GAAP accounting misses that Fiserv is at the heart of the monetary revolution

Over the course of history, physical currency in some form has been a staple of civilization and trade, allowing for the seamless exchange of goods and services. Now, the internet is allowing currency to take the next step.

Today, credit cards, wires, and peer-to-peer payments replace cash as payment options. Cash may no longer be king.

This is a big transition taking place globally, and one of the companies that are at the center of this transition is Fiserv (FISV). The company is in a position to help customers speed up the transition and use newly developed payment options with ease.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

It has been nearly 5,000 years since people started using tokens like coins and shells to enhance global commerce – a revolutionary innovation.

As governments and economies continued to evolve, people realized there was a better way of holding and spending money. That is when banknotes were introduced, and coins were replaced.

Now, it seems there is even an easier form of payment, and it promises a similar revolution from the move from gold coins to cash.

The proportion of people carrying cash has become smaller and smaller. While some people still prefer holding cash, most people disagree.

Younger adults are least likely to have cash, as 40% of millennials and 45% of Generation X said they carry it “most of the time” versus 59% of people born between 1946 and 1964. As younger generations eschew the greenback in their pocket, the future will eventually be cash free.

Cash is no longer king, and the ever-developing world of payments replaces it, including credit cards, wires, and now peer-to-peer payments.

This is an amazingly fast transition as well. According to a Boston Consulting Group report, the number of fintech startups doubled in the past two years, rising from over 12,200 in 2019 to 26,000 in 2021.

The fintech sector is forecasted to grow at an annual rate of 20% and the peer-to-peer payments sector is estimated to grow at 17%. These numbers alone would be sufficient to see how the new payment options take the place of cash.

One of the companies at the heart of this transition is Fiserv (FISV).

Fiserv is a global provider of payments and financial services technology solutions. The company works in lots of different areas such as digital banking solutions, card issuer processing and network services, and payments.

It provides these services under its three segments: Merchant Acceptance, Fintech, and Payments. Even though the majority of the company’s revenue comes from the U.S., it is exposed to international business as well.

Considering how ubiquitous the fintech world is, one might think that these services are a commodity. This perception of a glut of fintech companies all performing interchangeable services is only backed up when looking at the as-reported metrics.

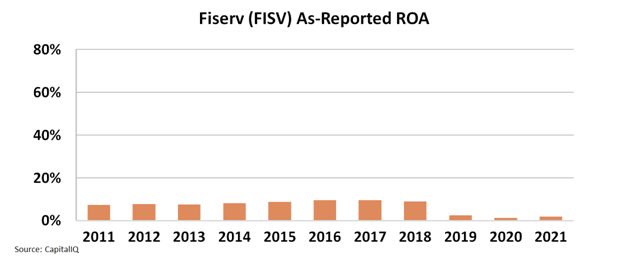

As-reported return on assets (“ROA”) makes it seem like the company struggles with profitability. Not only have returns never crossed corporate average levels of 12% in the last decade, but they have now collapsed to just 1%.

Investors looking at Fiserv’s performance may conclude fintech solutions were never that profitable, and recent competition has sent players like Fiserv into the doldrums.

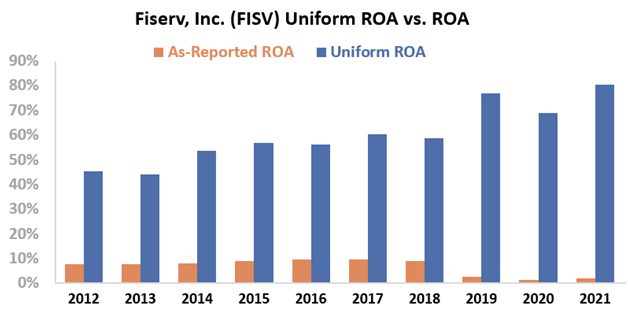

However, this picture of Fiserv’s performance is not accurate. This is due to distortions in as-reported accounting, and can be fixed by making the over 130 adjustments needed under Uniform Accounting.

The reality is that Fiserv plays a key role in a profitable industry, as the transition from cash to other payment options has been gaining pace. The company’s Uniform ROA almost reached 80% in 2021 after steadily improving over the last decade.

The company has been performing much better than anyone using GAAP metrics would guess, all due to the wrong data.

Without Uniform Accounting, investors would miss how strongly Fiserv positioned itself in the industry, and how much fintech is the way of the future for both the industry and payments at large. Without the right data, it’s impossible to understand a company well enough to invest in it.

SUMMARY and Fiserv, Inc. Tearsheet

As the Uniform Accounting tearsheet for Fiserv, Inc. (FISV:USA) highlights, the Uniform P/E trades at 15.8x, which is below the global corporate average of 24.0x and its own historical P/E of 19.8x.

Low P/Es require low EPS growth to sustain them. In the case of Fiserv, the company has recently shown a 5% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Fiserv’s Wall Street analyst-driven forecast is a 26% and 7% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Fiserv’s $98 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 6% annually over the next three years. What Wall Street analysts expect for Fiserv’s earnings growth is above what the current stock market valuation requires through 2023.

Furthermore, the company’s earning power in 2021 is 13x the long-run corporate average. Also, cash flows and cash on hand are at 171% of total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals moderate credit risk.

Lastly, Fiserv’s Uniform earnings growth is above its peer averages, and the company is also trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research