As more consumers than ever are looking for ATVs, UAFRS reveals the power of the all-terrain business

The At-Home Revolution has affected a swathe of different industries. Surprisingly, vehicles like ATVs and motorcycles have seen an uptick in sales. Today’s company is seeing increased demand for its products as hobbyists are buying more vehicles.

As-reported metrics would have you believe this company’s returns are near corporate averages, but true UAFRS (Uniform) based analysis shows the firm’s real profitability.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

One surprise area that has been boosted by the At-Home Revolution is physical toys. After spending so much time on screens, parents have been buying their kids toys to get them connected with the real world.

For example, Mattel (MAT) is having trouble keeping up with demand. Toys like board games and dolls are flying off the shelves, with demand for Barbie dolls alone rising by 50% last quarter.

However, it’s not just kids interested in physical toys. Adults are buying themselves something nice as well.

Many people have disposable income saved from the lack of vacations this past summer. This has led to adults buying RVs, boats, ATVs, and other vehicles with the saved up cash.

Additionally, international travel appears to be put on hold for the foreseeable future. Motorcycles, RVs, and other vehicles allow Americans to travel across the country in an exciting manner.

People don’t just want any ATV or motorcycle though, they want it to be personalized and full of bells and whistles. This is where Fox Factory (FOXF) comes in.

Fox Factory is the premier name for suspension and shock absorbers. It sells products for a wide variety of vehicles, ranging from bikes to snowmobiles.

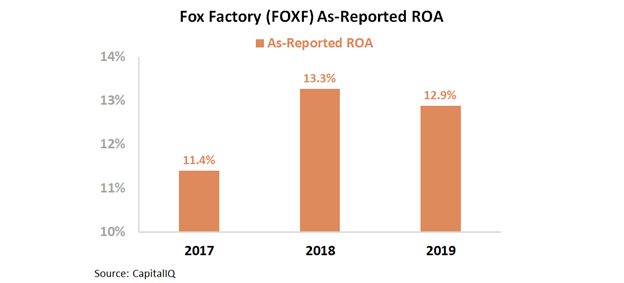

As a premium brand, one would expect the firm to charge a premium price. And yet, as-reported metrics show returns in line with corporate averages. As-reported return on assets (ROA) has ranged between 11% and 13% over the past three years.

However, this is not an accurate depiction of the firm’s profitability. GAAP’s treatment of non-cash stock option expense, accounts payable, and other distortions, is suppressing Fox Factory’s profitability.

Uniform Accounting shows Fox Factory’s premium pricing leads to returns far higher than corporate averages. People want their toys to an exact specification, which is boosting Fox Factory’s returns.

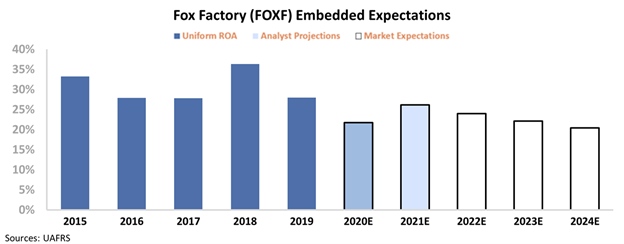

Uniform ROA for the firm has been at least double as-reported ROA over the past three years. It has ranged from 28% to 36% during that time frame.

The final piece of the puzzle we need to look at are expectations for the company. To understand what the market is expecting Fox Factory to do, we can use our Embedded Expectations Framework.

Most investors determine stock valuations using a discounted cash flow (DCF) model. Investors build a DCF model using assumptions about the future, which then produces the “intrinsic value” of the stock.

Here at Valens, we know models with garbage-in assumptions only come out as garbage. This is why we turn the DCF model on its head in the chart below. Here, we use the current stock price to solve for what returns the market expects the firm to make.

The dark blue bars represent the historical corporate performance levels, in terms of ROA. The light blue bars are Wall Street analysts’ expectations for the next two years. Finally, the white bars are the market’s expectations for how ROA will shift in the next five years.

Wall Street understands the At-Home Revolution will continue to help Fox Factory. As such, analysts expect Uniform ROA to remain near current levels. However, the market is pricing in Uniform ROA to fall to 20%.

This would be the lowest level for the firm since it became a public company. It is likely too pessimistic given the positive tailwinds Fox Factory is seeing.

Without Uniform Accounting, investors may miss a company aided by the At-Home Revolution.

Increased demand during the pandemic should continue through the future. If Fox Factory is able to sustain current profitability levels, it may be a company investors should continue watching.

SUMMARY and Fox Factory Holding Corp. Tearsheet

As the Uniform Accounting tearsheet for Fox Factory Holding Corp. (FOXF:USA) highlights, its Uniform P/E trades at 30.4x, which is above global corporate average valuation levels and its historical average valuations.

High P/Es require high EPS growth to sustain them. In the case of Fox Factory, the company has recently shown a 5% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Fox Factory’s Wall Street analyst-driven forecast a 13% EPS decline in 2020 and a 43% EPS growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Fox Factory’s $86 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 13% per year over the next three years. What Wall Street analysts expect for Fox Factory’s earnings growth is below what the current stock market valuation requires in 2020, but above its requirement in 2021.

Furthermore, the company’s earning power is 5x higher than the corporate average. Also, cash flows and cash on hand are 6x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Fox Factory’s Uniform earnings growth is above peer averages, and is trading above peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research