubs bench players are jeering at him, and the Wrigleyville faithful are screaming any insult they can think of.

Ruth doesn’t tune them out, instead he steps one foot out of the batter’s box and points the head of his bat to the deepest part of center field. He steps back into the box.

He takes strike two.

The fans, the players, the atmosphere only gets louder. They smell blood.

Ruth steps out again. And he does again uses his bat again to point to the Exact. Same. Place. He’s calling his shot!

He steps back in to the batter’s box… and Charlie Root throws a curveball that never makes it to the catcher’s mitt.

Instead it ends up over 440 feet away into the center field stands. Exactly where he said he would.

The Yankees went on to win the game 7-5, and to win the series also. And baseball fans have loved telling that story every day since.

That story has such staying power because of the improbability of it. It’s easy for a pitcher, to say after a no-hitter, that he felt like something special was going to happen as he warmed up that afternoon. It’s easy to look back and call David Ortiz one of the most clutch players of all time after he helped the Red Sox win 3 world series. But to be able to call your shot, not just that you were going to get a hit, but that you were going to hit a home run, over right center field, is near impossible.

Which is why it’s so impressive that sixty years later, Seth Klarman did the exact same thing. And its why he’s a legend in his field, almost to the scale Babe Ruth is in baseball.

Seth Klarman didn’t play in the World Series for the Yankees or hit a home run in Wrigley. He’s actually a minority owner of the Red Sox, so the idea of him playing for the Yankees is rather ironic.

But Seth Klarman has been a wildly successful investor. His fund Baupost has produced 20% returns a year since 1983. He’s outperformed the market by almost 4x since he started the strategy.

But what’s impressive isn’t just that he has had such phenomenal returns. It’s that he told everyone how he was going to get those returns before he did.

Long before Klarman became a billionaire he wrote a book called Margin of Safety. The name is an homage to Ben Graham’s Security Analysis.

In the book, Klarman laid out his value investing philosophy and how he would pick stocks. He laid out his exact strategy that would eventually lead to Baupost’s phenomenal performance. He called his shot, and then he delivered 4x the market’s performance.

Klarman and Baupost are still picking stocks today, and is doing an amazing job.

Part of the reason they remain so successful is because Klarman has as much skepticism about as-reported accounting metrics as we do here at Valens.

Klarman has regularly railed against the issues with as-reported accounting metrics. He has mocked investors who use metrics like EBIT and EBITDA to value companies, because of how distorted they are.

At Baupost, they are focused on the real operating profitability of companies, not the inaccurate noise of as-reported accounting metrics.

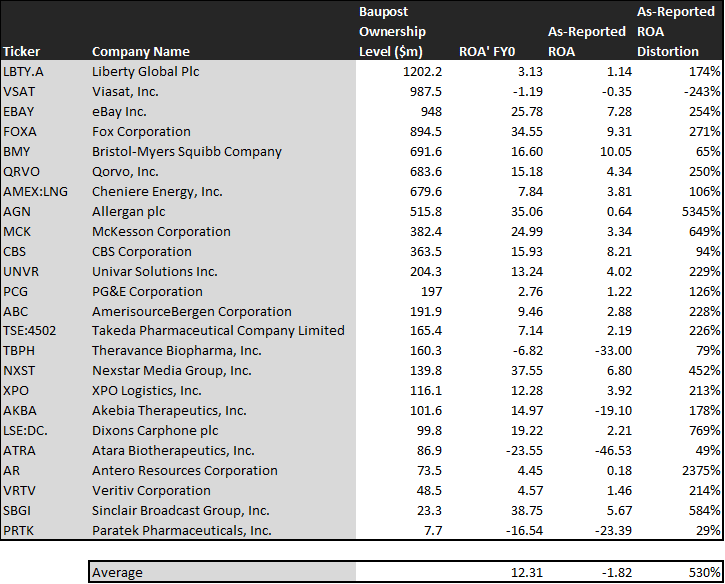

Because of Baupost’s strong research, their analysis unsurprisingly lines up with Valens Uniform Accounting. To show what we mean, we’ve done a high level portfolio audit of Baupost’s current portfolio, based on their most recent 13-F. This is a very light version of the custom portfolio audit we do for our institutional clients when we analyze their portfolios for torpedos and companies they may want to “lean in” on.

Using as-reported accounting, investors would be scratching their heads at the companies that Baupost is buying. The average company in their portfolio has a negative return on assets (ROA). On an as-reported basis, it is losing money. If we look at the median, the median company in their portfolio only is producing a miserly 2.5% ROA. That’s well below cost-of-capital levels, according to any model.

But once we make Uniform Accounting (UAFRS) adjustments, we realize that the returns of the companies in Klarman’s portfolio are much more robust. Once the distortions from as-reported accounting are removed, we realize that Allergan (AGN) doesn’t have a 0.6% ROA, its actually at 35%. For some companies, as-reported metrics are even directionally wrong. Akebia Therapeutics (AKBA) doesn’t have a -19% ROA, like as-reported metrics show, they have a 15% UAFRS ROA. Sinclair Broadcast Group’s (SBGI) ROA is really 39%, not 6%.

If Baupost was looking at as-reported metrics, they would never pick most of these companies, because they look like bad companies, and poor investments. For the average company, as-reported ROA understates profitability by almost 80%. Uniform ROA is 500% higher than the distorted as-reported metrics.

But Baupost isn’t just finding companies where as-reported metrics mis-represent a company’s real profitability. The reason Baupost has such phenomenal returns is because they’re also identifying companies where the market is significantly undervaluing the company’s potential. This is where Klarman’s “Margin of Safety” comes into play. They are buying companies that the market has low expectations for, that they think the companies can exceed.

