This $8.5 billion acquisition was deemed a failure, Uniform Accounting shows the value hidden within this discount retailer

Acquisitions have the ability to transform a company. Sometimes they can improve a company’s performance. In other cases, they do the opposite. Today’s firm made a sizable acquisition in 2015, and the market has punished it since.

As-reported metrics would have you believe this company’s returns have stagnated due to the acquisition, but true UAFRS (Uniform) based analysis shows the firm’s real profitability.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

“Survive and Thrive” has become a top theme since the coronavirus pandemic began and one that’s often discussed here at Valens.

Companies that are in a position to acquire other businesses fit the theme well. This is because strategic acquirers have the opportunity to buy distressed companies at cheap prices. In turn, this allows the acquirer to consolidate market share and create synergies.

However, not all acquisitions are created equal. There are two common mistakes companies make that have the potential to destroy value.

The first is entering a bidding war.

When a bidding war commences, the winner oftentimes struggles from the “winner’s curse,” meaning the winning bid is higher than the value of the asset. Usually, this occurs during the second half of a bull market.

The second common mistake is buying a company that is too large.

Smaller companies are easier to integrate. Synergies can take a long time to surface when acquiring a large company.

In 2014, the Dollar Tree (DLTR) made both of these mistakes. At the time, business was booming for the company. People were still struggling after the Great Recession and needed somewhere to buy cheap everyday goods.

Due to competitive pressures, Dollar Tree was forced to grow through consolidation. As such, Dollar Tree went after Family Dollar.

It wasn’t the only company with this idea—Dollar General (DG) joined the bidding war too.

In the end, Dollar Tree prevailed; but in doing so, management made both acquisition mistakes we mentioned earlier. One, Dollar Tree entered a bidding war with Dollar General, and two, Family Dollar was over half the size of Dollar Tree at the time. Because of this, it makes sense that Dollar Tree had trouble integrating Family Dollar’s operations.

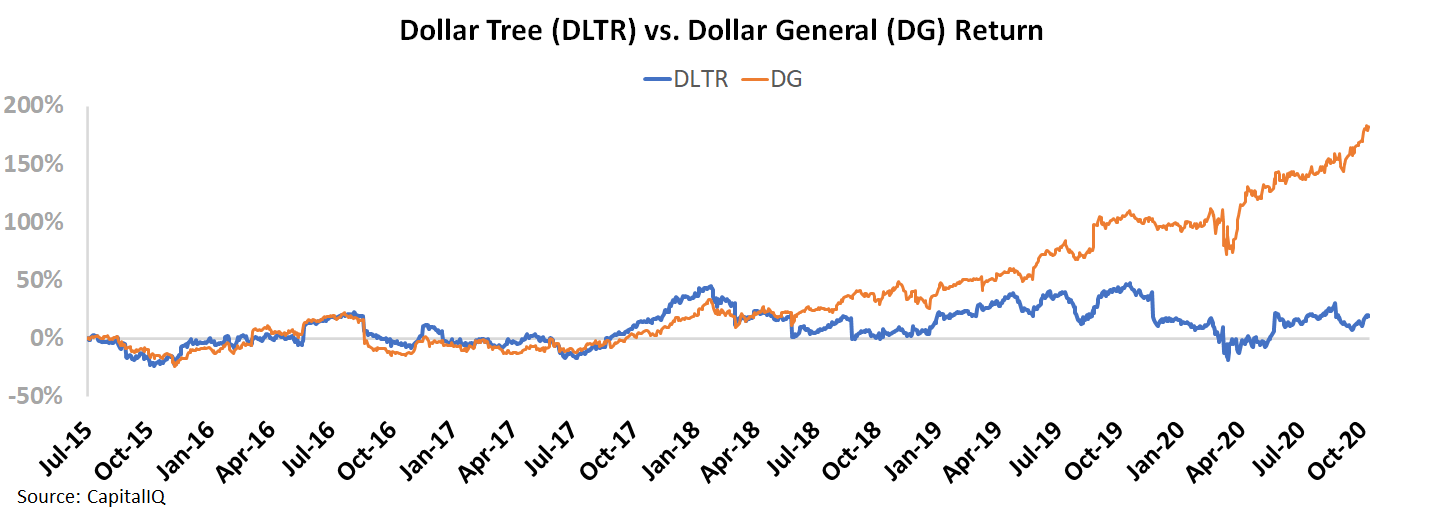

Dollar Tree has underperformed Dollar General since the bidding war. Since July 2015, Dollar General’s stock has appreciated roughly 180% while Dollar Tree’s stock is only up 20% in the same time period.

