It’s not just the tech companies that will benefit from the Internet of Things

The Internet of Things (IoT) promises to revolutionize transportation, manufacturing, data collection, and more. Smart investors are looking for places to put their money to work behind this compelling tailwind.

However, many IoT startups are already being priced in to change the world by investors. To find the alpha behind this trend, we have to find the vital suppliers of the industry.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

One of the most popular investment themes nowadays is the “Internet of Things,” or IoT.

While a device like a Wi-Fi enabled toaster that sings you Happy Birthday is a fun party trick, the real IoT opportunities lie deeper within industry.

The fundamental reason behind the rise of IoT in agriculture, energy, manufacturing and healthcare is that human error can be astronomically expensive.

In 2019 alone, nearly a quarter of all unplanned manufacturing downtime was due to human error.

Smart devices that communicate with each other can replace workers in many applications, and they never get distracted, take lunch breaks, or simply forget to turn a valve on time.

More commonly, however, IoT devices would work together with workers to keep them as informed and safe as possible.

The 2010 British Petroleum (BP) Deepwater Horizon oil spill, for example, was caused by the failure of an unmonitored blowout protector. To prevent a repeat of that disaster, there are now sensors that can send notifications directly to workers near and far should this component fail, and can automatically seal the pipes to avoid a similar catastrophe.

There are other opportunities in self-driving long-haul trucks, farmland management drones, livestock geo-trackers, sensors for predictive maintenance on machinery, and a whole host of other clever applications for internet-enabled gadgets.

The IoT market is expected to grow by 25% per year to a total value of $1.6 trillion by 2025.

And although the train may have already left the station, there are still plenty of ways for savvy investors to catch up and hop on.

One company, Eaton Corporation (ETN:USA), may give you some ideas.

The market is well aware of where IoT is going. Startups are getting record valuations, and many public companies are already expensive.

Eaton, however, serves the IoT world differently.

For the connected devices to exist, someone needs to make the basic motors, pumps, sensors, and raw components. Eaton, in effect, is the pickaxe supplier to the IoT gold rush.

Companies that fill this type of role in their respective industries often get noticed after the all-star innovators become un-investable given all of the attention they’ve garnered. It’s a sneaky way to “get in” when some may think it’s too late.

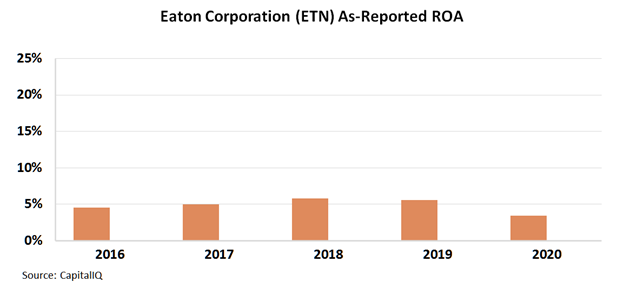

On the surface, however, Eaton does not seem to be worth looking into. Breaking down the firm’s as-reported return-on-assets (ROA), we see that it appears to demonstrate economic profitability right around the cost of capital.

The reality is starkly different. The low returns are the consequence of distortions and inconsistencies inherent to the rules of the Generally Accepted Accounting Principles, or GAAP, that are the standard by which American companies report their financials.

GAAP figures often fail to reflect true economic productivity, so we dig through the dirt to uncover the actual metrics investors should be looking at.

Eaton is not merely a cost-of-capital return business. In fact, during the pre-pandemic years, it generated a 15%-20% ROA – well above the corporate average. Even during the pandemic, which hit manufacturing especially hard, Eaton was far more profitable than its as-reported figures suggest.

See for yourself:

Eaton is a strong company that provides essential components to a high-growth industry. This is a formula that has worked for investors in the past, and will continue to do so.

But the equity market is deeply competitive. Alongside the good fundamentals, to make sure a stock is a buy means understanding the market’s expectations.

Valens Research’s tools not only demonstrate the GAAP distortions that most investors would typically never see, but also the degree to which future expectations are already priced into a stock.

Demand for IoT components is booming and will continue to grow, and we believe some other members of the American Mittelstand may be more compelling buys than Eaton.

If you want to see which ones we like the most, you can get access to our Conviction Long List and our other newsletters by clicking here.

SUMMARY and Eaton Corporation plc Tearsheet

As the Uniform Accounting tearsheet for Eaton Corporation plc (ETN:USA) highlights, the Uniform P/E trades at 27.4x, which is above the global corporate average of 23.7x and its own historical average of 23.4x.

High P/Es require high EPS growth to sustain them. That said, in the case of Eaton, the company has recently shown a 38% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Eaton’s Wall Street analyst-driven forecast is a 51% and 19% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Eaton’s $154 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 12% annually over the next three years. What Wall Street analysts expect for Eaton’s earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 2x above the long-run corporate average. Also, cash flows and cash on hand are above its total obligations—including debt maturities, capex maintenance, and dividends. Meanwhile, intrinsic credit risk is 60bps. All in all, this signals a low dividend and credit risk.

To conclude, Eaton’s Uniform earnings growth is significantly above its peer averages, and the company is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research