Demand for American energy isn’t going anywhere

Europe is shifting away from Russian energy supplies in favor of American alternatives.

Diamondback Energy (FANG), specializing in the exploration and extraction of oil and natural gas, plays an important role in this scenario.

With extensive reserves of onshore oil and natural gas coupled with its operation of midstream infrastructure assets, the company is well-positioned to meet Europe’s evolving energy demands.

Given Europe’s strong commitment to reducing dependence on Russian gas and the expected prolonged period of elevated energy prices, Diamondback’s assets are poised for significant demand.

Also below, is the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The Ukraine conflict has had a profound impact on the global energy landscape, extending far beyond Ukraine’s borders.

It caused European nations to quickly reevaluate their energy supply chains due to the realization of their vulnerability to Russian sources. Russia supplied 40% of the European Union’s natural gas demand, making this dependence a critical concern.

As a response, these European nations began a significant shift away from Russian energy sources. This shift disrupted well-established energy trade routes, resulting in sudden supply shortages.

Russia, as a dominant player in the oil and gas sector, accounted for 14% of the world’s crude oil production and 8% of the global liquid natural gas supply in 2021. Consequently, detaching from Russian sources proved to be a formidable challenge.

Europe’s pursuit of new energy sources raised the demand for American alternatives, which meant more cash flowing into owners of energy reserves in the Western Hemisphere.

One of these owners is Diamondback Energy (FANG), an oil and natural gas company that stands at the forefront of addressing Europe’s energy needs.

The company boasts substantial onshore oil and natural gas reserves in some of the United States’ most prolific basins; including the Permian Basin, Midland Basin, and Delaware Basin.

These reserves position Diamondback Energy as a reliable source of energy supply for Europe, as they provide a diverse range of hydrocarbon resources that can meet various energy demands.

Furthermore, the company’s operations extend beyond production. It also owns and operates midstream infrastructure, including crude oil and natural gas pipelines and integrated water systems.

This vertical integration not only ensures a stable supply of energy resources but also facilitates their transportation, storage, and distribution. Having control over midstream assets is a strategic advantage that sets Diamondback Energy apart.

You can see this competitive advantage by looking at how profitable the company is.

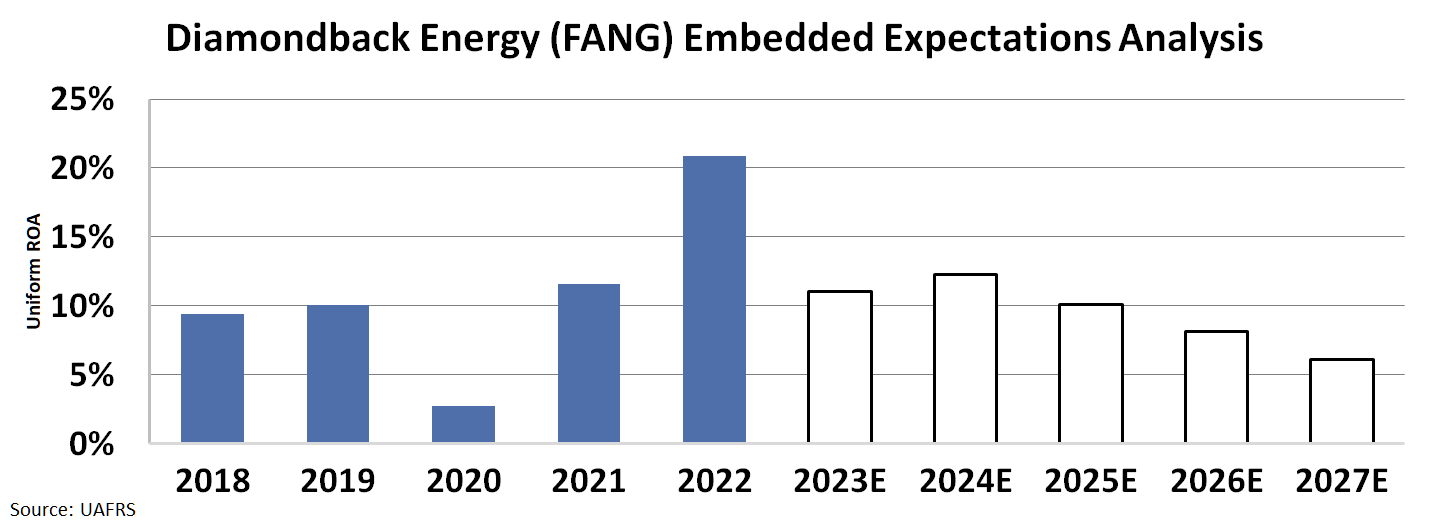

During the pandemic, transportation networks worldwide faced severe limitations, leading to a significant downturn in oil demand. Consequently, the company’s Uniform return on assets (“ROA”) plummeted to 3% in 2020 from 10% in 2019.

But the company orchestrated a swift recovery in 2021 and after that managed to get its ROA to 21% in 2022, the highest ever. All thanks to demand coming from Europe and the Diamondback’s ability to meet that demand…

Europe is unlikely to revert to relying on Russian gas in the near future, keeping energy prices elevated for an extended period.

However, the market thinks this is not the case.

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to return back to 6% levels.

The market’s pessimistic expectation is caused by the belief that demand for Diamondback’s products is going to fall…

The market suspects that the high demand coming from Europe for Diamondback’s products is an exception caused by short-term geopolitical troubles and is not sustainable.

This is very very unlikely.

The demand for American energy is likely to stay high for a long time. As that happens, the profitability of Diamondback Energy should remain high. This might mean an opportunity for investors.

SUMMARY and Diamondback Energy Tearsheet

As the Uniform Accounting tearsheet for Diamondback Energy (FANG:USA) highlights, the Uniform P/E trades at 13.2x, which is below its global corporate average of 18.4x but above its historical P/E of 9.0x.

Low P/Es require low EPS growth to sustain them. In the case of Diamondback Energy, the company has recently shown a 116% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Diamondback Energy’s Wall Street analyst-driven forecast is a 47% EPS shrinkage in 2023 and a 20% EPS growth in 2024.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Diamondback Energy’s $154.19 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 16% annually over the next three years. What Wall Street analysts expect for Diamondback Energy’s earnings growth is below what the current stock market valuation requires in 2023 but above its 2024 requirement.

Furthermore, the company’s earning power is 3x its long-run corporate average. Moreover, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends.Also, the company’s intrinsic credit risk is 80bps above the risk-free rate.

All in all, this signals high dividend risk.

Lastly, Diamondback Energy’s Uniform earnings growth is immaterial to its peer averages but below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research