The pandemic gave this e-signature company a chance for recovery

When offices shut down and everyone started working from home, there was no easy way to sign contracts, purchase orders, and other important legal documents.

For DocuSign, this was the perfect scenario, as the company provides a way to securely sign legal documents and contracts digitally.

Today, we are going to break down DocuSign and see how its true performance under Uniform Accounting is much different than investors realize.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

As the pandemic overtook the world, companies transitioned to remote working. This was followed by a surge in the housing market as people moved out of cities and into the suburbs—no longer needing to be near their jobs.

Employees scattered and companies realized they could be better off cutting out utility expenses by closing offices. One of the big issues people worried about initially was how to get all the contracts, legal documents, and purchase orders signed.

People realized society still needed a way to prove contracts were actually signed by the person in question without face-to-face contact.

In a world where notaries weren’t an option if you had to socially distance, or where in person signings were impractical if someone had relocated, a better solution was necessary.

That’s where DocuSign (DOCU) came in.

DocuSign provides online solutions for signing documents and contracts in the cloud. DocuSign allowed for home purchases or rentals without meeting in person during the pandemic, both saving lives and allowing purchasers to buy sight unseen.

It’s used in a wide range of industries beyond just real estate, including financial services, governmental, education, and health care, and its certificate-based signature integration assures legal documents and contracts to be executed and completed within a couple of clicks.

One would expect that the pandemic would be a banner period for a company like DocuSign as everyone moved online, especially after things really started accelerating for it in 2021 once the initial volatility of the pandemic was put behind it.

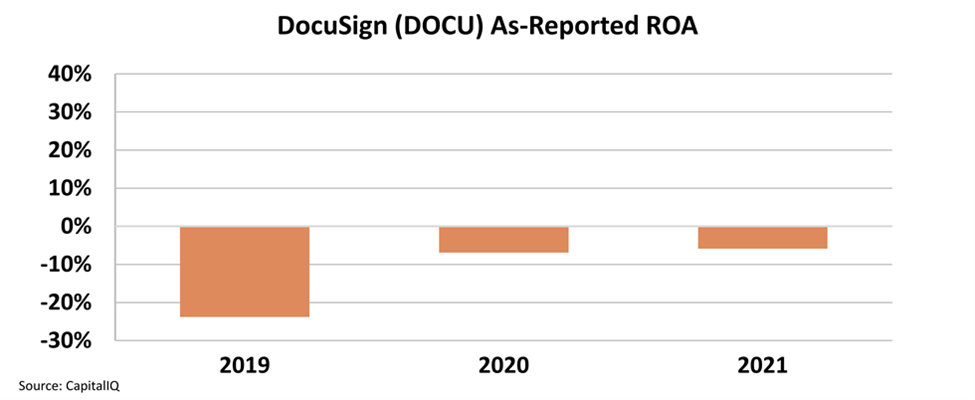

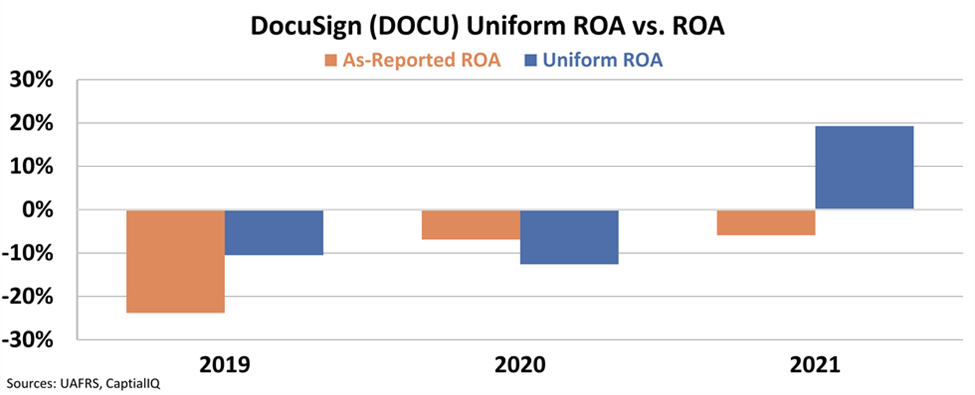

Yet looking at as-reported metrics, DocuSign saw negative profitability in 2020 and 2021, sitting at -7% and -5% ROA, respectively.

This poor profitability makes it appear that even in the best of times for DocuSign, it couldn’t generate a profit.

However, Uniform metrics tell a different story.

Uniform Accounting shows us that while DocuSign actually performed worse in 2020 than as-reported metrics make it appear, with a -13% ROA, it inflected positively in 2021, reaching a 19% ROA.

As-reported metrics distort how much the pandemic helped DocuSign. Furthermore, as people move out to the suburbs and more people continue to work from home, it doesn’t seem the need for the ability to sign documents online will go away any time soon.

Uniform metrics show us that as DocuSign finally hit critical mass, it saw fundamentals accelerate, and along with that came great improvement in profitability. This flip to positive profitability with scale was completely missed by as-reported metrics, which may mean many investors would write off the stock before doing any valuation work.

SUMMARY and DocuSign, Inc. Tearsheet

As the Uniform Accounting tearsheet for DocuSign, Inc. (DOCU:USA) highlights, the Uniform P/E trades at 38.6x, which is above the global corporate average of 24.0x but below its own historical P/E of 43.2x.

High P/Es require high EPS growth to sustain them. In the case of DocuSign, the company has recently shown a 200% Uniform EPS growth from 2020.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, DocuSign’s Wall Street analyst-driven forecast is a 109% and 4% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify DocuSign’ $75 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 26% annually over the next three years. What Wall Street analysts expect for DocuSign’ earnings growth is above what the current stock market valuation requires in 2022 but below that requirement in 2023.

Furthermore, the company’s earning power in 2021 is 3x the long-run corporate average. Moreover, cash flows and cash on hand are almost twice its total obligations—including debt maturities and capex maintenance. Additionally, intrinsic credit risk is 60bps above the risk-free rate. All in all, this signals low credit risk.

Lastly, DocuSign’s Uniform earnings growth is above its peer averages and the company is also trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research