Moody’s is panicked about theoretical risk to a company, Uniform Accounting shows why investors should ignore Moody’s yet again

Google’s transition from a partner to a competitor has become a major obstacle to many online firms, resulting in significant profitability pressure.

This firm shows that, despite robust cash flows and ample cash on hand, Moody’s may be overly distracted by Google-related headline risks. Instead of paying attention to economic reality, it’s giving this company a cross-over rating, despite investment-grade fundamentals.

Below, we show how Uniform Accounting restates financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

For many years, Google (GOOGL) operated as a partner to the travel services industry. Its search engine and ad platform allowed travel services firms, such as Expedia Group (EXPE), reach a broader audience.

As a result, Expedia started to rely heavily on the partnership with Google, who helped to attract a large portion of its site traffic.

For many years, the partnership was a win-win for both firms. Expedia could attract more travelers to its site to book stays. Google could continue to grow its ad revenues.

However, recently Google started to turn its focus on a bigger prize. Instead of being the advertisement vendor to travel sites, it could leverage its platforms to enter the travel services industry directly.

First, by offering airplane bookings, and eventually, by offering hotel bookings, Google continued to encroach on Expedia’s core business. As a result, it transitioned from being Expedia’s partner to one of its chief competitors.

Meanwhile, Expedia’s other biggest pure-play rival, online travel company Booking Holdings (BKNG) had been preparing itself for the increase in competition.

Much larger than Expedia, Booking had been accumulating an unmatched portfolio of travel destinations and powerful travel site brands such as Booking.com, Kayak, and Priceline.com that helped make it less reliant on Google’s advertising.

In addition, it had made a concerted effort to diversify into new complementary businesses, such as car reservations, through rentalcars.com, and restaurant reservations, through OpenTable.

This strategy allowed the firm to rapidly grow its revenue by offering an all-inclusive service, and it was able to largely overcome potential headwinds from Google’s entrance.

Expedia wasn’t so lucky. It’s been getting squeezed from all sides.

The firm attempted to scale unsuccessfully by simply taking on more customer inventory. Meanwhile, board members called for antitrust scrutiny into Google’s practices and CEO Mark Okerstrom questioned whether Google was playing on a “level playing field”.

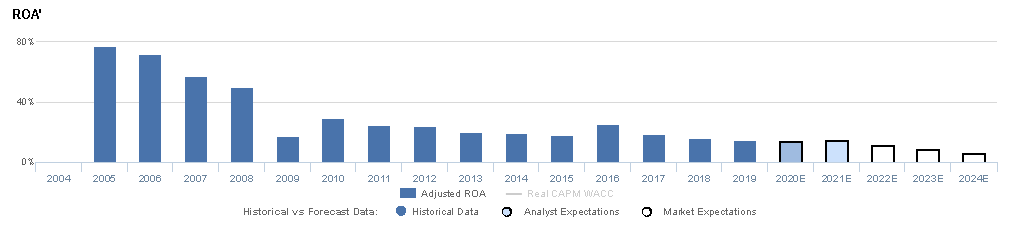

The inability to adapt led to a massive decline in profitability, with Uniform ROA declining from 25% in 2016 to a historical low of 11% in 2019, well off of Expedia’s historical highs of 77%, as seen in 2005.

The encroachment on its business and seemingly panicked response by management makes it clear that the firm may have operational risks going forward. Therefore, it seems to make perfect sense that Moody’s would rate Expedia as a cross-over credit risk with its Baa3 rating.

However, by using Uniform Accounting, and by focusing on the numbers, we can get a clearer picture of the firm’s credit profile and whether or not it can pay off its debt obligations, which should be the main determinant of credit risk.

Currently, the firm has approximately $4.9 billion in debt, but it also has about $3.8 billion in cash and short-term investments. This means the firm has a net debt position of only $1 billion.

Meanwhile, its Uniform cash from operations is around $3 billion a year, suggesting that the firm can take itself from a net debt position to a net cash position by utilizing just a third of a year’s worth of operating cash flow. It can do this even after operating pressures have caused an over 10% drop in profitability in recent years.

Expedia once again shows how Moody’s and the other credit agencies are missing the mark on accurately portraying credit risk.

Moody’s seems to be overreacting to headline risk that isn’t real, at least not in terms of credit and cash flows. The rating agency is completely ignoring the company’s fundamentals.

Using Uniform Accounting we can see why a cross-over rating for a firm with strong cash flows and ample cash on hand is ridiculous. Expedia deserves an investment-grade rating, which we’ve given with our IG3+, equivalent to an A1, rating.

When investors pay more attention to economic reality as opposed to Moody’s distorted as-reported accounting analysis, they get a better understanding of where credit risk truly lies.

