The Market is Too Excited About this Company Being the Gillette of Industrial Machinery

If you’ve been in a business class in the past 20 years, or read any book on great companies, you’ve probably heard about the “razorblade model.”

We use it so regularly in business conversations that you wouldn’t be blamed for forgetting its origin.

King Camp Gillette, the founder of Gillette and inventor of the disposable safety razor is widely quoted as saying “give ‘em the razor, sell ‘em the blades.”

In reality, he didn’t invent the model, and if anything was against the model initially. When the disposable safety razor was invented, he charged a premium for the product, it wasn’t until his patent expired and competitors introduced the strategy that he and the company adopted that philosophy.

But they adopted it impressively, and that philosophy turned Gillette into a $58 billion company by the time it was bought by Procter & Gamble (PG) in 2005.

The strategy was simple. Get people to use the product by basically selling them the razor handle and first blade for cost, to get them to use the inexpensive product. Then, sell them each of the subsequent razors they buy for an impressively high margin, and generate revenue on the recurring purchases.

Don’t worry about making money on getting people in the door, get them in the door and make them have to pay to remain customers.

That business model has been applied to many other businesses since. From printers and printer ink to cable providers giving away the cable boxes to get subscription revenue to name a few examples.

FlowServe (FLS) makes pumps, seals, and valves for various industrial purposes, from refineries and oil & gas rigs to chemical plants, power plants, and water treatment plants.

They don’t sell their pumps for cost, but their pumps are not where their real profit comes from. That is just the installed base they generate their real profits from.

Almost half of Flowserve’s business comes from aftermarket sales, the sale of parts and seals and valves for the pumps they make.

Because of the company’s healthy after-market business, the market has regularly paid a premium for Flowserve. The company’s Uniform P/E has consistently been over market average levels for the past 7 years.

However, the company’s return stream highlights they haven’t been nearly as successful as Gillette has been in turning that “razorblade model” into massive regular cash flow. Returns have been under pressure the last several years.

The market is pricing the company like those issues are now behind it, and is expecting the company to see Uniform ROA recover to prior levels. However, management is showing concerns about EPS, margin, and their aftermarket business that signal the market may be too optimistic about returns improving going forward.

On Friday, we’re highlighting massive as-reported accounting distortions for Facebook, ServiceNow, Jazz Pharma, UnitedHealth, and GrubHub

At noon today, we’ll be hosting a webinar highlighting the massive distortions that are inherent in as-reported accounting.

We’ll be drilling down on why as-reported accounting gets these 5 companies wrong:

Facebook (FB)

ServiceNow (NOW)

Jazz Pharmaceuticals (JAZZ)

UnitedHealth (UNH)

Grubhub (GRUB)

And how, using Uniform Accounting, we can get better insights, understand what the market’s pricing in, and what the company could really be worth.

For example, we’ll be discussing why ServiceNow’s EPS is really $3.37, not -$0.15,

We’ll also discuss how GrubHub is cheaper than investors think, as its P/E is really 44x, not 193x.

To register for the webinar, click here.

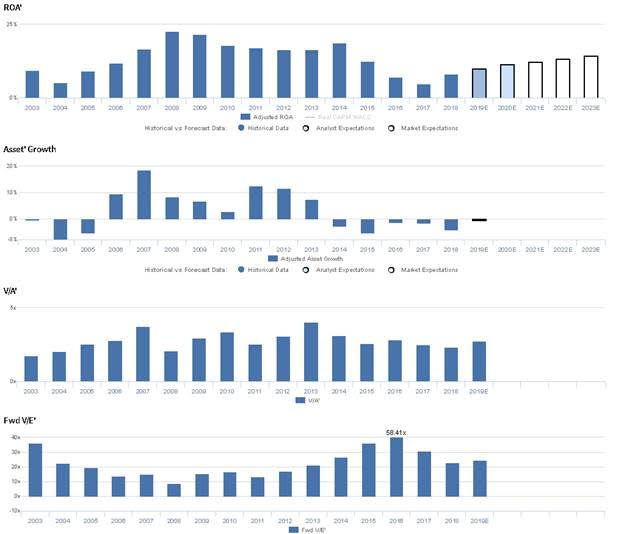

Market expectations are for Uniform ROA to continue to expand, but management may be concerned about their EPS, margin, and aftermarket segment

FLS currently trades above corporate averages relative to UAFRS-based (Uniform) Earnings, with a 24.5x Uniform P/E. At these levels, the market is pricing in expectations for Uniform ROA to rebound from 8% in 2018 to 14% in 2023, accompanied by immaterial Uniform Asset growth going forward.

