This famous fund manager made double-digit returns while distracted by a legal battle

Fund managers usually make the headlines with their exceptional performances, both in good or bad directions, but sometimes they make the headlines with their personal life.

This is what Israel (“Izzy”) Englander, founder of Millennium Management, has been experiencing recently due to his controversial divorce.

However, his fund made double-digit returns last year in a challenging market environment while he was dealing with the legal battle.

Let’s have a look at the fund from the Uniform Accounting lens and see if this distraction could affect his positioning for the year ahead.

In addition to examining the portfolio, we include a deeper look into the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Also below is a detailed Uniform Accounting tearsheet of the fund’s largest holding.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

Izzy Englander has been in the news recently due to a legal battle regarding his divorce.

His wife, Caryl Englander, is saying that Izzy forced her to sign a post-nuptial agreement to cut her out of much of his money.

Caryl claims that in order to get the signature, the famous fund manager has been conducting a “yearslong campaign of pressure and coercion.”

The agreement takes away billions of dollars from Caryl in shared marital assets, which the couple has accumulated over 40 years of their marriage.

Media argues that Izzy has been trying to punish his ex-wife as she falls in love with another woman after growing apart from him in 2016.

According to Bloomberg Billionaires Index, Izzy Englander has a net worth of around $11.5 billion, and with the agreement, he is taking more than 95% of the marital assets.

Additionally, he is almost taking total control of the few assets and funds available to Caryl.

While he’s not doing a great job running his personal life, he had a banner year last year in his fund, Millennium Management.

The fund made double-digit returns last year in a challenging market environment where S&P 500 companies lost around 19%.

This performance is incredible for a year with chaos in the markets due to the Russian invasion of Ukraine, which exacerbated the existing global supply chain problems.

Now, Millennium investors could be worried about whether the fund can continue this stellar performance for the year ahead or not due to Englander’s personal issues.

Let’s check in on his fund’s top holdings using the Uniform Accounting to make sure this legal battle isn’t distracting him from continuing to put points on the board.

Economic productivity is massively misunderstood on Wall Street. This is reflected by the 130+ distortions in the Generally Accepted Accounting Principles (GAAP) that make as-reported results poor representations of real economic productivity.

These distortions include the poor capitalization of R&D, the use of goodwill and intangibles to inflate a company’s asset base, a poor understanding of one-off expense line items, as well as flawed acquisition accounting.

It’s no surprise that once many of these distortions are accounted for, it becomes apparent which companies are in real robust profitability and which may not be as strong of an investment.

See for yourself below.

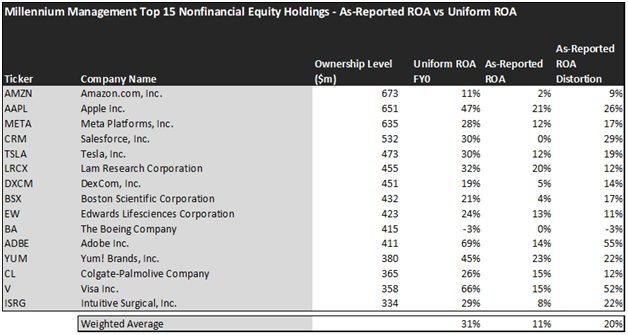

Looking at as-reported accounting numbers, investors would think that investing in Millennium Management is not really rewarding.

On an as-reported basis, many of the companies in the fund are just average performers. The average as-reported ROA for the top 15 holdings of the fund is 11%, which is slightly below the U.S. corporate average of 12%.

However, once we make Uniform Accounting adjustments to accurately calculate the earning power, we can see that the average return in Millennium Management’s top 15 holdings is actually 31%.

As the distortions from as-reported accounting are removed, we can see that Salesforce (CRM) isn’t an unprofitable business with 0% returns. Its Uniform ROA is 30%.

Meanwhile, Adobe (ADBE) looks like a 14% return business, but this multinational computer software company actually powers a 69% Uniform ROA.

To find companies that can deliver alpha beyond the market, just finding companies where as-reported metrics misrepresent a company’s real profitability is insufficient.

To really generate alpha, any investor also needs to identify where the market is significantly undervaluing the company’s potential.

These dislocations demonstrate that most of these firms are in a different financial position than GAAP may make their books appear. But there is another crucial step in the search for alpha. Investors need to also find companies that are performing better than their valuations imply.

