This fund is taking lessons from the Vikings

We covered a “Tiger Cub” fund at the end of 2021, which sought to remain relevant in a market that was undergoing rapid change and poised with uncertainty.

Naturally, many conventional investing techniques have been completely upended by the pandemic and its aftermath.

It’s now two years later, and this fund may be facing choppy waters once again. Post-pandemic performance recovery has been underwhelming. However, 2023 returns suggest that the fund may have found its investment sweet spot.

That said, let’s take a look at the fund’s top 15 holdings and gauge whether its portfolio will be resistant to market turmoil or fall victim to economic downturns once again.

In addition to examining the portfolio, we include a deeper look into the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Also below is a detailed Uniform Accounting tearsheet of the fund’s largest holding.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

The Vikings understood the hedge fund space before it existed.

There are lessons to be learned from the Viking Age that apply to modern-day investing.

The Vikings became traders and raiders because, while they were focused on farming and fishing, those alone could not provide for their people as they grew. Also, a mini-Ice Age led to less productivity of their lands than normal.

The Vikings weren’t just raiding for the sake of raiding. They had to continue to provide for their people like they’d done historically.

Modern investors have had to do much the same, jumping into, and disrupting new markets and pursuing new strategies to try to continue to generate the returns their investors expect.

One of those firms is a fund named after its founder’s ancestors. Ole Andreas Halvorsen was born in Norway, and partially took the fund’s name because of his heritage.

Halvorsen is a Tiger Cub. He was incredibly successful studying under Julian Robertson at Tiger Management, where he was a director of equities and on the supervisory board of the firm’s Jaguar Fund.

He left Tiger in 1999 before the fund closed down, starting Viking Global. However, like all the Tiger Cubs, he has remained part of the network of Cubs that all share ideas and strategies, and themes for investing.

One of the things Halvorsen, and all the Cubs took from Tiger Management’s downfall was the importance of not just focusing on absolute value when making investments, but understanding the fundamental themes driving the market and companies.

However, Viking Global has seen its fair share of calm and stormy market conditions. 2020 featured a sharp downturn, followed by huge gains for investors willing to ride out the down periods.

Then in the beginning of 2021, Viking Global was one of the hedge funds burned during the Gamestop (GME) and AMC (AMC) trading, down 7% in just a few weeks.

Things didn’t change in 2022 either. The fund posted yet another loss of 3% as a result of rising interest rates and an overall poor economic landscape. Although these market conditions continued into 2023, Viking has since recovered some of its losses being up 21% at the end of June.

Amid this unexpected market rally, Viking is now rumored to be accepting new capital into its flagship equity fund that has been closed for over a decade.

Overall, it’s been a busy year for the Tiger Cub fund. Earlier in the year, Viking added 20 new stocks to its portfolio while simultaneously closing out 18 other positions.

Given the drastic changes in its portfolio, let’s take a look at Viking Global’s top 15 holdings and see if the strategy we outlined in 2021 still holds two years later.

Economic productivity is massively misunderstood on Wall Street. This is reflected by the 130+ distortions in the Generally Accepted Accounting Principles (GAAP) that make as-reported results poor representations of real economic productivity.

These distortions include the poor capitalization of R&D, the use of goodwill and intangibles to inflate a company’s asset base, a poor understanding of one-off expense line items, as well as flawed acquisition accounting.

It’s no surprise that once many of these distortions are accounted for, it becomes apparent which companies are in real robust profitability and which may not be as strong of an investment.

See for yourself below.

