FTC pushback is no problem for this fund

In the past, hedge funds would invest almost exclusively for high net-worth individuals. Today, a large portion of invested capital in hedge funds comes from endowments and pension funds.

Today’s fund helped pioneer these developments back in the 1980s. It brought institutional money to the industry and helped drive high returns for the fund that still continues today.

In addition to examining the portfolio, we include a deeper look into the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Also below is a detailed Uniform Accounting tearsheet of the fund’s largest holding.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

Tom Steyer is probably most famous at this point for his failed 2020 presidential run. However, he first came to prominence as the founder of the successful hedge fund Farallon Capital.

Farallon Capital changed the game for hedge funds. It made a name for itself by being one of the first hedge funds to raise money from university endowments. Previously, hedge funds had invested almost exclusively for high net-worth individuals.

Steyer approached Yale University, his undergraduate alma mater, to give his new fund money to manage. The Yale Endowment initially declined due to the high fees in the hedge fund industry.

However, the Yale Endowment eventually came to an agreement in which Steyer would initially manage the funds for free. After the investment proved to be a success, the endowment began paying fees to Farallon Capital.

This began the influx of endowment and pension funds into the hedge fund industry. No longer did only rich businessmen have access to these investing vehicles.

Farallon also claims to be the primary creator of absolute return investing. Absolute returns are expressed as a percentage of invested capital and generally do not have benchmarks.

Farallon invested in a variety of different asset classes using multiple strategies. It was known for event-driven investing, where the fund would help distressed companies restructure as a stakeholder. For example, Farallon invested in an Argentinian shoe company and stabilized its profits as Argentina recovered from an economic crisis.

Other strategies involved merger arbitrage, real-estate investments, credit investments, and emerging markets.

Steyer eventually left the fund in 2012 to pursue his political interests, but not before leaving a mark on the hedge fund industry.

Farallon Capital has maintained much of the same strategy it employed during the Steyer years. The firm still focuses on merger arbitrage and buying assets that might be in distress looking for an upside.

That said, the firm appears to have recently begun to up its exposure to the real estate market. Farallon has just closed its fourth US-focused opportunistic real estate fund structure with commitments totaling over $650 million. This adds to the fund’s 30-year span of commercial real investing, amounting to about $7.4 billion of capital in 263 investments over that period.

Farallon continues to see wins in the merger arbitrage space, being one of the many funds with large stakes in the Amgen-Horizon deal. According to its recent filings, the company held around 7 million shares in Horizon Therapeutics (HZNP) despite pushback by the FTC. Patience paid off for the fund when the deal closed as it appears they made a pretty penny off the play.

Lastly, Farallon has ramped up its activist efforts for its 7.8% stake in Exelixis (EXCEL). Management has been appointed three additional seats on the board, as the fund has been concerned with unnecessary R&D spending.

In all, the fund has remained resilient since we last talked about it. Its strategy hasn’t diverted and the fund appears to remain active in all spaces invested in.

Today, let’s take a look at Farallon’s top 15 holdings and see if its portfolio is consistent with the recent headlines of the fund’s performance.

Economic productivity is massively misunderstood on Wall Street. This is reflected by the 130+ distortions in the Generally Accepted Accounting Principles (GAAP) that make as-reported results poor representations of real economic productivity.

These distortions include the poor capitalization of R&D, the use of goodwill and intangibles to inflate a company’s asset base, a poor understanding of one-off expense line items, as well as flawed acquisition accounting.

It’s no surprise that once many of these distortions are accounted for, it becomes apparent which companies are in real robust profitability and which may not be as strong of an investment.

See for yourself below.

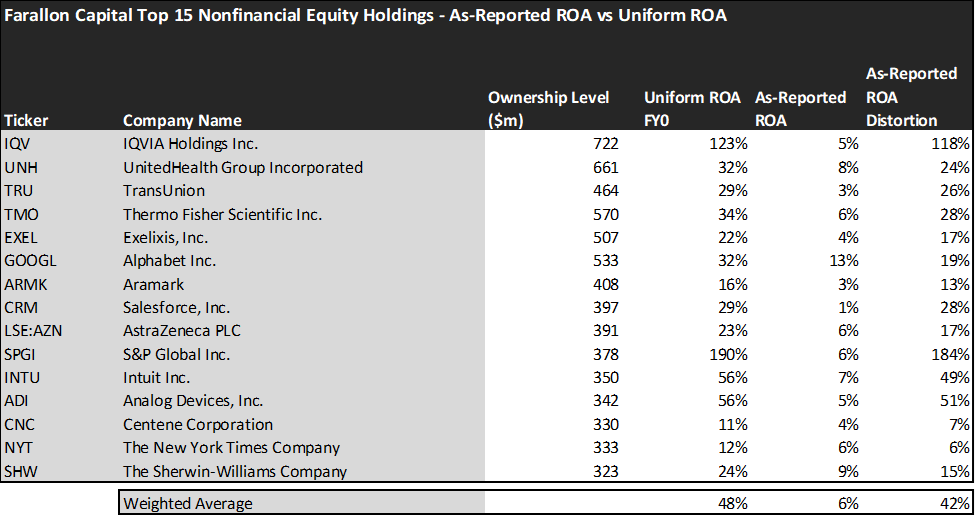

Looking at as-reported accounting numbers, investors would see that Farallon Capital invests in low-quality companies.

On an as-reported basis, many of the companies in the fund are significantly below-average performers. The average as-reported ROA for the top holdings of the fund is 6%, which is notably lower than the 12% U.S. corporate average.

