There was nearly no flu season in 2020, but today’s company may be hoping for a virus comeback in 2021

In the height of the pandemic, the market was only fixed on news that could be directly correlated to the lockdown orders or treatment. This meant only one offering from this company was talked about, and the rest forgotten.

However, there is much more to the business, and the headwinds driven by the pandemic significantly disrupted the company’s demand.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

While sickness was on everyone’s minds in 2020, there were many that went unnoticed.

2020 was the year without the flu. As the coronavirus was wreaking havoc on healthcare systems around the globe, individuals began to wear masks and practice social distancing measures.

Thus, the common cold and flu virus had a tough time spreading as they usually do over the winter.

In addition, folks were more aware of viruses in general, with flu vaccinations seeing a spike in 2020 compared to 2019. This further limited the spread of the winter virus.

However, the flu was not the only illness that had trouble spreading.

Sexually transmitted infections (STIs) were down significantly as well. Additionally, the majority of people were not getting preventative care for these types of diseases during the pandemic either.

That being said, a company at the forefront of both the pandemic and these treatments is Gilead Sciences (GILD).

The company was able to help the early fight against the coronavirus thanks to its drug named remdesivir.

However, the company also relies on drugs and treatments for many other diseases, with the headwinds mentioned above hurting performance.

For example, it saw weaker demand for its treatments in relation to illnesses such as HIV and Hepatitis C. These served as material headwinds for this business.

The market neglected this as the company’s treatment for the coronavirus and its development of remdesivir dominated the news cycle. To see whether these headwinds or tailwinds were stronger in 2020, we can turn to the numbers.

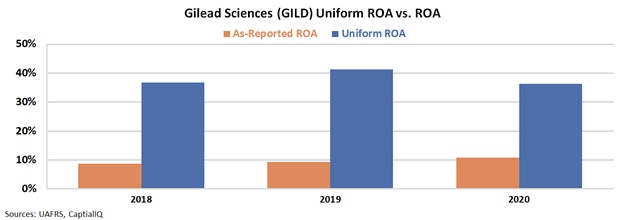

Based on the company’s as-reported metrics, the weak demand and returns seen in various areas of the business was not just a problematic headwind for a high-return business.

It also showed a company with already weak return on assets (ROA) continue to hover around 10% levels.

Specifically, the company’s as-reported ROA levels slightly expanded from 9% levels in 2018 to 11% in 2020.

See for yourself below.

In reality, this is not an accurate picture of Gilead Sciences’ true profitability levels.

The company is not generating returns near corporate averages of 12%. The firm is really producing robust returns.

Specifically, Uniform ROA has been able to maintain 36% levels despite pandemic-related headwinds. This is only a slight decline from 37% levels in 2018.

The as-reported metrics completely misrepresent the company’s profitability.

When looking at Uniform Accounting metrics, we can see that the company has been able to maintain high returns despite headwinds from the pandemic disrupting demand.

By being one of the few companies to treat these types of illnesses, the company is able to profit.

SUMMARY and Gilead Sciences, Inc. Tearsheet

As the Uniform Accounting tearsheet for Gilead Sciences, Inc. (GILD:USA) highlights, the Uniform P/E trades at 9.2x, which is below the global corporate average of 23.7x, but above its own historical average of 7.2x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Gilead Sciences, the company has recently shown a 6% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Gilead Sciences’ Wall Street analyst-driven forecast is a 15% and 9% EPS decline in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Gilead Sciences’ $69 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 17% annually over the next three years. What Wall Street analysts expect for Gilead Sciences’ earnings growth is above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is 6x the long-run corporate average. Also, intrinsic credit risk is 50bps above the risk-free rate and cash flows and cash on hand are around 2x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low dividend and credit risk.

To conclude, Gilead Sciences’ Uniform earnings growth is below its peer averages and the company is trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research