Disney isn’t the only company with strong IP… Today’s firm stands toe-to-toe against the largest conglomerates in the content world

Today’s firm has been able to hold up against some of the biggest content creators thanks to its strong brand.

Despite its robust operations and strategies, many investors see this firm as an average content creator. However, this is only because they are looking at the incorrect data.

As-reported metrics highlight that today’s firm has seen profitability hover around the corporate average since 2013, but Uniform Accounting tells a different story.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

With Disney’s (DIS) Star Wars and Marvel Cinematic Universe, it may feel as though “The Mouse” dominates the world of content.

However, there are still companies other than Disney that capture the attention of large swaths of the marketplace. These are companies who build a unified content strategy with everything from movies to TV shows, alongside games and toys.

Hasbro’s (HAS) portfolio of content has been beloved for decades, even if a game of Monopoly can sometimes feel more like torture than entertainment. The company is known for its range of product lines such as G.I. Joe and Transformers, Magic the Gathering to Nerf, and even Play Doh.

The company even holds partnerships with content juggernauts such as Disney to make toys in the Star Wars universe.

Considering the dominance of Hasbro’s brands across various end markets and its success in monetizing some of these markets in new ways, investors might expect it to have impressive profitability levels.

Creating innovative ways to monetize end markets is difficult. Hasbro has been trying to grow profitability through initiatives like the Transformer movies or the acquisition of the film studio eOne to push more of its brands into the digital age.

Hasbro has been able to position itself in front of the younger generation. The franchise My LIttle Pony, first launched in 1981, has seen a new renaissance in toys, shows, and movies with a widely successful reboot in 2010.

To the casual investor, it would appear that Hasbro has struggled in the face of other large entertainment conglomerates.

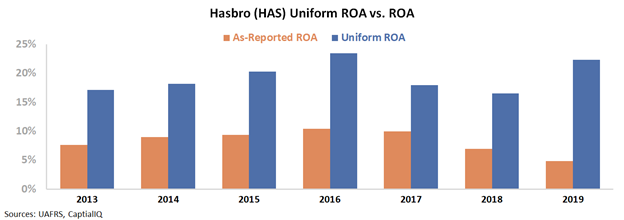

Hasbro’s as-reported ROA expanded from 8% in 2013 to a peak of 11% in 2016. Despite this rise, as-reported ROA has steadily declined to a grim 5% in 2019. Looking at these metrics, Hasbro can just be seen as a steadily failing business struggling to stay relevant in the digital world.

While many investors explain these returns away as other major content machines consuming all the attention in the space, the reality is most investors are missing out on Hasbro’s true profitability.

Once we make the necessary Uniform Accounting adjustments to line items such as goodwill, operating leases, and other distortions, we can see Hasbro has in fact generated returns well above corporate average levels.

In reality, Hasbro has been able to hold its position in the face of other monoliths thanks to the strength of its brands.

Over the past seven years, Uniform ROA has risen from 17% to 22%. Despite having a minor lull from 2016 to 2019, Hasbro was able to bounce back on the back of its cross-integration strategy.

See for yourself below.

When analyzing the company with Uniform Accounting, investors can see the success of Hasbro’s ventures over the past decade. Investors stuck using as-reported metrics for their analysis will only ever be grasping at straws when trying to determine the success or failure of a business.

SUMMARY and Hasbro, Inc. Tearsheet

As the Uniform Accounting tearsheet for Hasbro, Inc. (HAS:USA) highlights, the Uniform P/E trades at 18.0x, which is below the global corporate average of 25.2x and its historical average of 22.9x.

Low P/Es require Low EPS growth to sustain them. In the case of Hasbro, the company has recently shown a 49% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Hasbro’s Wall Street analyst-driven forecast is a 51% EPS shrinkage in 2020, followed by a 104% EPS growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Hasbro’s $94 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 4% per year over the next three years and still justify current stock prices. What Wall Street analysts expect for Hasbro’s earnings growth is below what the current stock market valuation requires in 2020, but above this requirement in 2021.

Furthermore, the company’s earning power is 4x the corporate average. Also, cash flows and cash on hand are almost 2x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Hasbro’s Uniform earnings growth is below its peer averages, but the company is trading in line with peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research