Ratings agencies are lettings sports and politics get in the way of good judgment

Despite secular declines in TV viewership for years, this company’s market positioning has set it up for success.

Credit rating agencies are overly pessimistic over this name, given the firm’s healthy balance sheet, coupled with robust and resilient cash flows.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Investors and industry experts often talk about the slow death of cable television. Some compare cable television and the rise of streaming to horse and buggy with the automobile.

The exception to this secular decline is live sports. With no direct competitor for live sports, cable divisions are able to draw in strong viewership numbers and advertising revenue.

Furthermore, cable news has been able to hold its market sway, particularly in the years President Trump was in office.

As a result, investors might assume ratings agencies and credit investors would be bullish on a company that is largely positioned to benefit from these two macroeconomic tailwinds.

Fox News (FOXA) is the most popular cable news network in America. Furthemore, the company’s Fox Sports platform is one of the largest sports broadcasting networks in the U.S.

The company has fought off the decline in viewership that much of television broadcasting has seen for the past ten years.

This can be seen comparing Fox’s traditional cable broadcast with the company as a whole.

Fox’s broadcasting EBITDA dropped from approximately $770 million in 2016 to roughly $430 million in 2020. However, on an aggregate basis, the company’s EBITDA rose from $2.25 billion to $2.8 billion over the same timeframe.

These two markets still have strong tailwinds.

That being said, credit investors appear to look at Fox and miss how its portfolio is different from the vast majority of its peers.

Despite the firm’s exposure to these unique tailwinds, credit rating agencies are barely rating this name as an investment grade credit.

Specifically, S&P’s rating is currently a BBB, or the low end of investment grade.

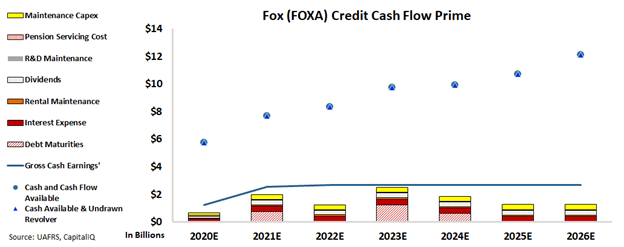

Using our Credit Cash Flow Prime (CCFP) analysis, we are able to get to the heart of the firm’s true credit risk.

In the below chart, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

Our CCFP highlights credit rating agencies are too pessimistic regarding Fox’s financial health.

As depicted, Fox’s cash flows alone consistently exceed all obligations including debt maturities through 2026.

Additionally, the firm has a solid balance sheet with large amounts of cash. This gives the firm further cushion in case any black swan events take place, bolstering the firm’s cash flows.

As such, there is virtually no default risk for Fox over the next five years.

Using the CCFP analysis, Valens rates Fox as an investment grade IG3+ rating. An IG3+ corresponds with a default rate below 1.5% within the next five years and an A+ rating from the S&P.

Uniform Accounting and the Credit Cash Flow Prime analysis highlights how Fox’s credit risk profile lines up with its strong performance in the cable space, shrugging off its competitors’ shortfalls.

SUMMARY and Fox Corporation Tearsheet

As the Uniform Accounting tearsheet for Fox Corporation (FOXA:USA) highlights, the Uniform P/E trades at 9.2x, which is below the global corporate average valuation levels, but above its historical average valuations.

Low P/Es require low EPS growth to sustain them. That said, in the case of Fox, the company has recently shown a 8% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Fox’s Wall Street analyst-driven forecast is a 36% EPS growth in 2021 and 23% EPS shrinkage in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Fox’s $33.78 stock price. These are often referred to as market embedded expectations.

Fox is currently being valued as if Uniform earnings were to decline by 14% annually over the next three years. What Wall Street analysts expect for Fox’s earnings growth is above what the current stock market valuation requires in 2021 but below the requirement in 2022.

Furthermore, the company’s earning power is 6x the corporate average. In addition, cash flows are almost 5x its total obligations—including debt maturities, capex maintenance, and dividends. Also, Intrinsic credit risk is 100bps above the risk-free rate. Together, this signals a low dividend and credit risk.

To conclude, Fox’s Uniform earnings growth is well-above with its peer averages and the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research