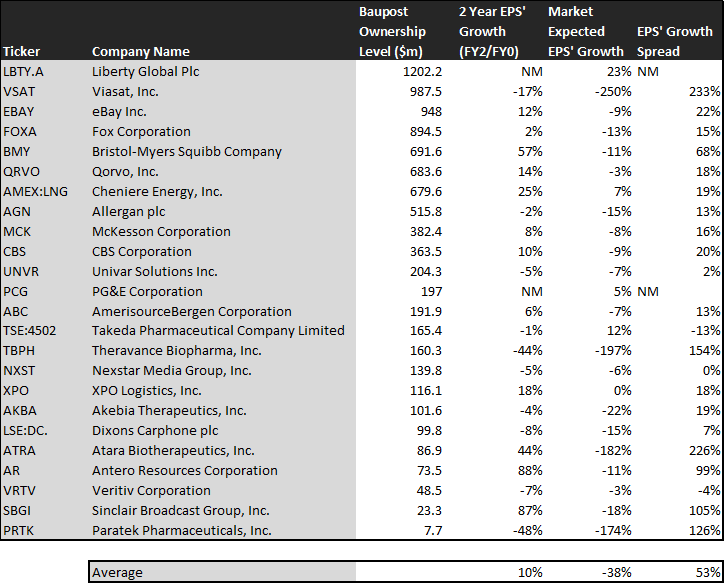

This chart shows three interesting datapoints:

- The first datapoint is what earnings growth is forecast to be over the next two years, when we take consensus Wall Street estimates, and we convert them to the Uniform Accounting framework. This represents the earnings growth the company is likely to have in the next two years

- The second datapoint is what the market thinks earnings growth is going to be for the next two years. Here, we are showing how much the company needs to grow earnings by in the next 2 years to justify the current stock price of the company. If you’ve been reading our daily and our reports for a while, you’ll be familiar with the term embedded expectations. This is the market’s embedded expectations for earnings growth

- The final datapoint is the spread between what the company could do, if the Uniform Accounting adjusted Wall Street estimates are right, and what the market expects earnings growth to be

If the spread is highly positive, that means a company is undervalued, and the stock is likely to rise if the company delivers on what earnings are forecast to be. If the spread is highly negative, that means the company is overvalued and will fall if the company hits on estimated earnings growth rates.

For context, the average US listed company (above $1 billion market cap) has an EPS growth spread of 5%. For the average company, the market is undervaluing their earnings growth by 5%, which is basically fairly valued. For most companies, the market gets it right, and correctly prices the company’s potential.

But Baupost is finding companies the market is MASSIVELY undervaluing. The market is mispricing the average Baupost company’s earnings growth by 50%+. For some companies, like Sinclair, the market is undervaluing the company’s earnings growth by over 100%. The market is expecting Sinclair to have shrinking earnings the next 2 years, when they’re actually forecast to almost double.

Baupost is even finding megacap names with significant mispricings. Bristol-Myers Squibb (BMY) is priced for earnings to decline by 11% a year the next 2 years. It’s actually forecast to grow 57%.

There are some names that we’d recommend Baupost review in their portfolio if we were meeting with their PMs. Two that jump out are Takeda (TSE:4502) and Nexstar (NXST). For Takeda, the market is pricing in 12% annual earnings growth right now, but the company is actually forecast for Uniform Accounting EPS to shrink by 1% a year the next two years. For Nexstar, the market appears to be getting the company right. The company is forecast to see Uniform Accounting earnings shrink by 5% a year going forward, and the market is pricing it for 6% a year declines.

But for the most part, Baupost gets it right. And they get it right because they’re not trusting the as-reported accounting statements, and they’re following the maxims that Klarman wrote long before he became as successful as he is today.

We’re Relaunching Our Portfolio Audit Review Offering – And Making A Special Offer

For our institutional clients, we don’t just provide access to our Valens Research app. We also do bespoke research. We produce one-off deep-dive company analyses using all our tools, including Uniform Accounting, credit work, and our management compensation and earnings call analysis. We monitor their portfolios for potential Uniform Accounting signals to alert them. We provide custom datasets for quantitative analysis, and provide aggregate analytics. We also help them create unique idea generation screens that are customized to their approach, using Uniform Accounting and our other analytics.

But for most of our institutional clients, the analysis that they find most useful, and almost universally ask for, is a quarterly portfolio audit and call with our analysts.

Our institutional clients pay a significant premium for all our bespoke research. Some of our institutional clients have paid well over $100,000 a year for our uniquely tailored Uniform Accounting research because of the value it adds to their process.

Until Thanksgiving, we’re making a special offer.

For any investor that buys access to the Valens Research app ($10,000/year or $1,000/month subscription), we will include an Institutional-level portfolio audit and call with our analyst team with no extra charge.

Also, for those people who sign up to the offer before November 1st, we’ll include a lifetime access to all of our newsletters, including our Market Phase Cycle™ and Conviction Long Idea List (a $6,000 value), for no extra charge, as long as you remain a Valens Research app subscriber.

We want to help show you how powerful Uniform Accounting research can be for your investment strategy.

If you want to hear more about this offer, or are interested in subscribing, feel free to reply to this email. I’ll forward on your note to our head of client servicing. Or, feel free to reach out to Doug Haddad, the head of our client relations team, at doug.haddad@valens-securities.com or at 630-841-0683.

Today’s Tearsheet

Today’s tearsheet is for Home Depot. Home Depot trades at a slight premium to the market. However, at current valuations, the market expectations for Uniform EPS growth are significantly less than growth was last year, and roughly in line with forecasts for the next 2 years. The company’s forecast earnings growth lags peers, but the company has robust profitability and no risk to its dividend yield.

Regards,

Joel Litman

Chief Investment Strategist