This payment processor is thriving during the pandemic and benefits from a surge in e-commerce demand

E-commerce has seen its biggest rise ever during the pandemic. With many in-person stores closed, consumers are turning to online shopping to meet their needs. Companies with exposure to different aspects of the industry are thriving during this period.

Today’s firm is a payment processor for transportation companies. As e-commerce demand picks up, transportation of these goods to consumers is thriving as well.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The pandemic has hit some industries hard while boosting others. We regularly talk about how homebuilders and online platforms have seen increased demand during the pandemic.

People are looking to move out of cities and into spacious homes, creating an influx of new housing demand. Additionally, e-commerce platforms have thrived as in-person shopping has been limited. Dovetailing with the homebuying trend, people are investing in furnishings, entertainment, and all kinds of home-improving purchases, many of which are being ordered online.

One other industry benefiting from this e-commerce boom is the world of transportation infrastructure. As more people order products online, there is an increased need to deliver these goods quickly.

Companies that support the transportation industry have seen strong performances as a result. One name to note in particular is FleetCor Technologies (FLT).

FleetCor provides a business payment platform that allows for easy payment of items like gas, lodging, and tolls, among others. This often includes getting discounts for users of the service. Its goal is to improve the transportation infrastructure and allow e-commerce companies to focus on selling their products.

By being a volume payer, FleetCor can aggregate demand and collect a small percentage of the payment it processes. This is how FleetCor became an asset-light provider of payment solutions. The firm does not need to own the trucks, gas stations, or other capital intensive aspects of transportation.

FleetCor fits the mold for one of our favorite investment stories. It’s asset-light, it fills a niche, and it has several tailwinds pushing it forward. That said, as-reported metrics don’t seem to agree with the thesis.

As-reported return on assets (ROA) was just 7% in 2019, slightly above cost-of-capital returns. It would appear as though FleetCor is merely a commodity business, with no way to differentiate its offerings from competitors in the industry.

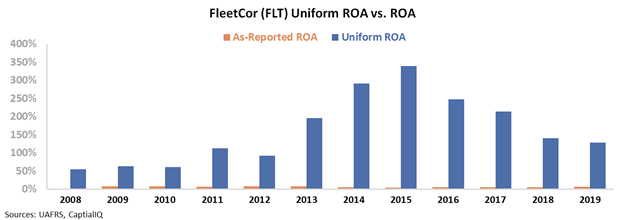

However, this picture of FleetCor’s performance is wildly inaccurate. This is due to distortions in as-reported accounting. These include the treatment of goodwill and other distortions. Wall Street has missed FleetCor’s profitability.

FleetCor’s Uniform ROA has been at least ten times as high as as-reported numbers since 2012. Uniform ROA was a robust 128% in 2019, compared to 7% for as-reported ROA.

FleetCor is not a cost-of-capital business but rather a firm with industry leading returns. FleetCor has been able to create an essential service for companies looking to transport goods.

By being an asset-light provider of payment solutions, FleetCor can benefit from the surge in demand from increased e-commerce spending, without having to make costly investments.

Without Uniform Accounting, investors would miss the strong performance of this payment processor. They might see FleetCor as a firm with cost-of-capital returns, instead of industry leading profitability.

Ultimately, FleetCor should continue to benefit from surging e-commerce and transportation demand. As consumers migrate their shopping life online, demand for FleetCor’s services looks set to increase, and returns may rise in tandem.

SUMMARY and FleetCor Technologies, Inc. Tearsheet

As the Uniform Accounting tearsheet for FleetCor Technologies, Inc. highlights, the Uniform P/E trades at 24.5x, which is around the global corporate average valuation levels and its historical average valuations.

Moderate P/Es require moderate EPS growth to sustain them. In the case of FleetCor, the company has recently shown a 17% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, FleetCor’s Wall Street analyst-driven forecast is a 13% EPS shrinkage in 2020, followed by a 15% EPS growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify FleetCor’s $273 stock price. These are often referred to as market embedded expectations.

The company would need to grow its Uniform earnings by 6% per year over the next three years to justify current stock prices. What Wall Street analysts expect for FleetCor’s earnings growth is below what the current stock market valuation requires in 2020, but above this requirement in 2021.

Furthermore, the company’s earning power is 21x the corporate average. Also, cash flows and cash on hand are slightly above its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals an average credit and dividend risk.

To conclude, FleetCor’s Uniform earnings growth is below its peer averages, while its valuations are traded in line with its average peers.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research