Analysts have similar expectations, projecting Uniform ROA to rise to 11% by 2020, accompanied by immaterial Uniform Asset shrinkage.

Historically, FLS has seen volatile profitability, with Uniform ROA fading from 9% in 2003 to 5% in 2004, before improving to a peak of 23% in 2008. Subsequently, Uniform ROA declined to 17%-19% levels from 2010-2014, before compressing to a low of 5% in 2017, and most recently recovering to 8% in 2018. Meanwhile, Uniform Asset growth has been similarly volatile, positive in eight of the past 16 years, while ranging from -8% to 19% annually.

Performance Drivers – Sales, Margins, and Turns

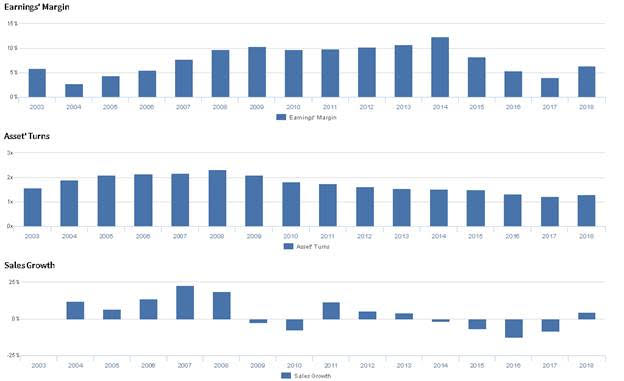

Volatility in Uniform ROA has been driven by trends in both Uniform Earnings Margin and Uniform Asset Turns. Uniform Margins declined from 6% in 2003 to 3% in 2004, before expanding to 10% levels from 2008-2012. Subsequently, Uniform Margins reached a peak of 12% in 2014, before declining to 4% by 2017, and most recently improving to 6% in 2018. Meanwhile, Uniform Turns improved from 1.6x in 2003 to 2.3x in 2008, before gradually declining to a low of 1.2x in 2017, and then improving to 1.3x in 2018. At current valuations, markets are pricing in expectations for continued improvements in both Uniform Margins and Turns.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q3 2019 earnings call highlights that management is confident they have made progress in the industrial sector despite a challenging market environment. However, they may be concerned about further weakness in the MRO market impacting profitability, and they may lack confidence in their ability to secure larger awards above $15 million. Furthermore, they may lack confidence in their ability to sustain growth in their aftermarket segment, and they may be concerned about the sustainability of gross margin improvement. Finally, they may lack confidence in their ability to modernize their inventory tracking system, sustain EPS improvements, and offset mix changes on their margin with lean initiatives.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for FLS than as-reported metrics reflect. As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics understate FLS’s profitability. For example, as-reported ROA for FLS was 5% in 2018, lower than Uniform ROA of 8%, making FLS appear to be a weaker business than real economic metrics highlight. Moreover, since 2003, as-reported metrics have consistently understated Uniform ROA, distorting the market’s perception of the firm’s profitability for over a decade.

Today’s Tearsheet

Today’s tearsheet is for Bristol Meyers Squibb. Bristol trades at a significant discount to market average valuations. The company has recently had impressive Uniform EPS growth, at around 21%. EPS growth is forecast to moderate in 2019 before accelerating rapidly in 2020. At current valuations, the market is pricing the company to see earnings shrink going forward.

The company’s earnings growth for 2019 is at the lower end of peer average levels, but the company is also trading at below peer average valuations. The company has robust returns, and no cash flow risks.

Regards,

Joel Litman

Chief Investment Strategist