General Dynamics is taking off thanks to the rise in private jets

The unexpected restrictions that came with the pandemic put people back in their homes, wildly curtailing the use of public transportation. Only the owners of private vehicles had the chance to travel safely. For most, this meant road trips in 2020 and 2021.

However, this could also mean the air for those who could afford it. Demand for commercial aviation decreased, while the usage of private jets surged. Businesses related to private jets benefited from this development.

One of these companies was General Dynamics (GD). The company manufactures and provides private jets under the Gulfstream brand and enjoys the rise in demand for its products.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

When the world heard about the COVID-19 pandemic at the end of 2019 for the first time, there were only a handful of people that guessed the possible impact.

Even if there was a way to be outside and see friends and family, transportation was a huge issue. Having a private vehicle could save you from the crowds on the bus or train, but it was not an option for everyone.

When it came to long-distance plans, it became even harder. You had to go through the crowd in the check-in area at the airport and wait in queues to sit with possible COVID-19 suspects on a plane.

Between personal fear and government mandates, most airports became ghost towns. The number of passengers carried through air transport decreased from 4.6 billion in 2019 to 1.8 billion in 2020.

However, one kind of jet was still taking off—the private jet.

Travelers can avoid large airports and other passengers, and you do not have to rush to catch the plane, as it waits for you. It is a huge comfort if you have the means.

While commercial planes were on the ground during the pandemic, business leaders and others with means were still able to travel. This meant demand spiked for this relatively niche product.

Private plane usage has climbed reaching 3.3 million in 2021, 7% higher than the previous high seen in 2019.

One of the companies that benefited from this trend was General Dynamics (GD).

General Dynamics is a global aerospace and defense company that specializes in high-end design, engineering, and manufacturing to deliver solutions to its customers.

One of its segments focuses on the company’s aerospace operations, which include producing business jets under the Gulfstream brand and providing aftermarket services.

The aerospace business has footprints on six continents and continues to expand to new regions.

A business that has such a global footprint and benefits from the private plane usage trend would be expected to be booming and have high profitability.

However, the as-reported metrics don’t appear to back this up.

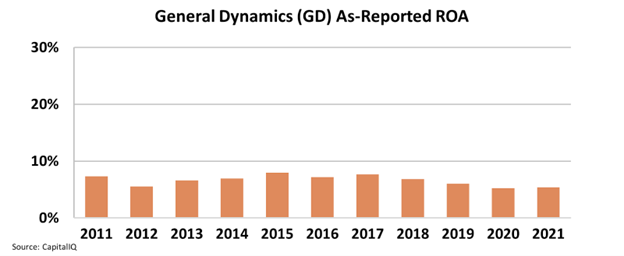

The as-reported return on assets (“ROA”) makes it seem like the company has some problems with profitability, as it never crossed 10% in the last decade, the corporate average.

Even though private plane usage saw the highest levels in 2021, the as-reported ROA was only 5%.

Investors looking at General Dynamics’ performance may think that the business will never be profitable enough, as it is not high even when the demand for the business is flourishing.

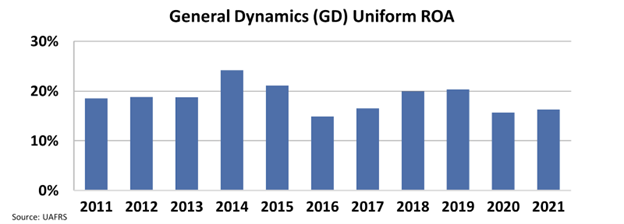

However, this picture of the company’s performance is not accurate. This is due to distortions in as-reported accounting and can be fixed by making the over 130 adjustments needed under Uniform Accounting.

In fact, General Dynamics has been a critical player in a profitable industry. The Uniform ROA of the company has been higher than 10% every single year in the last decade, and was 16% in 2021.

Investors are looking at the wrong data and missing the actual profitability of the company.

Without Uniform Accounting, investors could not see the strong position of General Dynamics. As-reported metrics make the private jet industry seem sluggish when it is in reality a powerful industry to be in after the pandemic.

Uniform Accounting provides the right tools for investors to unlock the real value that the company offers. To learn more about how to gain access to the real numbers for almost 25,000 companies around the world, click here to read about our Uniform Accounting database.

SUMMARY and General Dynamics Corporation Tearsheet

As the Uniform Accounting tearsheet for General Dynamics Corporation (GD:USA) highlights, the Uniform P/E trades at 22.9x, which is above the global corporate average of 20.6x, but around its own historical P/E of 21.5x.

High P/Es require high EPS growth to sustain them. In the case of General Dynamics, the company has recently shown a 2% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, General Dynamics’ Wall Street analyst-driven forecast is an 8% and 12% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify General Dynamics’ $225 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 1% annually over the next three years. What Wall Street analysts expect for General Dynamics’ earnings growth is above what the current stock market valuation requires through 2023.

Furthermore, the company’s earning power in 2021 is 3x the long-run corporate average. Also, cash flows and cash on hand are twice its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals low credit and dividend risk.

Lastly, General Dynamics’ Uniform earnings growth is below its peer averages, and the company is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research