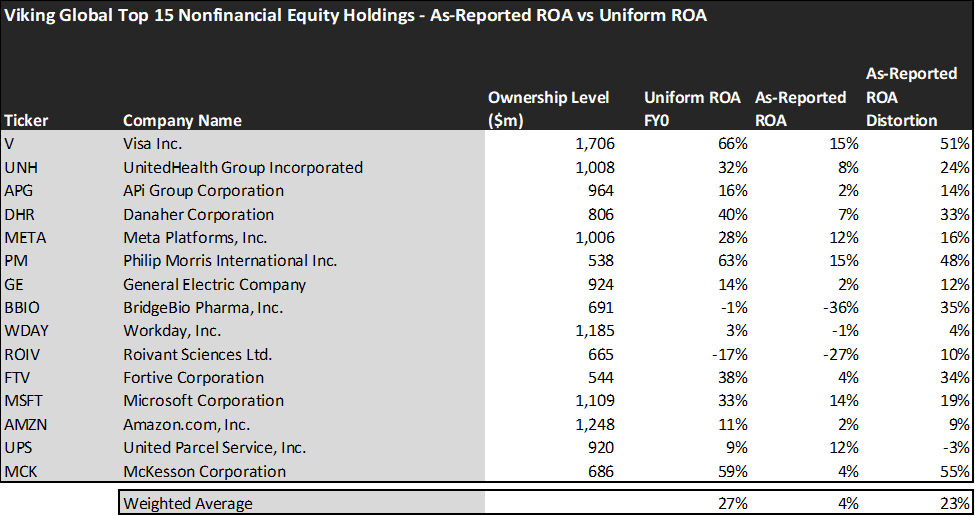

Looking at as-reported accounting numbers, investors would see that Viking Global invests in very low-quality companies.

On an as-reported basis, many of the companies in the fund are significantly below-average performers. The average as-reported ROA for the top holdings of the fund is 4%, which is notably lower than the 12% U.S. corporate average.

However, once we make Uniform Accounting adjustments to accurately calculate the earning power, we can see that the average return of Viking Global’s top holdings is very profitable compared to what as-reported metrics show, coming in at 27%.

As the distortions from as-reported accounting are removed, we can see that Visa (V) isn’t a 15% return business. Its Uniform ROA is 66%.

Meanwhile, Danaher (DHR) seems like a 7% return business, but this large life science company actually powers a 40% Uniform ROA.

That being said, to find companies that can deliver alpha beyond the market, just finding companies where as-reported metrics misrepresent a company’s real profitability is insufficient.

To really generate alpha, any investor also needs to identify where the market is significantly undervaluing the company’s potential.

These dislocations demonstrate that most of these firms are in a different financial position than GAAP may make their books appear. But there is another crucial step in the search for alpha. Investors need to also find companies that are performing better than their valuations imply.

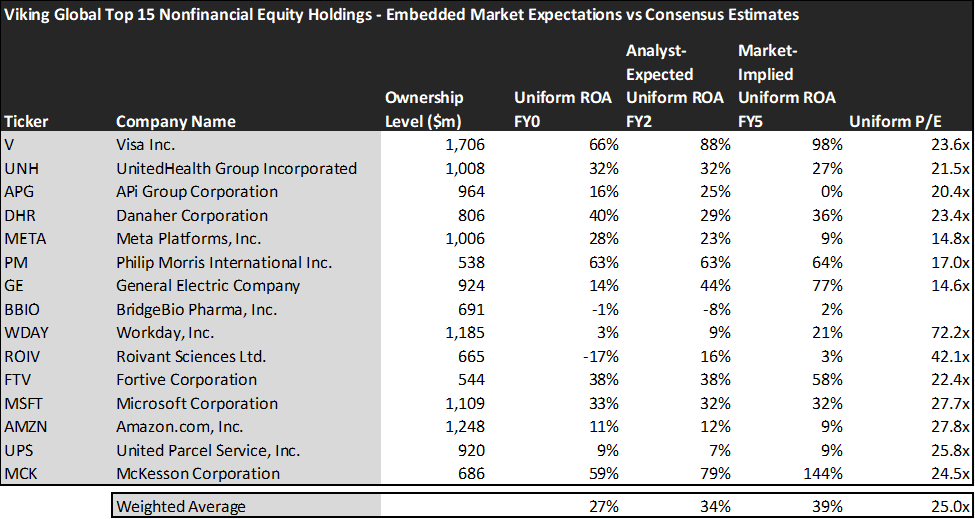

Valens has built a systematic process called Embedded Expectations Analysis to help investors get a sense of the future performance already baked into a company’s current stock price. Take a look:

This chart shows four interesting data points:

- The average Uniform ROA among Viking Global’s top holdings is actually 27%, which is way above the corporate average in the United States.

- The analyst-expected Uniform ROA represents what ROA is forecasted to do over the next two years. To get the ROA value, we take consensus Wall Street estimates and convert them to the Uniform Accounting framework.

