EPR Properties may be the dark horse of the pandemic recovery

While the COVID-19 pandemic has cast a long shadow on many industries, those in the movie and entertainment business have been hit especially hard.

Not only were movie theaters empty during the pandemic, but they also took a long-term hit from the massive uptake in streaming services as a result of the At-Home Revolution.

Combining these two trends seems like a death sentence for the industry. However, the market is pricing movie theater companies to see an impressive recovery.

Despite these expectations, the market seems less enthused about the REITs that own the properties the movie chains rent out. Today, Uniform accounting highlights one such name investors may want to keep an eye on.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

For most of the past year, the one industry most concerned about a resurgence of COVID-19 and subsequent lockdown restrictions has been the theater business.

From the very beginning of the COVID-19 crisis, movie chain and theater operators have scrambled to survive, as government restrictions to slow the spread of the virus and weak consumer confidence shuttered their businesses.

It’s not just that many consumers feel uncertain about being crammed into a packed movie theater in the midst of a pandemic. The pressure on the entertainment industry has another, perhaps more threatening, dimension as well.

Thanks to the At-Home Revolution, powerful movie studios have started to explore new ways of bringing content to viewers, ones that rely less on in-person cinemas and more on streaming.

Facing competition from the likes of Netflix (NFLX), which saw its subscriber base explode as consumers were stuck at home for months, studios such as Time Warner have begun releasing movies on their own streaming platforms the same day as they go live in theaters.

The idea is to draw more attention to platforms like HBO Max by offering customers the chance to forgo the usual wait time after a movie is released on the big screen before it becomes more widely available at home.

While the combination of COVID-19 disruption and the streaming wars led to fears that companies like AMC Entertainment (AMC) would go bankrupt—of course, before it became an $18 billion meme stock—it also directly impacted those who own the properties theater operators rent.

These Real Estate Investment Trusts (“REITs”) involved in the entertainment industry rely on payments from their tenants. If a cinema operator like AMC were to go bankrupt, payments due to the REIT that owns the property would dry up.

One such REIT with significant entertainment exposure is EPR Properties (EPR), which counts theaters as 46% of its tenant base.

Because of the headwinds from streaming competition and the continuing pandemic, the market is pricing EPR as if theater companies will never recover to pre-pandemic levels of profitability.

This comes in contrast to expectations for the theater companies themselves, which the market is pricing to see recover impressively as virus concerns abate and movie-goers return to the big screen.

Not only is there a mismatch between expectations, but there is also the fact that EPR has a much more resilient business underneath its theater exposure.

The company is the largest owner of Top Golf properties across the country, which at 26% of its business gives EPR exposure to a booming At-Home Revolution name in a secular growth area.

Combining this Top Golf growth story with a potential recovery in the theater business, one would think EPR is primed for success.

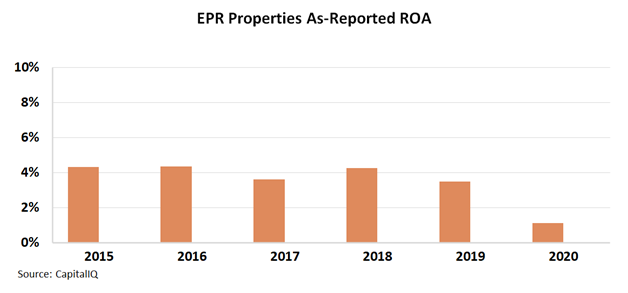

However, on an as-reported basis, it is understandable why investors are hesitant to pay attention to the name.

Even before the pandemic, it appears EPR was a 4% return on assets (“ROA”) firm at best, right around average cost of capital levels for REITs.

In reality, Uniform Accounting metrics highlight that a strong theater business can support returns much higher than the average REIT.

Excluding the pandemic disruption of 2020, EPR’s Uniform ROA was around 7% a year, well above many of its peers.

Uniform Accounting shows us that EPR is a much stronger business than the market currently suspects.

If the recovery in movie theaters plays out, which the market is currently pricing in, and the company continues to benefit from secular growth trends from its Top Golf client, this REIT could be one to keep an eye on.

SUMMARY and EPR Properties Tearsheet

As the Uniform Accounting tearsheet for EPR Properties (EPR:USA) highlights, the Uniform P/E trades at 26.7x, which is above the global corporate average of 24.3x but below its historical P/E of 34.8x.

High P/Es require high EPS growth to sustain them. In the case of EPR Properties, the company has recently shown a 114% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, EPR Properties’ Wall Street analyst-driven forecast is a 249% EPS shrinkage in 2021 and 158% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify EPR Properties’ $52 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 20% annually over the next three years. What Wall Street analysts expect for EPR Properties’ earnings growth is way below what the current stock market valuation requires in 2021, but well above that requirement in 2022.

Furthermore, the company’s earning power in 2020 is below the long-run corporate average. Moreover, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a high credit and dividend risk.

Lastly, EPR Properties’ Uniform earnings growth is below peer averages. However, the company is trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research