Finding the Silver Lining in Inflation’s Campervan Cloud

Despite the decline in consumer sentiment, hope remains for Thor Industries (THO), a prominent player in the recreational vehicle (“RV”) industry.

High inflation and elevated interest rates have strangled the RV sector, forcing a reality check upon a once-a-pandemic beneficiary. Consumers’ reduction in discretionary spending and unfavorable lending environments have contributed to the industry’s challenges.

Nevertheless, Thor has positioned itself to weather the storm through a diversified customer base, international pricing power, and strategic acquisitions.

In today’s FA Alpha 50 analysis, we will assess Thor’s sustainability in the face of economic turmoil by examining its returns using Uniform Accounting.

Investor Essentials Daily:

Tuesday FA Alpha 50

Powered by Valens Research

Good news may just be reemerging for certain recreational vehicle (“RV”) companies.

If you have been keeping up with our Investor Essentials Daily articles, then you would know that it has been a tough year for the RV industry.

High interest rates have put pressure on companies’ ability to borrow and have harmed consumers’ ability to finance large discretionary purchases.

Moreover, inflation has increased the costs of vital components, and disruptions in the supply chain only exacerbated the issue.

Though inflation is softening, investors are still weary of the RV industry’s ability to weather a potential hard landing.

As we have been saying for a while now, things could not look much worse for the RV industry, and that is possibly the best news you could hear about it.

Thor Industries (THO) is the leading American RV retailer but is no exception from the industry’s poor performance.

Increased costs of production have shrunk the company’s margins, and lower sales volume has heavily impacted both its domestic and international distribution.

However, Thor shows promising signs of resiliency.

In fact, just over a decade ago, it was able to survive the great recession without making a loss, and fully recovered in just three years.

One reason for the company’s vitality is its level of pricing power. The company has over 3500 customers, who have little bargaining power as they are independent dealers.

Furthermore, the company has a history of acquisitions building toward vertical integration. This allowed it to mitigate the risks of supplier-related cost increases and is focused on building a company that lasts.

The acquisition of Erwin Hymer Group (EHG) in 2019, one of Europe’s largest RV manufacturers, made Thor the second biggest player in European RVs, expanding its dominance past domestic markets.

Overall, Thor’s market share has expanded by 5% since 2014. Although it operates in a cyclical industry, it will continue to be able to leverage its pricing power and scale to surf the choppy waters ahead.

While the backlog for the company is down significantly since its highs in 2022, the European backlog has expanded from $2.88 billion to $3.47 billion. This indicates that while shipments may be down, demand is still high enough for the company to continue hiking international prices.

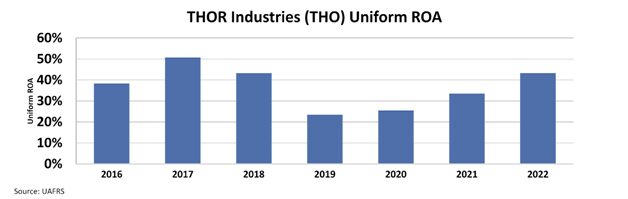

Thor boasts a strong advantage over its peers due to its sheer size. The result is significant negotiating power and a return on assets (“ROA”) that frequently surpasses 40%.

The company’s inorganic growth and pricing power have resulted in huge surges in its profitability, and robust rebounds from downturns as represented by recovery from a 24% ROA in 2019 to 43% in 2022.

Yet, the market sees the operational and demand-side pressures going on in the industry and automatically lumps in Thor with them.

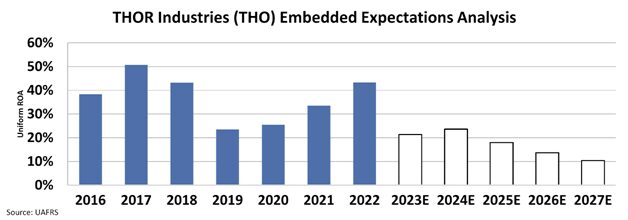

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At today’s price, the market is expecting the company’s ROA to tank to 10%, a level not seen since the great recession.

Expectations are that we are headed back toward another recession similar to the great recession of 2008. We are not, and even if we were, Thor is in a far better position than its competitors.

As a result, its cheap valuation, in combination with its high returns and high growth, make Thor a great FA Alpha 50 name.

Throughout financial market history, many of the world’s most successful investors have been candid in their belief that Generally Accepted Accounting Principles (“GAAP”) distort economic reality.

Warren Buffett, for example, once said investors should “concentrate on the world of companies, not arcane accounting mathematics.”

Investors who neglect the very real issues with as-reported accounting can find themselves caught up in investing with the crowd, blindly following hot “themes” without a thorough grasp of how to understand the businesses in question.

The only true way to focus on the “world of companies,” as Buffett suggests investors do, is to present a clear picture of how a business operates, something that can only be done by adjusting financial statements to reflect the arbitrary nature of certain accounting rules that leave much to discretion.

The world’s best investors understand the need to make these adjustments, which allows them to focus not on picking out the most popular companies but rather on looking for great names in sleepy areas that the market isn’t paying much attention to. From there, the goal is to then identify quality companies with significant growth potential at reasonable prices.

That’s exactly what we’ve set out to do with the FA Alpha, our monthly list of 50 companies that rank at the top for quality, high growth, and low valuations.

This list has outperformed the market by 300 basis points per year for over 20 years now, effectively doubling the performance of the market by focusing on the real fundamentals and valuations of companies with our proprietary Uniform Accounting framework.

See for yourself below.

To see the other 49 names on the list, click here.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research