- The market-implied Uniform ROA is what the market thinks Uniform ROA is going to be in the three years following the analyst expectations, which for most companies here are 2023, 2024, and 2025. Here, we show the sort of economic productivity a company needs to achieve to justify its current stock price.

- The Uniform P/E is our measure of how expensive a company is relative to its Uniform earnings. For reference, the average Uniform P/E across the investing universe is roughly 20x.

Embedded Expectations Analysis of Viking Global paints a clear picture. Over the next few years, Wall Street analysts expect the companies in the fund to increase profitability. Similarly, the market has expectations for these companies to exceed current valuations.

Analysts forecast the portfolio holdings on average to see Uniform ROA jump to 34% over the next two years. At current valuations, the market has even higher expectations than analysts and it expects a 39% Uniform ROA for the companies in the portfolio.

For instance, Workday (WDAY) returned 3% this year. Analysts anticipate its returns to increase to 9%. Similarly, the market seems to think optimistically about the company’s future and its pricing in an increase in profitability to reach a Uniform ROA of 21%.

Viking Global has a clear investment framework. Almost all of its top holdings are high-quality businesses, from a ROA standpoint, as well as industry.

This sentiment is reflected clearly in the numbers. The average Uniform ROA is more than double the corporate average for the portfolio. Moreover, a majority of these companies are industry leaders that dominate with size.

And for good reason. These companies are industry leaders because they have been able to establish a sustainable competitive advantage. We have done extensive work on developing theories and themes regarding what constitutes a competitive advantage and what doesn’t.

That said, a majority of the holdings in Viking’s portfolio can be bucketed into certain competitive advantages we look for when analyzing companies.

Take Visa for instance. This payment services company is powering a 66% Uniform ROA and it’s expected to jump 98% over the next 5 years. The way it does this is what we call “network effects.”

Visa has consolidated the market and is one of the largest payment networks in the world. People want to be involved in the network as connectivity makes things more efficient and convenient. This principle allows for Visa to function at higher volumes and create better value for its network, thereby leading to stability and growth.

Similarly, UnitedHealth Group (UNH) uses its scale to gain a competitive advantage over peers. While similar, UNH differs as its value is derived from access to data. Like many search engines, UnitedHealth Group’s data is the driving force behind its ability to create better value for customers.

UNH has such an extensive network, with a large pool of accessible data, which provides them the capabilities to improve services faster than competitors. As a healthcare firm, UNH can leverage its data pool to provide options and services that are more catered to its customers, giving them an edge over competitors.

These are just two companies that fall in line with the various themes and concepts related to one’s competitive advantage. Viking Global understands, like us, that a high-quality business must contain some sustainable advantage that will allow it to outperform peers.

In the end, differentiation is key to outlasting competitors, and this portfolio is a great example of that.

This just goes to show the importance of valuation in the investing process. Finding a company with strong profitability and growth is only half of the process. The other, just as important part, is attaching reasonable valuations to the companies and understanding which have upside which has not been fully priced into their current prices.

To see a list of companies that have great performance and stability at attractive valuations, the Valens Conviction Long Idea List is the place to look. The conviction list is powered by the Valens database, which offers access to full Uniform Accounting metrics for thousands of companies.

Click here to get access.

Read on to see a detailed tearsheet of one of Viking Global’s largest holdings.

SUMMARY and Danaher Corporation Tearsheet

As one of Viking Global’s largest individual stock holdings, we’re highlighting the Danaher Corporation’s (DHR:USA) tearsheet today.

As the Uniform Accounting tearsheet for Danaher Corporation highlights, its Uniform P/E trades at 23.4x, which is above the global corporate average of 18.4x, but below its historical average of 25.0x.

High P/Es require high EPS growth to sustain them. In the case of Danaher Corporation, the company has recently shown 10% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Danaher Corporation’s Wall Street analyst-driven forecast is for EPS to shrink by 27% and 4% in 2023 and 2024, respectively.

Furthermore, the company’s return on assets was 40% in 2022, which is 7x the long-run corporate averages. Also, cash flows and cash on hand consistently exceed its total obligations—including debt maturities and CAPEX maintenance. These signal low operating risk and low credit risk.

Lastly, Danaher Corporation’s Uniform earnings growth is below peer averages, and in line with peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research