This underappreciated consulting company may be delivering more value than well-regarded firms like McKinsey

When thinking about consulting companies, of course most people are likely to think about well-established firms such as any of the Big Four.

However, the most prominent consulting firms are not always the ones creating more value.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

When most people are asked to think of consulting firms, they right away think of companies such as McKinsey and Boston Consulting Group.

They can picture prestigious partners wheeling in high paid MBAs to help firms fix a strategy that management didn’t even know was broken.

People also think of companies like Accenture (ACN) that come in to help companies, with an army of information technology (IT) and accounting experts to help with tasks like SAP and PeopleSoft implementations.

The main value consultants bring to the table is to help a company make tough decisions and implement new technologies, along with stop-gap solutions to get a company running better, faster, and more efficiently.

However, when it comes to designing products, an integral part of most businesses, the story drastically changes.

Companies will naturally view designing products as their core competency. If not, they will seek out industry partners to provide support in that area of the business.

However, they can only find so much talent externally. It is difficult to find high quality industry partners that have a diverse skill set in designing products.

When companies can no longer find quality industry partners, they turn to EPAM Systems (EPAM). This is the company’s bread and butter market.

While other consultants mainly focus on soft skills, EPAM Systems covers the entire value chain. The company’s diverse skill set is where their true value comes from.

They can thrive in soft skills, but they can also help companies design both real and physical products, engineer processes, and can even design business plans that are ready to be taken to a market.

This is real value creation, and it is a service most companies likely utilize at one point or another during their lifespan.

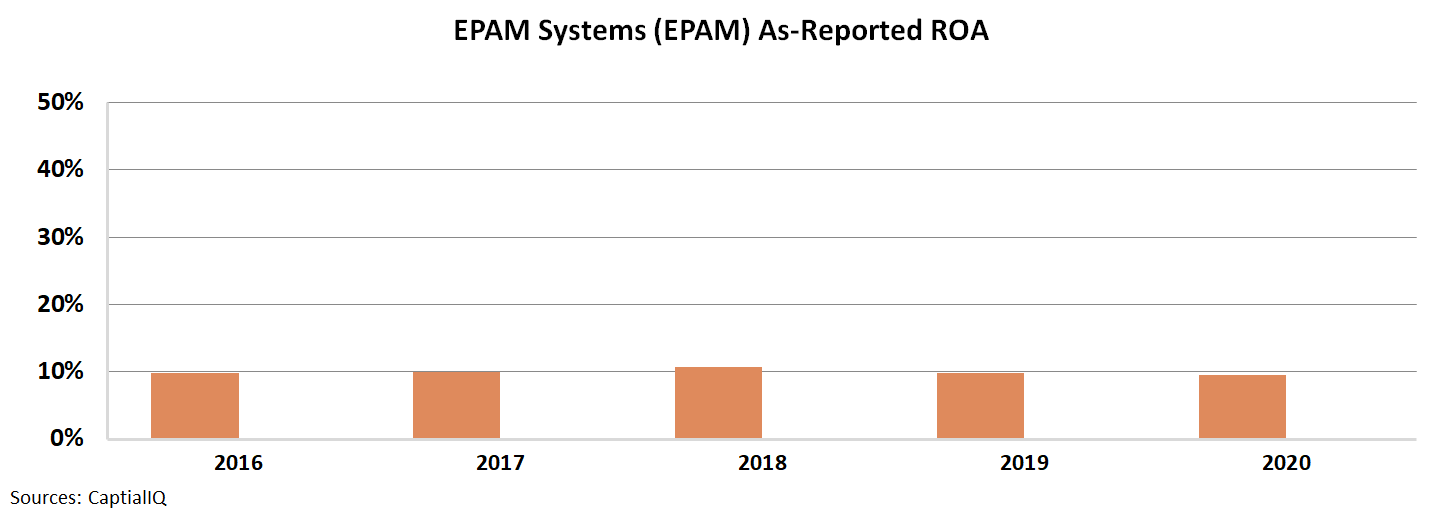

However, while other consulting companies like Accenture regularly earn impressive returns of around 40%, EPAM Systems’ asset intensive approach to market has appeared to hold down its returns.

Specifically, the company’s as-reported return on assets (ROA) have failed to break 10%-11% levels over the past 5 years.

See for yourself below.

This is only true until investors look deeper into the accounting distortions for the company. In reality, the company is printing money.

The company’s Uniform ROA trend is robust and on an upward trend.

Specifically, Uniform ROA levels have expanded from 25% in 2016 to 45% just last year in 2020.

See for yourself below.

Once investors begin to use Uniform Accounting to view EPAM Systems, they realize being a complete solution for clients translates into robust returns.

The company can charge higher premiums than the average as their services are so valuable. As more and more people rely on EPAM Systems’ design expertise, along with all of its other services, the business continues to profit.

SUMMARY and EPAM Systems, Inc. Tearsheet

As the Uniform Accounting tearsheet for EPAM Systems, Inc. (EPAM:USA) highlights, the Uniform P/E trades at 64.3x, which is above the global corporate average of 23.7x and its own historical P/E of 42.3x.

High P/Es require high EPS growth to sustain them. In the case of EPAM Systems, the company has recently shown a 30% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, EPAM Systems’ Wall Street analyst-driven forecast is a 25% and 20% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify EPAM Systems’ $508 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 27% annually over the next three years. What Wall Street analysts expect for EPAM Systems’ earnings growth is below what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is 8x the long-run corporate average. Also, cash flows and cash on hand are 11x its total obligations—including debt maturities and capex maintenance. In addition, intrinsic credit risk is 30bps above the risk-free rate. All in all, this signals a low credit risk.

To conclude, EPAM Systems’ Uniform earnings growth is in line with its peer averages, and the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research