However, once we make Uniform Accounting adjustments to accurately calculate the earning power, we can see that the average return of Farallon Capital’s top holdings is actually extremely profitable compared to what as-reported metrics show, coming in at 48%.

As the distortions from as-reported accounting are removed, we can see that Thermo Fisher Scientific Inc. (TMO) isn’t a 6% return business. Its Uniform ROA is 34%.

That being said, to find companies that can deliver alpha beyond the market, just finding companies where as-reported metrics misrepresent a company’s real profitability is insufficient.

To really generate alpha, any investor also needs to identify where the market is significantly undervaluing the company’s potential.

These dislocations demonstrate that most of these firms are in a different financial position than GAAP may make their books appear. But there is another crucial step in the search for alpha. Investors need to also find companies that are performing better than their valuations imply.

Valens has built a systematic process called Embedded Expectations Analysis to help investors get a sense of the future performance already baked into a company’s current stock price. Take a look:

This chart shows four interesting data points:

- The average Uniform ROA among Farallon Capital’s top holdings is actually 48%, which is way above the corporate average in the United States.

- The analyst-expected Uniform ROA represents what ROA is forecasted to do over the next two years. To get the ROA value, we take consensus Wall Street estimates and convert them to the Uniform Accounting framework.

- The market-implied Uniform ROA is what the market thinks Uniform ROA is going to be in the three years following the analyst expectations, which for most companies here are 2023, 2024, and 2025. Here, we show the sort of economic productivity a company needs to achieve to justify its current stock price.

- The Uniform P/E is our measure of how expensive a company is relative to its Uniform earnings. For reference, the average Uniform P/E across the investing universe is roughly 20x.

Embedded Expectations Analysis of Farallon Capital paints a clear picture. Over the next few years, Wall Street analysts expect the companies in the fund to slightly decrease profitability. Moreover, the market has expectations for these companies to exceed current valuations.

Analysts forecast the portfolio holdings on average to see Uniform ROA fall to 46% over the next two years. At current valuations, the market has higher expectations than analysts and it expects a 53% Uniform ROA for the companies in the portfolio.

For instance, IQVIA Holdings Inc. (IQV) returned 123% this year. Analysts anticipate its returns to decrease to 92%. On the other hand, the market seems to think very optimistically about the company’s future and its pricing in an increase in profitability to reach a Uniform ROA of 116%.

Evidently, Farallon Capital has a strong focus on investing in companies that are financially and operationally sound. Given the current macro environment and downward outlook, these types of investments may allow consistency and decrease the risk of economic implications.

Furthermore, as these companies are operating at very high levels today, the market is also pricing in expectations of future growth. The only issue here is it may limit the upside potential for some of these companies as they would need to exceed their current growth expectations.

Given the diverse strategies and market exposures that Farallon has historically followed, the company does not appear to be concentrated on a specific company or stock. Even considering its merger arbitrage and activist track record, the fund’s money is dispersed relatively evenly among its top holdings.

However, there appears to be a trend of healthcare investments in the company’s top 5 holdings. Despite TransUnion (TRU), the fund’s other holdings all have heavy exposure to the healthcare systems, whether that be in the biotechnology space like Exelixis (EXEL) or life science tools and services such as IQVIA Holdings Inc. (IQV).

This is one thing to consider when looking at the future of this fund’s portfolio. Depending on who you talk to, the healthcare industry can be seen as “recession-proof,” but this does not mean that this doesn’t come with risks. For instance, United Healthcare Group (UNH) is a health insurance provider that could be affected by macro headwinds such as hiking interest rates.

Additionally, Farallon appears to have more of an activist position in Exelixis, as they have recently used its 7.8% stake to achieve more power on the company’s board of directors. Exelixis is a biotech company that specializes in cancer treatments. These types of companies can be unpredictable at times as most of their products are subjected to extensive regulation and testing.

In the end, Farallon has without a doubt proven its ability to maneuver the market and remain a consistent player in the hedge fund industry. However, from an investor standpoint, it’s essential to understand the industry dynamics and business structure of the fund’s portfolio. The fund poses no glaring threats, though the market can be unpredictable.

This just goes to show the importance of valuation in the investing process. Finding a company with strong profitability and growth is only half of the process. The other, just as important part, is attaching reasonable valuations to the companies and understanding which have upside which has not been fully priced into their current prices.

To see a list of companies that have great performance and stability at attractive valuations, the Valens Conviction Long Idea List is the place to look. The conviction list is powered by the Valens database, which offers access to full Uniform Accounting metrics for thousands of companies.

Click here to get access.

Read on to see a detailed tearsheet of one of Farallon Capital’s largest holdings.

SUMMARY and UnitedHealth Group Incorporated Tearsheet

As one of Farallon Capital’s largest individual stock holdings, we’re highlighting the UnitedHealth Group Incorporated (UNH:USA) tearsheet today.

As the Uniform Accounting tearsheet for UnitedHealth Group Incorporated highlights, its Uniform P/E trades at 21.3x, which is above the global corporate average of 18.4x, but around its historical average of 21.6x.

High P/Es require high EPS growth to sustain them. In the case of UnitedHealth Group Incorporated, the company has recently shown 13% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, UnitedHealth Group Incorporated’s Wall Street analyst-driven forecast is for EPS to grow by 11% and 11% in 2023 and 2024, respectively.

Furthermore, the company’s return on assets was 32% in 2022, which is 5x the long-run corporate averages. Also, cash flows and cash on hand consistently exceed its total obligations—including debt maturities and CAPEX maintenance. These signal low dividend risk and low credit risk.

Lastly, UnitedHealth Group Incorporated’s Uniform earnings growth is in line with peer averages, and in line with peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research