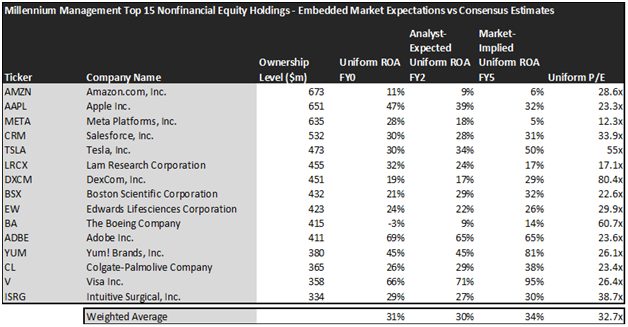

Valens has built a systematic process called Embedded Expectations Analysis to help investors get a sense of the future performance already baked into a company’s current stock price. Take a look:

This chart shows four interesting data points:

- The average Uniform ROA among Millennium Management’s top 15 holdings is actually 31% which is much better than the corporate average in the United States.

- The analyst-expected Uniform ROA represents what ROA is forecasted to do over the next two years. To get the ROA value, we take consensus Wall Street estimates and convert them to the Uniform Accounting framework.

- The market-implied Uniform ROA is what the market thinks Uniform ROA is going to be in the three years following the analyst expectations, which for most companies here are 2023, 2024, and 2025. Here, we show the sort of economic productivity a company needs to achieve to justify its current stock price.

- The Uniform P/E is our measure of how expensive a company is relative to its Uniform earnings. For reference, the average Uniform P/E across the investing universe is roughly 20x.

Embedded Expectations Analysis of Millennium Management paints a clear picture. Over the next few years, Wall Street analysts expect the companies in the fund to slightly decline in profitability, but the market does not agree with analysts and thinks returns will improve.

Analysts forecast the portfolio holdings on average to see Uniform ROA decline to 30% over the next two years. At current valuations, the market thinks differently from the analysts and expects a 34% Uniform ROA for the companies in the portfolio.

For instance, Dexcom (DXCM) returned 19% this year. Analysts think its returns will fall slightly to 17%. And at an 80.4x Uniform P/E, the market expects a significant improvement in profitability and is pricing Uniform ROA to be around 29%.

Similarly, Edwards Lifesciences’ (EW) Uniform ROA is 24%. Analysts expect its returns will drop to 22%, but the market is pricing its returns to rise to 26%.

Overall, Millennium Management, led by Izzy Englander, has well-regarded and high-quality companies in its portfolio. However, the high market expectations may limit the upside potential for these names at current valuations. Additionally, his personal issues and distractions, coupled with recession concerns and high market expectations may lead to some downside risk for its investors. That is why investors should be careful and should analyze the current valuations along with the market’s expectations before making an investment decision.

This just goes to show the importance of valuation in the investing process. Finding a company with strong profitability and growth is only half of the process. The other, just as important part, is attaching reasonable valuations to the companies and understanding which have upside which has not been fully priced into their current prices.

To see a list of companies that have great performance and stability also at attractive valuations, the Valens Conviction Long Idea List is the place to look. The conviction list is powered by the Valens database, which offers access to full Uniform Accounting metrics for thousands of companies.

Click here to get access.

Read on to see a detailed tearsheet of one of Millennium Management’s largest holdings.

SUMMARY and Amazon.com, Inc. Tearsheet

As one of Millennium Management’s largest individual stock holdings, we’re highlighting The Amazon.com, Inc. (AMZN:USA) tearsheet today.

As the Uniform Accounting tearsheet for Amazon.com, Inc. highlights, its Uniform P/E trades at 28.6x, which is above the global corporate average of 18.4x, but below its historical average of 35.4x.

High P/Es require high EPS growth to sustain them. In the case of Amazon.com, Inc., the company has recently shown 22% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Amazon.com, Inc.’s Wall Street analyst-driven forecast is for EPS to shrink by 14% in 2023 and grow by 20% in 2024.

Furthermore, the company’s return on assets was 11% in 2022, which is 2x the long-run corporate averages. Also, cash flows and cash on hand consistently exceed its total obligations—including debt maturities and CAPEX maintenance. Moreover, its intrinsic credit risk is 30bps above the risk-free rate. Together, these signal low operating risks and low credit risks.

Lastly, Amazon.com, Inc.’s Uniform earnings growth is in line with peer averages, and above peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research