Budget wireless service provider DISH may not be as much of a bargain for investors

With 5G communications shaping up to be the next avenue of growth for wireless providers, it is no surprise to industry giants snapping up the wireless spectrum.

Yet, a much smaller player has quietly become one of the biggest bidders for 5G bandwidth, competing with the likes of AT&T, Verizon, and T-Mobile with its plans for low cost phone and wireless bundles.

While as-reported metrics show this company trading at a favorable discount to the market, a quick look at Uniform Accounting may make investors think twice before rushing in.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Over the past decade, the steady consolidation of the telecommunications industry, particularly in the U.S., has many regulators worried about a lack of competitive markets and higher consumer prices.

These longstanding concerns have been ramped up recently following the 2020 merger of Sprint with T-Mobile (TMUS), which has effectively left the U.S. with only three real major telecom players: AT&T (T), Verizon (VZ), and the new T-Mobile and Sprint combination.

With smaller companies such as U.S. Cellular now practically irrelevant, many have placed their hopes for a competitor further afield, specifically one like DISH Network (DISH).

DISH has traditionally been a provider of paid television services, offering its 11 million customers programming on national, regional, and local broadcast and cable networks, as well as sports and premium movie channels.

As the potential of 5G communications technology has emerged over the past few years, one of the biggest surprises has been DISH’s foray as a bidder for spectrum space against the telecom giants.

The company has recently discussed a plan to compete with the big three providers by combining its existing low-cost bundle satellite offering with a low-cost phone bundle.

Ironically, DISH helped the Sprint and T-Mobile acquisition go through. The Department of Justice required Sprint to sell its prepaid wireless business to approve the merger, so DISH entered as a buyer for the business, which includes the Boost Mobile and Virgin Mobile brands.

DISH’s plans to reshape the wireless business and introduce more competition to one of the country’s most consolidated industries have many curious if they can actually pull it off.

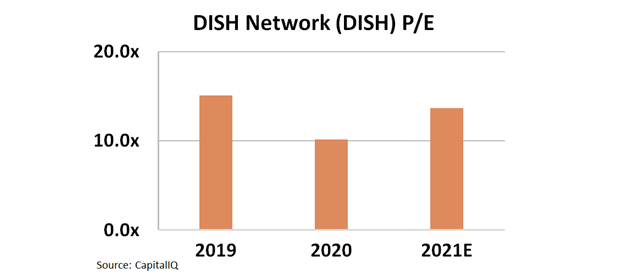

The most interesting piece to this story is, based on DISH’s as-reported forward price-to-earnings ratio (“P/E”), it appears investors don’t have to overpay to bet the company will at least have some success with its strategy.

The as-reported P/E figure, which was as high as 22.4x in 2017, is now sitting at a low of 13.8x, comfortably below market averages. If the company sees any sort of uptake of its wireless business, so the thinking goes, the market will wake up to the cheap discount and the stock could rocket higher.

While this may sound like an interesting investment opportunity at first glance, it’s actually an important case study for how GAAP accounting and as-reported metrics fail investors.

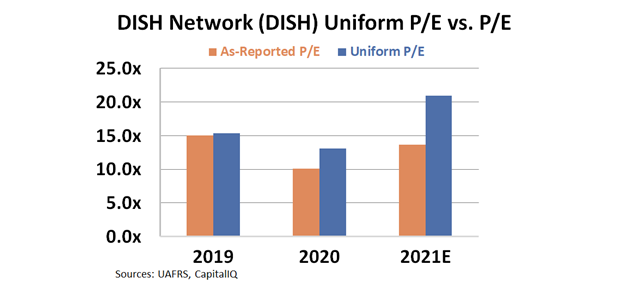

This is because the reality for DISH isn’t as rosy as it seems. By utilizing Uniform Accounting to remove distortions and get to the true operating picture of the company, we can see that DISH’s Uniform P/E is actually trading at 20.9x levels, not the 13.8x as-reported metrics suggest.

This means anyone buying the stock at these levels is paying average valuations for a company now staring down some significant capex spending in the coming years, making the stock look much less compelling.

The casual observer might be led to believe DISH offers a compelling discount at current prices, yet in reality, Uniform Accounting shows investors might be getting less than they bargained for.

SUMMARY and DISH Network Corporation Tearsheet

As the Uniform Accounting tearsheet for DISH Network Corporation (DISH:USA) highlights, the Uniform P/E trades at 20.7x, which is below the global corporate average of 24.3x, but above its historical P/E of 18.9x.

Low P/Es require low EPS growth to sustain them. In the case of DISH, the company has recently shown a 98% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, DISH’s Wall Street analyst-driven forecast is a 2% EPS growth in 2021 and a 30% shrinkage in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify DISH’s $45 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 3% annually over the next three years. What Wall Street analysts expect for DISH’s earnings growth is above what the current stock market valuation requires in 2021, but is below that requirement in 2022.

Furthermore, the company’s earning power in 2020 is equal to the long-run corporate average. Moreover, cash flows and cash on hand are almost twice its total obligations—including debt maturities and capex maintenance. All in all, this signals a low credit risk.

Lastly, DISH’s Uniform earnings growth is below peer averages, while the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research