Uniform Accounting shows even companies in “safe” industries have credit and dividend risk the market isn’t capturing

Consumer staples companies like those in the packaged foods and meats industry are thought to be safe, especially in this environment when everyone is stockpiling on longer-lasting foods. Even if there’s no demand for many discretionary goods, everyone still needs to eat.

As a result, consumer staples firms can get higher valuations and lower yields on their debt and equity than those in other industries might.

This can lead to those companies being perceived as safe, even if the data says otherwise. The company below highlights just that: a company that is much less safe than some appear to realize.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

When looking at a company’s credit, one needs to look at more than just the amount of debt outstanding, or ratios of debt to cash flows, or debt to assets. Investors also need to look at more than just the debt, they need to look at all of the company’s obligations.

Specifically, investors need to understand what a firm’s cash flows are like relative to all spending on an ongoing basis. Can it service obligations, or is there some credit risk there?

When cash flows are going to fall short of obligations, and cash on hand is thin, the next step is understanding where a company can trim obligations. For some firms, they can cut capex for a year or two, and just let assets age. Some can trim things like buybacks, with little issue.

For others, they can reduce R&D. We’ve talked about that before, with companies like AMD.

However, sometimes, when those avenues are exhausted, companies have to look to their dividend and other higher priority cash obligations. While not required to keep the company afloat, those that cut dividends signal material risk on the balance sheet. These companies see share prices fall, and bond yields jump.

As our Director of Research highlighted on CNBC recently, General Mills (GIS) is a company that may be facing that risk.

However, the company currently has a very low yield on its outstanding debt, and credit ratings that suggest it is a high-grade firm. It is perceived as a safe name in the current market, selling durable foods that have yet to be disrupted by the current environment. The market is highly optimistic about General Mills, and is looking right past the firm’s obligations.

But when one does look at the firm’s obligations, it is clear not all is rosy:

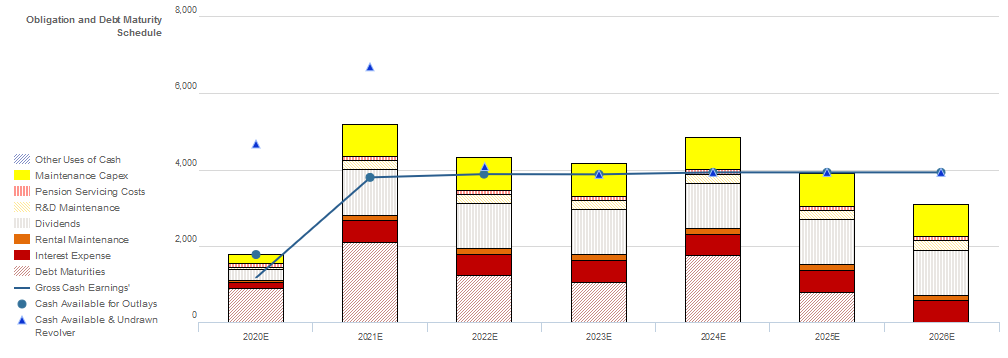

Although General Mills should be able to service obligations in the near-term, once fiscal 2021 is in full-swing, the firm will have decisions to make.

It doesn’t have cash flows nearly as robust as investors might think. Moreover, cash balances are thin currently, at just over $1bn after the firm’s recent debt issuance, which is less than the firm spends annually on dividends.

This looks like a firm that will have to make decisions about spending very soon.

The only other alternative is the firm accesses the credit markets to refinance, which they may be able to do. However, in this environment, a firm that needs help to remain a going concern likely shouldn’t be an investment-grade name, like Moody’s says.

Additionally, low credit and dividend yields suggest the market isn’t quite pricing in the risks related to General Mills’s credit structure, and those may rise as well.

Cash Bond Markets are Overstating GIS’s Credit Risk While Rating Agencies are Understating It

Cash bond markets are grossly overstating credit risk with a YTW of 4.565%, relative to an Intrinsic YTW of 1.595%, while CDS markets are accurately stating credit risk with a CDS of 51bps, relative to an Intrinsic CDS of 28bps.

Meanwhile, Moody’s is materially understating risk, with their Baa2 rating six notches lower than Valens’ HY2- (equivalent to B2) rating.

Fundamental analysis highlights that GIS’s cash flows should comfortably exceed operating obligations in each year going forward. However, the combination of the firm’s cash flows and cash on hand would fall short of meeting all obligations including debt maturities starting in 2020, as the firm faces consistent debt headwalls in each year through 2025.

That said, the firm has some capex flexibility to free up liquidity in the near-term, and given its sizeable market capitalization, it should have access to credit markets to refinance, albeit at potentially unfavorable rates, as a result of its lackluster 30% recovery rate on unsecured debt.

Incentives Dictate Behavior™ analysis highlights positive signals for creditors. GIS’s management compensation framework should drive them to focus on improving all three value drivers; margins, top-line growth, and asset utilization, which should lead to Uniform ROA improvement and higher cash flows available for servicing obligations.

Additionally, management members are material holders of GIS equity relative to their annual compensation, indicating they should be aligned with shareholders for long-term value creation.

Furthermore, most management members are not well compensated in a change-in-control, suggesting that they are unlikely to pursue a sale or accept a buyout of the firm, reducing event risk.

Earnings Call Forensics™ of the firm’s Q3 2020 earnings call (3/18) highlights that management is confident they have played a critical role in meeting customer needs for over 150 years, consumption will shift to at-home in the near future, and that demand in China continues to be strong.

However, they may be concerned about declines in restaurant traffic and away-from-home food demand, the uncertainty surrounding COVID-19, and sharp declines in their China shop business and Asia and Latin America operating profit.

Moreover, they may lack confidence in their ability to sustain cash from operations growth, continue regularly-scheduled production, and service increased e-commerce demand. Finally, management may be exaggerating the strength of their retail partnerships and the sustainability of Gushers and Disney Fruit Snacks performance.

GIS’s operational sustainability and sizeable market capitalization indicate that cash bond markets are overstating credit risk, while consistent and material debt headwalls indicate Moody’s is understating credit risk. As such, both a tightening of cash bond spreads and a ratings downgrade are likely going forward.

SUMMARY and General Mills Tearsheet

As the Uniform Accounting tearsheet for General Mills, Inc. (GIS:USA) highlights, the company trades at a 23.2x Uniform P/E, which is around the global corporate average valuation levels and its historical average valuations.

Moderate P/Es only require moderate EPS growth to sustain them. That said, in the case of General Mills, the company has recently shown a 12% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, General Mills’ Wall Street analyst-driven forecast projects 10% growth in earnings in 2020 followed by 7% shrinkage in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $62 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels for General Mills, the company would just have to have Uniform earnings grow by 3% each year over the next three years.

Wall Street analysts’ expectations for General Mills’ earnings growth are above what the current stock market valuation requires in 2020.

Meanwhile, General Mills’ Uniform earnings growth is above peer average levels, yet the company is still trading below peer valuations.

In addition, the company’s earnings power is 4x corporate averages. Furthermore, total obligations, including debt maturities, maintenance capex, and dividends, are above total cash flows, signaling an average risk to its dividend or operations.

To summarize, General Mills is expected to see above average Uniform earnings growth in 2020, which is expected to decline in 2021, falling short of market expectations. Therefore, as is warranted, the company is trading below peer valuations.

Best regards,

Joel Litman

Chief Investment Strategist

at Valens Research