This Company is Revolutionizing How You Will Consume Sports

Fox (FOX) and Warner Bros. Discovery (WBD) are teaming up with Disney (DIS) to introduce a new sports streaming service jointly owned by the three companies.

This partnership, while facing concerns about limited competition, marks a significant move from traditional cable to digital streaming.

Despite previous hurdles in similar projects, the recent uptick in Disney’s stock indicates a growing confidence in their strategy.

Today, we will delve into what this platform means for Disney’s future in sports, and if the market is on board.

Also below is a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

As the landscape of television consumption shifts dramatically, the move from cable to streaming platforms represents what could be the final chapter for traditional cable TV, especially in the realm of sports broadcasting.

In response to this seismic shift, industry giants Disney, Fox, and Warner Bros. Discovery are joining forces to launch a groundbreaking sports streaming service.

This collaborative effort not only heralds a new era in how sports content is delivered but also presents a direct challenge to the cable industry’s hold on live sports.

The platform will merge the sports content from each company. Each partner will license their channels to the service and retain their respective advertising revenue.

The move to streaming has been anticipated, as sports broadcasts have kept cable television relevant. This joint venture could accelerate the decline of traditional cable, marking a significant shift in how viewers consume sports.

However, Disney’s previous attempt to create a streaming superteam was unsuccessful. Hulu was originally co-owned by Fox, NBC, and Disney, but the failed venture led to Disney acquiring Hulu outright. Hulu’s story leaves question marks about the potential success of this new venture.

A significant challenge for this new service is the absence of key sports content. Without NBC’s Comcast and CBS’s Paramount, popular events like Sunday and Thursday NFL games will not be available, potentially alienating a large portion of the audience.

Moreover, the partnership has not secured direct involvement from major sports leagues. These leagues can license their content elsewhere, further limiting the platform’s offerings.

The rise of technology companies like Amazon (AMZN) and Apple (AAPL) as major content distributors adds to the competition.

Currently, Warner’s TNT and Disney’s ESPN are negotiating to renew their NBA broadcasting rights. Failure to secure a deal could lead the NBA to explore other options.

Despite these challenges, Disney is not relying solely on the joint venture, as it plans to launch its ESPN streaming service independently in the fall of 2025.

This dual strategy might position Disney favorably, regardless of the new platform’s performance, leading to speculation about the future impact on the sports streaming landscape.

Over the past year, Disney’s stock suffered due to a decrease in Disney+ subscriptions and growing doubts about the company’s proficiency in the streaming industry, particularly the future of ESPN.

However, the situation appears to be turning around. Since the announcement of the new streaming service, Disney’s stock (DIS) has seen a 12% increase, indicating a positive market response and potentially marking the beginning of a recovery for the company in the competitive streaming landscape.

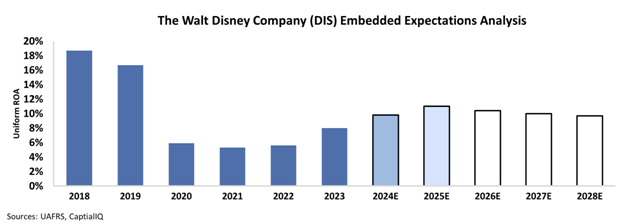

We can further see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to rebound to 9.8%. While this is far from the highs of 2018, it shows significant improvement over the last several years.

The market’s optimism suggests that it believes that Disney may have finally turned a corner when it comes to streaming.

Overall, while competition continues to intensify, Disney has taken active steps to secure a foothold in the sports streaming industry, leveraging its strong content portfolio and brand legacy.

SUMMARY and The Walt Disney Company Tearsheet

As the Uniform Accounting tearsheet for The Walt Disney Company (DIS:USA) highlights, the Uniform P/E trades at 24.7x, which is around its global corporate average of 22.9x but below its historical P/E of 34.4x.

Average P/Es require average EPS growth to sustain them. In the case of Walt Disney, the company has recently shown a 43% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Walt Disney’s Wall Street analyst-driven forecast is a 15% and 20% EPS growth in 2024 and 2025, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Walt Disney’s $108 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to have immaterial growth annually over the next three years. What Wall Street analysts expect for Walt Disney’s earnings growth is above what the current stock market valuation requires through 2025.

Furthermore, the company’s earning power is above its long-run corporate average. Moreover, cash flows and cash on hand are 2x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 30bps above the risk-free rate.

All in all, this signals low credit and dividend risk.

Lastly, Walt Disney’s Uniform earnings growth is in line with its peer averages, and also in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research