The digital transformation is helping this professional service provider unlock powerful new insights for clients

The global pandemic has unleashed a wave of digital disruption many experts previously expected was years or even decades away.

With lockdown restrictions and social distancing measures enacted in almost every economy around the world, many companies were forced to change how they do business to survive, adopting digital tools that minimize human interaction and increase efficiency and productivity.

For one firm that provides the expertise required to make these types of transitions, as-reported metrics fail to show how valuable the power of unlocking new insights can be.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Today, one of the most popular buzzwords in C-suites around the US and the world is “digital transformation.”

This idea has to do with taking repetitive human-driven processes, such as manual assembly line inspection in a manufacturing facility, or mundane data entry in an office, and applying new technologies that can save workers valuable time and effort.

At the same time, it also refers to generating more informed insights from the often fragmented systems and disparate data sets now prevalent in every corner of every industry in an increasingly digitized world and economy.

By applying artificial intelligence (“AI”), automation, and advanced data analytics, executives believe they can make their companies smarter, faster, and more efficient, not only cutting down costs but also boosting profits and shareholder returns.

These solutions seem like no-brainers, yet the problem is many companies lack the in-house skillset to apply these vital components of the digital transformation themselves.

As a result, they bring in major consulting firms to try and help. However, anyone working in those firms will tell you they themselves are often still conquering the same sorts of issues they are trying to solve for clients, meaning they don’t exactly lead from a position of expertise.

One exception is Genpact (G), a consulting firm deeply entrenched in digital analytics, AI, and everything else related to the digital transformation, having tailored itself to be well-positioned for this mega trend years before many of its competitors.

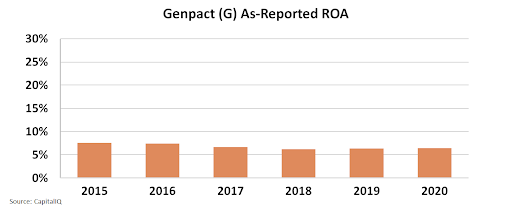

Looking at as-reported financial metrics however, it doesn’t seem Genpact is exactly reaping the benefits of its foresight, with return on assets (“ROA”) hovering around 6%-8% levels over the past five years, just above the average cost of capital in the U.S.

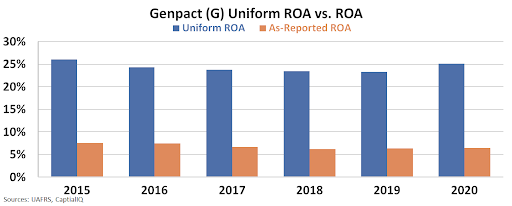

On the surface, this suggests Genpact struggles to generate value with its investments. But in reality, when looking at Uniform Accounting, we can see its cunning strategy and technology leadership have enabled it to be a remarkably stable high-return business.

With Uniform ROA consistently above 20% over the past half decade, along with an inflection higher in the pandemic, Genpact’s story highlights how the right analytics can provide companies with completely new insights that are worth a pretty penny.

With the digital transformation only just getting started, particularly as the COVID-19 pandemic has accelerated many of the underlying forces behind the trend, more and more management teams will need to seek out experts like Genpact to help guide them through the transition.

This means increased demand for business process outsourcing and information technology services, as well as the potential for higher revenues for companies like Genpact.

For investors looking at the next dynamic theme to invest in, they would completely miss the value of the digital transformation without the real Uniform Accounting numbers.

SUMMARY and Genpact Limited Tearsheet

As the Uniform Accounting tearsheet for Genpact Limited (G:USA) highlights, the Uniform P/E trades at 20.4x, which is around the global corporate average of 21.9x but above its historical average of 17.8x.

Average P/Es require average EPS growth to sustain them. In the case of Genpact, the company has recently shown a 15% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Genpact’s Wall Street analyst-driven forecast is an EPS growth of 3% and 11% in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Genpact’s $52 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 1% annually over the next three years. What Wall Street analysts expect for Genpact’s earnings growth is above what the current stock market valuation requires through 2022.

Furthermore, Genpact’s earning power is 4x the corporate average. Also, cash flows and cash on hand are more than its total obligations—including debt maturities, capex maintenance, and dividends. This signals a low credit and dividend risk.

To conclude, Genpact’s Uniform earnings growth is near its peer averages and the company is also trading near average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research