Credit Markets Disregard EXPE’s Strong Cash Flows and Healthy Expected Cash Build

Credit markets are grossly overstating credit risk, with a cash bond YTW of 11.690% and a CDS of 469bps, relative to an Intrinsic YTW of 2.070% and an Intrinsic CDS of 169bps.

Meanwhile, Moody’s is materially overstating the firm’s fundamental credit risk, treating EXPE as a cross-over credit, with its Baa3 rating five notches lower than Valens’ IG3+ (A1) rating.

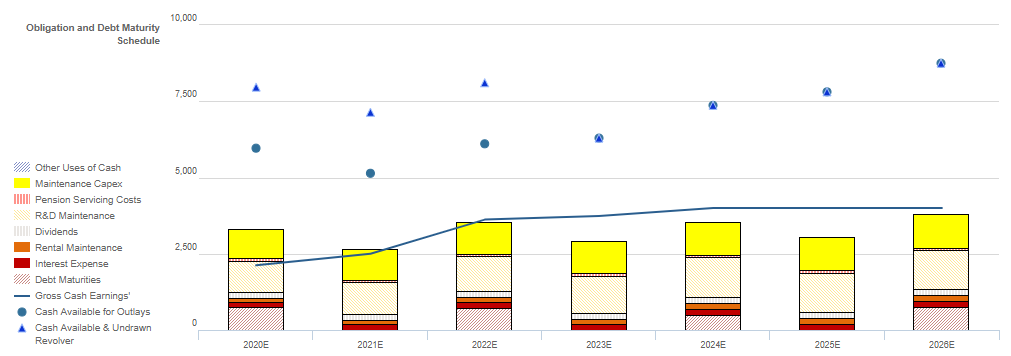

Fundamental analysis highlights that EXPE’s cash flows alone would exceed all obligations including debt maturities in each year after 2022, including material debt maturity headwalls of $725mn, and $497mn in 2022 and 2024, respectively.

Furthermore, even if cash flows weaken significantly in the near-term, a healthy liquidity position should allow the firm to service all obligations including a debt headwall in 2020.

Moreover, the firm’s robust 170% recovery rate on unsecured debt and a sizeable market capitalization should allow them easy access to credit markets to refinance, if necessary.

Incentives Dictate Behavior™ analysis highlights mixed signals for creditors.

Management’s compensation framework should drive management to focus predominantly on growth and margins.

This may incentivize overspending on capex and increased leverage, which may lead to ROA compression and weaker cash flows for servicing debt, even as the management team successfully executes on driving growth.

That said, although most management members do not own substantial EXPE equity relative to their annual compensation, Chairman Diller’s significant holdings may lead him to influence other NEOs to align with shareholders for long-term value creation.

Moreover, management members have low change-in-control compensation, indicating they are not well incentivized to seek a sale or accept a buyout of the company, reducing event risk for creditors.

Earnings Call Forensics™ of the firm’s Q4 2019 earnings call (2/13) highlights that management may be concerned about the impact of COVID-19, their market by market approach, and Google’s consistent infringement on their business and profitability.

In addition, they may lack confidence in their ability to reduce exposure to SEO, drive growth in the second half of the year, and outperform competition in the long-term.

Furthermore, they may be concerned about losing share to hotels, the progress of their CEO search, and the potential of taking on more inventory risk.

EXPE’s strong cash flows, healthy expected cash build, and robust recovery rate indicate that credit markets and Moody’s are overstating credit risk. As such, a tightening of credit spreads and a ratings improvement are likely going forward.

SUMMARY and Expedia Group, Inc. Tearsheet

As the Uniform Accounting tearsheet for Expedia Group, Inc. (EXPE) highlights, the company trades at a 22.4x Uniform P/E, which is around both global corporate average valuation levels and historical average valuations.

Corporate average P/E’s require fairly average EPS growth to sustain them. In the case of Expedia, the company has recently shown an 11% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Expedia’s Wall Street analyst-driven forecast projects a 62% decline in earnings in 2020. This rebounds to a 137% growth in earnings in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $49 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels for Expedia, the company would just have to have Uniform earnings shrink by 10% or less each year over the next three years.

However, Wall Street analysts’ expectations for Expedia’s earnings growth are below what the current stock market valuation requires in 2020, but far above the requirement in 2021.

In addition, Expedia’s Uniform earnings growth is below peer averages, while the company is trading in line with peer valuations.

Meanwhile, the company’s earnings power is 2x corporate averages, signaling very low risk to its dividend or operations.

To summarize, Expedia Group, Inc. is expected to see below average Uniform earnings growth in 2020, which is expected to recover in 2021. As a result, the company is somewhat justifiably trading at average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research