This Oil and Gas ‘pickaxe seller’ is priced to fail despite the booming oil market

Commodity prices are surging all over the world, a result of a demand-fueled economic recovery that is running up against tight supplies.

However, in the oil and gas industry, rising prices have yet to be met with ramped-up production. When they do, increased spending on equipment and services will provide temporary tailwinds to a well-positioned cohort of companies.

Today, we’ll highlight one such name that provides essential equipment and expertise to the world’s biggest oil producers.

Specifically, we’ll apply Uniform Accounting and our Embedded Expectations framework to see why both the market and Wall Street analysts are missing the story of a looming recovery in oil spending.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Inflation is a complex phenomenon whose study is mostly the concern of economists, investors, and policymakers.

Only when broad price increases begin to impact everyday Americans does this “hidden tax” start to truly become a hot-button political issue.

And nowhere is the anger associated with higher prices felt more than at the gas pump.

In some places around the U.S., such as California, gas prices are currently trending above $4.70. One country in the state’s interior even has stations charging over $6.00 a gallon.

The cause? A relentless rise in oil and gas prices over the past year or so has been driven by a number of confounding factors.

For one, government stimulus programs to combat the economic impacts of the pandemic have led to surging demand across many economies around the world.

At the same time, the production of the energy required to power this strong recovery has been lagging.

Supply chain disruptions, labor shortages, and shareholder activism in the energy sector have all led oil and gas companies to refrain from large-scale investments to ramp up production.

But as this perfect storm persists, and prices continue to rise, some players in the energy space are thinking about how they can launch one last profit bonanza before potential pressures from environmental regulators gain momentum.

It’s not just the oil producers looking to profit from the current circumstances. The companies that supply them with essential equipment and services see similar opportunities.

These are the businesses that help supermajors like Exxon Mobil (XOM) and Chevron (CVX) explore oil fields and extract oil and gas from the ground or offshore.

When the big oil companies finally start to increase production to take advantage of higher prices, their suppliers standy ready to benefit from increased demand for their expertise.

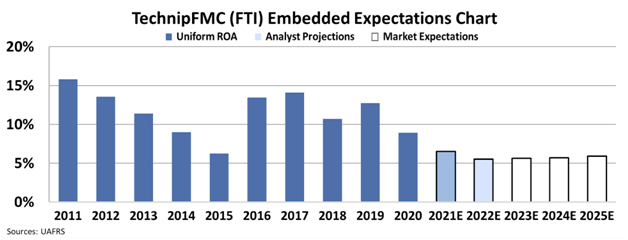

Yet, a company like TechnipFMC (FTI), which is one of the industry’s biggest suppliers to offshore oil exploration activities, is still being priced by the market to see Uniform return on assets (“ROA”) sit at historic lows.

A quick look at our Embedded Expectations Analysis (“EEA”) highlights that going forward, both the market and Wall Street analysts see Uniform ROA collapsing to 6% levels and staying there.

In the chart below, the dark blue bars represent TechnipFMC’s historical corporate performance levels in terms of ROA. The light blue bars are Wall Street analysts’ expectations for the next two years. Finally, the white bars are the market’s expectations for how the company’s ROA will shift over the next five years.

For context, 6% Uniform ROA represents levels last seen in 2015, when the oil industry was in shambles after collapsing to below $50 a barrel.

Today, oil prices are hovering around $80 a barrel and look poised to keep on rising, suggesting that market and analyst expectations for the industry to return to 2015 levels of profitability are overly bearish.

If energy prices stay higher for longer, as many expect they will, it is not unreasonable for a company like TechnipFMC to see returns more in line with what it has historically seen when oil prices were on the rise.

But both the market and Wall Street analysts seem to be totally missing the story.

Thankfully, Uniform Accounting and our Embedded Expectations framework allow us to see that TechnipFMC stands ready to benefit from a recovery in oil production spending likely to happen in the near-term.

SUMMARY and TechnipFMC plc Tearsheet

As the Uniform Accounting tearsheet for TechnipFMC plc (FTI:USA) highlights, the Uniform P/E trades at 21.8x, which is below the global corporate average of 24.0x but above its own historical P/E of 18.9x.

Low P/Es require low EPS growth to sustain them. In the case of TechnipFMC, the company has recently shown a 40% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, TechnipFMC’s Wall Street analyst-driven forecast is 76% and EPS shrinkage in both 2021 and 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify TechnipFMC’s $6 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 9% annually over the next three years. What Wall Street analysts expect for TechnipFMC’s earnings growth is below what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power in 2020 is slightly above the long-run corporate average. Moreover, cash flows and cash on hand are below its total obligations, and intrinsic credit risk is 170bps above risk free rate, signaling high dividend risk.

Lastly, TechnipFMC’s Uniform earnings growth is below peer averages, while the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research