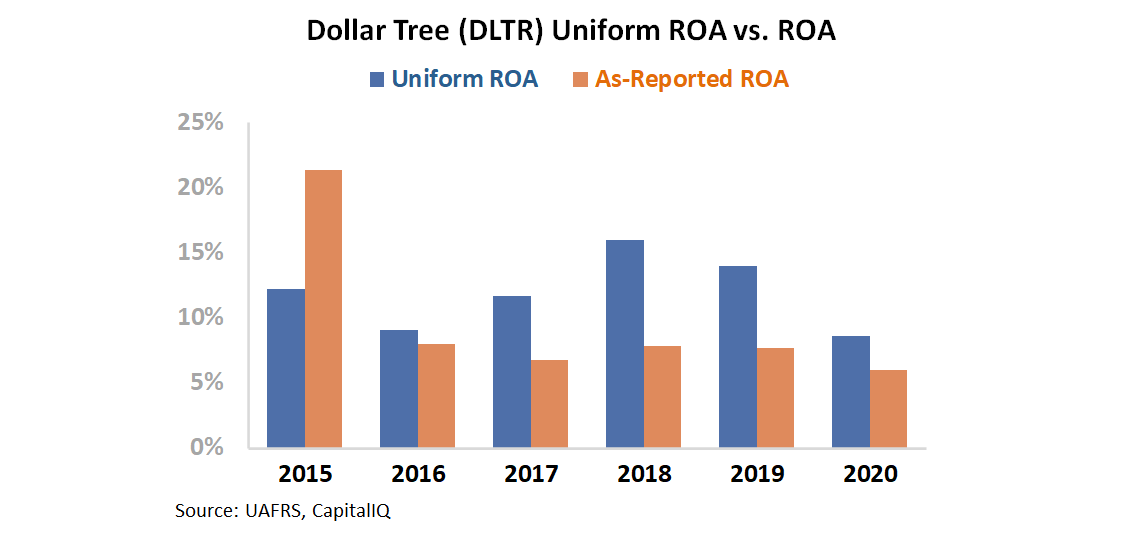

As-reported accounting confirms Dollar Tree’s struggles. As-reported return on assets (ROA) fell from 21% in 2015 to 8% the following year. Since then, ROA has remained between 6% and 8%, well below corporate averages.

These metrics seem to indicate that Dollar Tree failed to integrate Family Dollar and create synergies.

However, this is not an accurate representation of the firm’s profitability. GAAP’s treatment of special items, among other distortions, is suppressing the firm’s profitability metrics.

After adjusting for these adjustments, Uniform ROA shows Dollar Tree’s profitability has actually improved in recent years.

While returns fell the year after the acquisition, Dollar Tree has since been able to integrate Family Dollar into its business. By 2018, Uniform ROA reached 16%—a 13-year high.

In the last two years, returns have begun contracting. While investors might see that as a negative sign, it’s actually because Dollar Tree is growing its store count. New stores tend to be capital intensive with a multi-year payback period.

Dollar Tree’s renewed focus on store growth means that it has managed to integrate Family Dollar’s operations. Investors who recognize this should be excited, not scared about the company’s recent returns.

While investors focused on as-reported metrics might think recent struggles are from a failed acquisition, Uniform metrics reveal they are from shorter-term issues. Dollar Tree has worked through similar growing pains in the past.

With the stock roughly flat since 2015, investors who see the real story should be excited for a potential buying opportunity.

SUMMARY and Dollar Tree, Inc. Tearsheet

As the Uniform Accounting tearsheet for Dollar Tree, Inc. (DLTR:USA) highlights, its Uniform P/E trades at 19.5x, which is below global corporate average valuation levels, but around its historical average valuations.

Average P/Es require average EPS growth to sustain them. In the case of Dollar Tree, the company has recently shown a 31% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Dollar Tree’s Wall Street analyst-driven forecast is a 35% EPS growth in 2021 and a 6% EPS contraction in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Dollar Tree’s $95 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 4% over the next three years. What Wall Street analysts expect for Dollar Tree’s earnings growth is above what the current stock market valuation requires in 2021, but below its requirement in 2022.

Furthermore, the company’s earning power is higher than the corporate average. Also, cash flows and cash on hand are 2x its total obligations—including debt maturities and capex maintenance. Together, this signals low credit risk.

To conclude, Dollar Tree’s Uniform earnings growth is in line with its peer averages, but the company is trading below peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research