I’m at the CFA Institute Equity Research & Valuation Conference Today

Hello from New York City. I’ll be presenting at the CFA Institute Equity Research & Valuation Conference today.

My presentation is titled “NOT EVEN Apples to Oranges”, and I’ll be talking about how problematic GAAP and non-GAAP metrics are for investors.

Of course, our goal with Uniform Accounting is to remove the problems that make modern accounting bordering on useless for investors.

Great investors from Buffett, to Munger, Klarman, Whitman, and many others regularly use terms like “inconsistent,” “misleading,” and “distorted” to describe the accounting statements.

By making the 130 adjustments we make under Uniform Accounting, we remove the distortions inherent in arcane accounting mathematics, and enable investors to make educated investment decisions across equity, credit, and macro decision making.

There are also a couple of great speakers I’m excited to see at the event, from Nouriel Roubini later today for macro insights, to Aswath Damodaran tomorrow discussing how to analyze and value innovative disruptive companies.

If you’re going to be at the conference, be sure to stop by and say hello.

Join us for The Uniform Accounting Webinar this Friday

This Friday, we’ll be hosting a webinar highlighting the massive distortions that are inherent in as-reported accounting.

We’ll be drilling down on why as-reported accounting gets these 5 companies wrong:

Microsoft (MSFT)

Roku (ROKU)

Booking Holdings (BKNG)

Comcast (CMCS.A)

Discovery (DISCA)

And how, using Uniform Accounting, we can get better insights, understand what the market’s pricing in, and what the company could really be worth.

For example, we’ll be discussing why Roku’s EPS is really $1.00, not -$0.08,

We’ll also discuss how Comcast is more expensive than investors think, as its P/E is really 22x, not 14x.

To register for the webinar, click here.

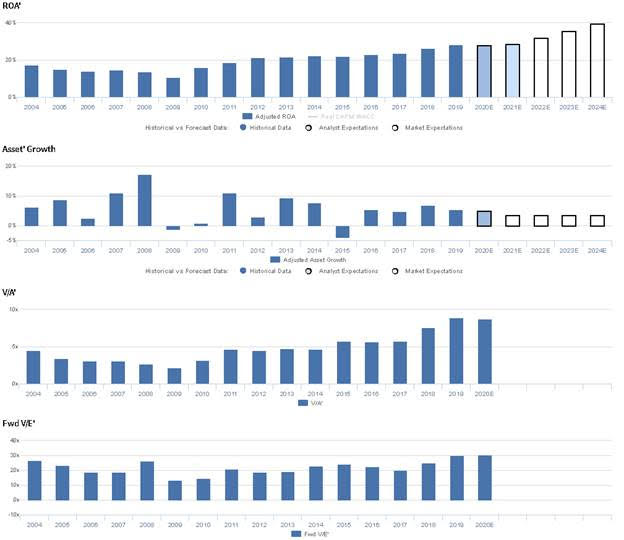

Market expectations are for Uniform ROA expansion, but management may be concerned about growth, China, and travel retail

EL currently trades near historical highs relative to UAFRS-based (Uniform) Earnings, with a 30.6x Uniform P/E. At these valuations, the market is pricing in expectations for Uniform ROA to expand from 28% in 2019 to a high of 40% in 2024, accompanied by 4% Uniform Asset growth going forward.

However, analysts have less bullish expectations, projecting Uniform ROA to expand to 29% by 2021, accompanied by 5% Uniform Asset growth.

EL has historically seen robust profitability, with Uniform ROA improving materially since the recession. Uniform ROA faded from 17% to a historical low of 11% in 2009. Then, after recovering to 21%-23% levels from 2012-2016, Uniform ROA expanded further, to a historical peak of 28% in 2019. Meanwhile, Uniform Asset growth has been somewhat consistent, positive in 14 of the past 16 years, while ranging from -4% to 17%.

Performance Drivers – Sales, Margins, and Turns

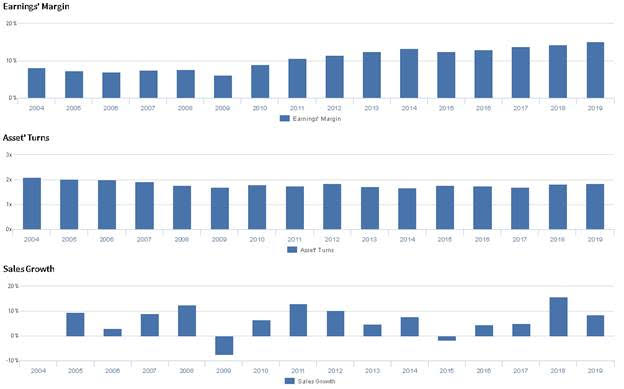

Improvements in Uniform ROA have been driven by improving Uniform Earnings Margin, offset slightly by compressing Uniform Asset Turns. After remaining stable at 7%-8% levels from 2004-2008, Uniform Margins fell to a low of 6% in 2009, before steadily recovering to 12%-13% levels in 2012-2016, and expanding to a peak of 15% in 2019. Meanwhile, after declining from 2.1x to 1.9x in 2003 to 2007, Uniform Turns further declined to 1.7x-1.8x levels from 2008 to 2017, before improving to 1.9x in 2019. At current valuations, markets are pricing in expectations for both Uniform Margins and Uniform Turns to continue expanding to new highs.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q4 2019 earnings call highlights that management is confident they are adding new distribution to their travel retail business, and they are confident in the strength of their creative assets under their Tmall partnership.

However, management is also confident their global travel retail business is flat to declining in the US, and they may lack confidence in their ability to sustain recent growth in their top brands. Furthermore, they may be concerned about the value of their digital spend, and they may lack confidence in their ability to expand digitally in China. In addition, they may be concerned about the impact of the Hong Kong protests on profitability and in their ability to meet their full-year margin guidance. Finally, management may be concerned about further declines in Prestige Beauty in North America.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for EL than as-reported metrics reflect. As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate EL’s profitability. For example, as-reported ROA for EL was 13% in 2018, materially lower than Uniform ROA of 28%, making EL appear to be a much weaker business than real economic metrics highlight. Moreover, while as-reported ROA has fallen from 15% in 2014 to 13% in 2018, Uniform ROA has expanded from 22% to a historical peak of 28% over the same period, distorting the market’s perception of the firm’s recent profitability trends.

Today’s Tearsheet

Today’s tearsheet is for Pepsi. Pepsi trades at a premium to market valuations. The market is pricing the company for modest EPS growth going forward, below historical levels. However, the company is forecast to have weaker growth going forward. The company’s earnings growth is below peer average levels, but the company is trading at a premium to peer valuations. The company has strong profitability, but also does have cash flow risk to their dividend.

Regards,

Joel Litman

Chief Investment Strategist