Uniform Accounting shows why recent M&A in the internet domain space was a huge deal

10 million dot-org domain names are changing hands this quarter and yet, most investors don’t seem to care.

This company shows how profitable the domain industry really is, but why that might be changing in the near future.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The internet’s standing as an unregulated entity “for the people” is once again coming under pressure.

Back in November, there was a small news story about a private equity firm called Ethos Capital entering into a purchase agreement with a nonprofit called the Internet Society.

The transaction didn’t get as much press as other internet issues like net neutrality, but it has a similar impact.

Ethos Capital bought an entity called The Public Interest Registry (“PIR”) for more than $1.1 billion.

For those close to the story, the transaction sparked outrage. The PIR owns all of the ‘.org’ domains on the internet and it stewards the process of maintaining reasonable prices for the nonprofits which use these domains.

This may not seem like that big of a deal, but many nonprofits are concerned it could mean their domain costs are about to skyrocket.

There’s nothing stopping the Internet Society from raising prices for .org domains, but the organization’s mission has always been to preserve the ‘ethos’ of the internet.

If you hadn’t heard about this story, you’re not alone. Most didn’t see the financial importance of domain names, which are typically considered to be a boring, low-profit business.

GoDaddy (GDDY) was the first company to get regular people talking about the domain business. GoDaddy runs a domain registry business, along with other add-on solutions for clients.

Whether it was its intriguing name, its list of sponsors they called “advocates,” or its controversial but very popular superbowl ads, GoDaddy got people interested in buying web domains.

That said, even GoDaddy’s ads couldn’t mask the low profitability of the domain business.

Looking at the company’s as-reported ROA, the domain business barely turns a profit. With returns only inflecting positively in the last three years and ROA never improving above 2%, it’s no wonder investors haven’t paid attention to the recent private equity deal.

Even with Ethos Capital being able to raise prices for dot-org domain names, it appears they’ve paid more than a billion dollars for a near-zero return business.

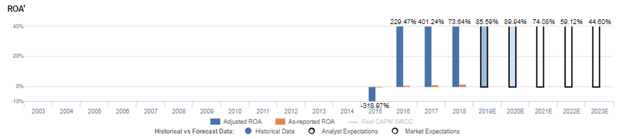

That’s not economic reality, though. When looking at GoDaddy’s Uniform ROA, which takes into account the company’s large non-cash stock option expense, goodwill, and R&D expenses, we can see why Ethos Capital was eager to buy the PIR.

As GoDaddy’s Uniform ROA highlights, the domain business can be massively profitable.

Since reaching positive ROA in 2016, the company has enjoyed 70%+ ROA in each of the last three years.

This is the type of value Ethos Capital is looking to unlock by properly monetizing dot-org domains. That said, their payback window may be narrow.

Despite having strong returns, GoDaddy’s ROA has started coming under pressure in recent years, reaching the low end of historical levels in 2018.

Furthermore, this pressure may continue in the coming years based on management’s concerns around their ability to integrate larger acquisitions and maintain recent growth rates.

While Uniform Accounting highlights that Ethos Capital’s acquisition is more savvy than most investors might think, Uniform Accounting and Valens’ other research also reveals their window to properly monetize the business may be limited.

GoDaddy Inc. Embedded Expectations Analysis – Market expectations are for Uniform ROA to continue to fade, and management may be concerned about acquisition integration, product strength, and top line growth

GDDY currently trades near recent averages relative to UAFRS-based (Uniform) Earnings, with a 24.3x Uniform P/E.

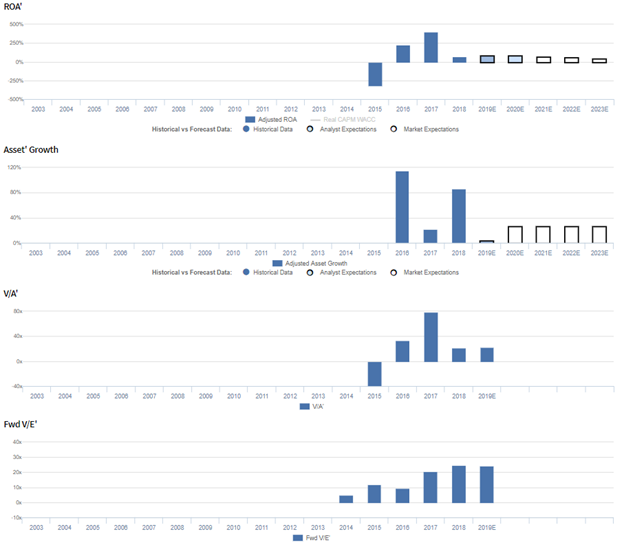

However, even at these levels, the market is pricing in expectations for Uniform ROA to fade from 74% in 2018 to 45% in 2023, accompanied by 26% Uniform Asset growth going forward.

Meanwhile, analysts have bullish expectations, projecting Uniform ROA to improve to 90% levels by 2020, accompanied by 4% Uniform Asset growth.

Historically, GDDY has seen volatile profitability, with Uniform ROA improving from negative levels in 2015 to 401% in 2017, before dropping back to 74% in 2018.

Meanwhile, Uniform Asset growth has been robust, at 115% in 2016, 22% in 2017, and 87% in 2018.

Performance Drivers – Sales, Margins, and Turns

Volatility in Uniform ROA has been driven by volatility in Uniform Asset Turns, coupled with stability in Uniform Earnings Margin.

After improving from immaterial levels in 2015 to 17.8x in 2017, Uniform Asset Turns then fell to 4.1x in 2018.

Meanwhile, Uniform Margin has sustained 17%-23% levels since 2015.

At current valuations, markets are pricing in expectations for Uniform Turns to further compress, coupled with further stability in Uniform Margins.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q3 2019 earnings call highlights that management may be exaggerating the value of their InSight dashboard and the accessibility of their WordPress product.

Furthermore, they may lack confidence in their ability to integrate larger acquisitions and sustain recent top-line growth.

Finally, they may lack confidence in their ability to sustain recent renewal rate improvement and drive active usage of their current products.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for GDDY than as-reported metrics reflect.

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight.

Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate GDDY’s profitability.

For example, as-reported ROA for GDDY was 2% in 2018, substantially lower than Uniform ROA of 74% in the same year.

Moreover, as-reported ROA has never been more than 2%, while Uniform ROA has reached 401%, significantly distorting the market’s perception of the firm’s profitability ceiling.

SUMMARY and GoDaddy Inc. Tearsheet

As the Uniform Accounting tearsheet for GoDaddy Inc. (GDDY) highlights, the Uniform P/E trades at 24.3x, which is above the global corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of GoDaddy, the company has recently shown a -12% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, GoDaddy’s Wall Street analyst-driven forecast is 23% into 2019. That falls down to a 12% growth in earnings in 2020.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $69 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels of GoDaddy, the company would have to have Uniform earnings grow by 22% each year over the next three years.

What Wall Street analysts expect for GoDaddy’s earnings growth increases below what the current stock market valuation requires.

Meanwhile, the company’s earnings power is 12x corporate averages, signaling that there is very low cash flow risk to the company’s operations and credit profile.

To conclude, GoDaddy’s Uniform earnings growth is below peer averages. Also, the company is trading at above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research